What is Complete Blood Count Analyzer - Global Market?

A Complete Blood Count (CBC) Analyzer is a crucial tool in the medical field, designed to evaluate the overall health of a patient by measuring various components of blood. This device is essential for diagnosing a wide range of conditions, from infections and anemia to more severe diseases like leukemia. The global market for CBC Analyzers is expanding due to the increasing prevalence of these health conditions and the growing demand for early and accurate diagnosis. These analyzers work by counting and analyzing the different types of cells in the blood, including red blood cells, white blood cells, and platelets. The data provided by CBC Analyzers helps healthcare professionals make informed decisions about patient care. As technology advances, these devices are becoming more sophisticated, offering faster and more precise results. The global market for CBC Analyzers is driven by technological advancements, an aging population, and the rising incidence of chronic diseases, making it a vital component of the healthcare industry. The demand for these analyzers is expected to continue growing as healthcare providers seek to improve diagnostic accuracy and patient outcomes.

Automatic Hematology Analyzers, Semiautomatic Hematology Analyzers in the Complete Blood Count Analyzer - Global Market:

Automatic Hematology Analyzers are advanced devices used in laboratories and hospitals to perform complete blood counts with high precision and efficiency. These analyzers automate the process of counting and classifying blood cells, reducing the need for manual intervention and minimizing human error. They are equipped with sophisticated software and hardware that allow for rapid processing of blood samples, providing results in a matter of minutes. This speed and accuracy are crucial in clinical settings where timely diagnosis can significantly impact patient treatment and outcomes. Automatic Hematology Analyzers are designed to handle large volumes of samples, making them ideal for high-throughput environments such as large hospitals and diagnostic laboratories. They offer a range of features, including the ability to detect abnormal cells and flag them for further analysis, which is essential for diagnosing conditions like leukemia and other blood disorders. On the other hand, Semiautomatic Hematology Analyzers require some level of manual intervention, typically in the preparation of samples or the interpretation of results. While they may not offer the same level of automation as their fully automatic counterparts, they are often more affordable and can be a practical choice for smaller clinics or laboratories with limited budgets. These analyzers still provide accurate and reliable results, making them a valuable tool in the diagnosis and monitoring of various health conditions. The choice between automatic and semiautomatic analyzers often depends on the specific needs and resources of the healthcare facility. Both types of analyzers play a critical role in the global market for CBC Analyzers, catering to different segments of the healthcare industry. As the demand for efficient and accurate diagnostic tools continues to grow, both automatic and semiautomatic hematology analyzers are expected to see increased adoption worldwide. The global market for these devices is driven by factors such as technological advancements, increasing healthcare expenditure, and the rising prevalence of chronic diseases. As healthcare providers strive to improve patient care and outcomes, the demand for reliable and efficient hematology analyzers is likely to continue growing.

Hospital, Laboratory in the Complete Blood Count Analyzer - Global Market:

The usage of Complete Blood Count Analyzers in hospitals is integral to patient care, as these devices provide essential information about a patient's health status. In a hospital setting, CBC Analyzers are used to quickly assess a patient's blood composition, which is crucial for diagnosing a wide range of conditions, from infections and anemia to more severe diseases like leukemia. The ability to rapidly obtain accurate blood counts allows healthcare professionals to make informed decisions about treatment plans and monitor the effectiveness of interventions. In emergency situations, where time is of the essence, CBC Analyzers can provide critical data that guides immediate medical actions. Additionally, these devices are used in routine check-ups and pre-surgical assessments to ensure patients are in optimal health before undergoing procedures. In laboratories, CBC Analyzers are indispensable tools for conducting detailed analyses of blood samples. They are used to perform a variety of tests that help identify abnormalities in blood cell counts and morphology, which can indicate underlying health issues. Laboratories rely on the precision and efficiency of CBC Analyzers to process large volumes of samples, ensuring timely and accurate results for healthcare providers. These analyzers are equipped with advanced technology that allows for the detection of subtle changes in blood cell characteristics, which can be critical for early diagnosis and treatment of diseases. The data generated by CBC Analyzers in laboratories is used to support clinical research and contribute to the development of new diagnostic and therapeutic approaches. The global market for CBC Analyzers in hospitals and laboratories is driven by the increasing demand for accurate and efficient diagnostic tools. As healthcare systems worldwide strive to improve patient outcomes and reduce costs, the adoption of advanced CBC Analyzers is expected to grow. These devices play a vital role in enhancing the quality of care provided to patients, making them an essential component of modern healthcare infrastructure. The continued advancement of technology in this field promises to further improve the capabilities of CBC Analyzers, enabling even more precise and comprehensive blood analyses.

Complete Blood Count Analyzer - Global Market Outlook:

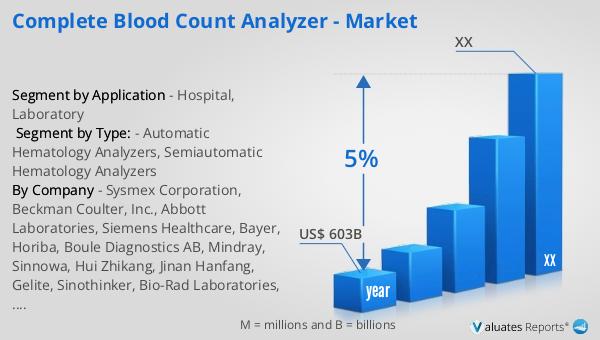

Based on our findings, the worldwide market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth is driven by several factors, including technological advancements, an aging global population, and the increasing prevalence of chronic diseases. As healthcare systems around the world continue to evolve, there is a growing demand for innovative medical devices that can improve patient outcomes and streamline healthcare delivery. The market for medical devices encompasses a wide range of products, from diagnostic equipment like CBC Analyzers to therapeutic devices and surgical instruments. This diverse market is characterized by rapid innovation and intense competition, as companies strive to develop cutting-edge technologies that meet the needs of healthcare providers and patients. The projected growth of the medical device market reflects the ongoing efforts to enhance healthcare quality and accessibility, as well as the increasing emphasis on preventive care and early diagnosis. As the market continues to expand, it presents significant opportunities for companies to develop and commercialize new products that address unmet medical needs and improve patient care. The global medical device market is poised for continued growth, driven by the increasing demand for advanced healthcare solutions and the ongoing pursuit of innovation in the field.

| Report Metric | Details |

| Report Name | Complete Blood Count Analyzer - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Sysmex Corporation, Beckman Coulter, Inc., Abbott Laboratories, Siemens Healthcare, Bayer, Horiba, Boule Diagnostics AB, Mindray, Sinnowa, Hui Zhikang, Jinan Hanfang, Gelite, Sinothinker, Bio-Rad Laboratories, Nihon Kohden, Zoetis |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |