What is Pentanone - Global Market?

Pentanone is a type of organic compound that falls under the category of ketones, which are characterized by a carbonyl group bonded to two hydrocarbon groups. The global market for Pentanone is a niche segment within the broader chemical industry, primarily driven by its applications in various industrial processes. As of 2023, the market was valued at approximately US$ 5 million, with projections indicating a growth to US$ 6 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 2.9% from 2024 to 2030. The demand for Pentanone is influenced by its use as a solvent and intermediate in the production of pharmaceuticals, pesticides, and paints, among other applications. The North American market, in particular, plays a significant role in the global landscape, although specific financial figures for this region were not disclosed. The market dynamics are shaped by factors such as technological advancements, regulatory frameworks, and the evolving needs of end-user industries. As industries continue to innovate and seek efficient chemical solutions, the demand for Pentanone is likely to experience steady growth, albeit within its specialized market segment.

2-Pentanone, 3-Pentanone in the Pentanone - Global Market:

2-Pentanone and 3-Pentanone are two isomers of Pentanone, each with distinct properties and applications that contribute to the global market for this compound. 2-Pentanone, also known as methyl propyl ketone, is a colorless liquid with a pleasant odor, commonly used as a solvent in various industrial applications. Its ability to dissolve a wide range of substances makes it valuable in the formulation of paints, coatings, and adhesives. Additionally, 2-Pentanone serves as an intermediate in the synthesis of pharmaceuticals and agrochemicals, where it plays a crucial role in the production of active ingredients. The compound's volatility and solvency properties are particularly advantageous in processes that require rapid evaporation and efficient mixing. On the other hand, 3-Pentanone, or diethyl ketone, is another isomer with similar solvent properties but is less commonly used compared to 2-Pentanone. It is primarily utilized in the production of perfumes and flavorings, where its distinct odor profile is desirable. The global market for these isomers is driven by their diverse applications across multiple industries, with demand fluctuating based on the specific needs of end-users. The chemical industry continuously explores new applications and formulations to enhance the utility of 2-Pentanone and 3-Pentanone, thereby expanding their market potential. Despite their niche status, these compounds are integral to various manufacturing processes, underscoring their importance in the global chemical market. The market dynamics for 2-Pentanone and 3-Pentanone are influenced by factors such as raw material availability, production costs, and regulatory considerations. As environmental regulations become more stringent, manufacturers are compelled to innovate and develop sustainable production methods for these compounds. This has led to increased research and development efforts aimed at improving the efficiency and environmental impact of Pentanone production. Furthermore, the global market is characterized by a competitive landscape, with numerous players vying for market share through strategic partnerships, mergers, and acquisitions. Companies are also investing in expanding their production capacities to meet the growing demand for Pentanone derivatives. The market's growth trajectory is supported by the rising demand for high-performance solvents and intermediates in emerging economies, where industrialization and urbanization are driving the need for advanced chemical solutions. As the global economy continues to evolve, the market for 2-Pentanone and 3-Pentanone is poised for steady growth, driven by their versatility and indispensability in various industrial applications.

Pharmaceutical Intermediate, Pesticide Intermediate, Solvent, Paint, Others in the Pentanone - Global Market:

Pentanone finds extensive usage across several industries, serving as a crucial component in the production of pharmaceuticals, pesticides, solvents, paints, and other applications. In the pharmaceutical industry, Pentanone acts as an intermediate in the synthesis of various drugs, facilitating the formation of complex chemical structures necessary for therapeutic efficacy. Its role as a solvent in pharmaceutical formulations is equally important, as it aids in the dissolution and stabilization of active ingredients, ensuring consistent drug delivery and performance. In the realm of agrochemicals, Pentanone serves as a pesticide intermediate, contributing to the development of effective pest control solutions. Its chemical properties enable the synthesis of compounds that target specific pests, enhancing crop protection and agricultural productivity. As a solvent, Pentanone is valued for its ability to dissolve a wide range of substances, making it indispensable in the formulation of paints, coatings, and adhesives. Its volatility and solvency properties allow for rapid drying and efficient application, resulting in high-quality finishes and durable coatings. Beyond these primary applications, Pentanone is also utilized in the production of fragrances and flavorings, where its distinct odor profile is leveraged to create appealing sensory experiences. The compound's versatility extends to other industrial processes, where it serves as a key ingredient in the manufacture of rubber, plastics, and textiles. The global market for Pentanone is driven by its diverse applications and the continuous demand for high-performance chemical solutions. As industries seek to enhance their production processes and product offerings, the need for reliable and efficient intermediates like Pentanone remains strong. The market is characterized by ongoing research and development efforts aimed at optimizing the production and application of Pentanone, ensuring its continued relevance in a rapidly evolving industrial landscape. Regulatory considerations also play a significant role in shaping the market dynamics, as manufacturers strive to comply with environmental and safety standards while maintaining competitive pricing and quality. As a result, the global market for Pentanone is poised for steady growth, supported by its indispensable role in various industrial applications and the ongoing pursuit of innovation and sustainability.

Pentanone - Global Market Outlook:

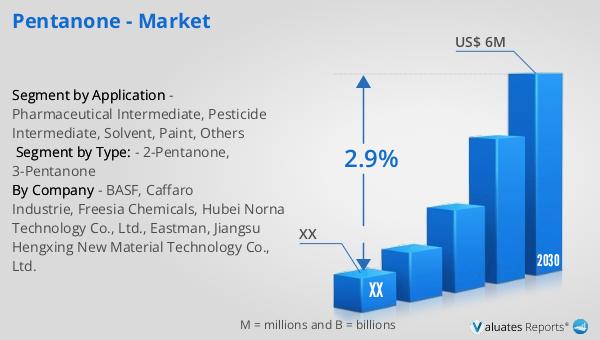

The global market for Pentanone was valued at approximately US$ 5 million in 2023, with projections indicating a growth to US$ 6 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 2.9% from 2024 to 2030. The North American market, in particular, plays a significant role in the global landscape, although specific financial figures for this region were not disclosed. The market dynamics are shaped by factors such as technological advancements, regulatory frameworks, and the evolving needs of end-user industries. As industries continue to innovate and seek efficient chemical solutions, the demand for Pentanone is likely to experience steady growth, albeit within its specialized market segment. The market's growth trajectory is supported by the rising demand for high-performance solvents and intermediates in emerging economies, where industrialization and urbanization are driving the need for advanced chemical solutions. As the global economy continues to evolve, the market for Pentanone is poised for steady growth, driven by their versatility and indispensability in various industrial applications.

| Report Metric | Details |

| Report Name | Pentanone - Market |

| Forecasted market size in 2030 | US$ 6 million |

| CAGR | 2.9% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | BASF, Caffaro Industrie, Freesia Chemicals, Hubei Norna Technology Co., Ltd., Eastman, Jiangsu Hengxing New Material Technology Co., Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |