What is Intrusion Detection Solution - Global Market?

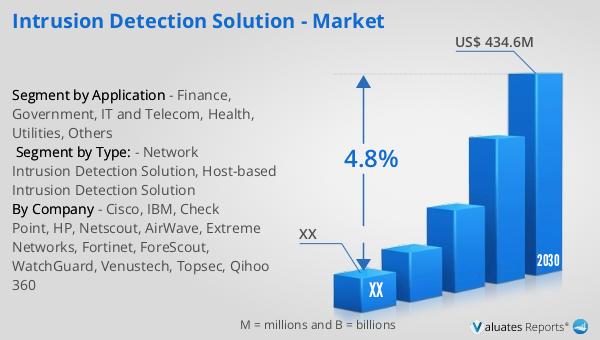

Intrusion Detection Solutions (IDS) are crucial tools in the realm of cybersecurity, designed to monitor and analyze network traffic for signs of unauthorized access or malicious activity. The global market for these solutions is expanding as organizations increasingly prioritize safeguarding their digital assets. In 2023, the market was valued at approximately US$ 276 million, with projections indicating a growth to US$ 434.6 million by 2030, reflecting a compound annual growth rate (CAGR) of 4.8% from 2024 to 2030. This growth is driven by the rising frequency and sophistication of cyber threats, prompting businesses across various sectors to invest in robust security measures. North America, a significant player in this market, is expected to see substantial growth, although specific figures for this region were not provided. The increasing adoption of cloud-based services and the proliferation of Internet of Things (IoT) devices further fuel the demand for IDS, as these technologies introduce new vulnerabilities that need to be monitored and managed. As organizations continue to digitize their operations, the importance of intrusion detection solutions in maintaining the integrity and security of their networks becomes ever more critical.

Network Intrusion Detection Solution, Host-based Intrusion Detection Solution in the Intrusion Detection Solution - Global Market:

Network Intrusion Detection Solutions (NIDS) and Host-based Intrusion Detection Solutions (HIDS) are two primary types of IDS, each serving distinct purposes within the broader cybersecurity landscape. NIDS are designed to monitor and analyze traffic across entire networks, identifying suspicious patterns that may indicate a potential breach. These systems are typically deployed at strategic points within a network, such as gateways or routers, to provide a comprehensive view of all incoming and outgoing data. By examining packet data, NIDS can detect anomalies, unauthorized access attempts, and other malicious activities, alerting administrators to potential threats in real-time. This proactive approach allows organizations to respond swiftly to incidents, minimizing potential damage and data loss. On the other hand, HIDS focus on individual hosts or devices, monitoring system logs, file integrity, and user activities to detect unauthorized changes or suspicious behavior. These solutions are particularly effective in environments where sensitive data is stored on specific machines, as they provide detailed insights into the activities occurring on those devices. By analyzing system-level events, HIDS can identify insider threats, malware infections, and other security breaches that may not be visible at the network level. Both NIDS and HIDS play vital roles in a comprehensive security strategy, offering complementary layers of protection that address different aspects of the threat landscape. As cyber threats continue to evolve, the integration of advanced technologies such as machine learning and artificial intelligence into IDS is becoming increasingly common. These innovations enhance the capabilities of both NIDS and HIDS, enabling them to detect and respond to threats with greater accuracy and speed. Machine learning algorithms, for instance, can analyze vast amounts of data to identify patterns and anomalies that may indicate a security breach, while AI-driven systems can automate the response process, reducing the time it takes to mitigate threats. The global market for intrusion detection solutions is poised for significant growth as organizations across various industries recognize the need for robust security measures. In sectors such as finance, government, IT and telecom, health, and utilities, the adoption of IDS is driven by the need to protect sensitive data and critical infrastructure from increasingly sophisticated cyber threats. As the digital landscape continues to evolve, the demand for effective intrusion detection solutions will only grow, underscoring the importance of these tools in safeguarding the integrity and security of modern networks.

Finance, Government, IT and Telecom, Health, Utilities, Others in the Intrusion Detection Solution - Global Market:

Intrusion Detection Solutions (IDS) are employed across various sectors to enhance security and protect sensitive data from cyber threats. In the finance sector, IDS play a crucial role in safeguarding financial transactions and customer information from unauthorized access and fraud. Financial institutions are prime targets for cybercriminals due to the valuable data they hold, making robust security measures essential. IDS help detect and respond to suspicious activities in real-time, preventing potential breaches and ensuring compliance with regulatory requirements. In the government sector, IDS are used to protect critical infrastructure and sensitive information from cyber espionage and other malicious activities. Government agencies handle vast amounts of confidential data, making them attractive targets for cyberattacks. By deploying IDS, these agencies can monitor network traffic and detect potential threats, ensuring the security and integrity of their systems. In the IT and telecom sector, IDS are vital for maintaining the security of complex networks and preventing unauthorized access to sensitive data. These industries are characterized by rapid technological advancements and the proliferation of connected devices, which introduce new vulnerabilities. IDS help identify and mitigate these risks, ensuring the smooth operation of IT and telecom services. In the healthcare sector, IDS are used to protect patient data and ensure compliance with regulations such as the Health Insurance Portability and Accountability Act (HIPAA). Healthcare organizations store vast amounts of sensitive information, making them attractive targets for cybercriminals. IDS help detect and respond to potential threats, safeguarding patient privacy and maintaining the integrity of healthcare systems. In the utilities sector, IDS are employed to protect critical infrastructure from cyberattacks that could disrupt essential services. Utilities are increasingly reliant on digital systems for operations, making them vulnerable to cyber threats. IDS help monitor network traffic and detect potential threats, ensuring the security and reliability of utility services. Other sectors, such as retail and manufacturing, also benefit from the deployment of IDS to protect sensitive data and maintain the security of their networks. As cyber threats continue to evolve, the importance of IDS in safeguarding critical infrastructure and sensitive information across various industries cannot be overstated.

Intrusion Detection Solution - Global Market Outlook:

The global market for Intrusion Detection Solutions was valued at approximately US$ 276 million in 2023, with expectations of reaching a revised size of US$ 434.6 million by 2030, reflecting a compound annual growth rate (CAGR) of 4.8% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for robust cybersecurity measures across various industries, driven by the rising frequency and sophistication of cyber threats. The North American market, a significant contributor to this growth, is anticipated to experience substantial expansion, although specific figures for this region were not provided. The adoption of cloud-based services and the proliferation of Internet of Things (IoT) devices are key factors driving the demand for intrusion detection solutions, as these technologies introduce new vulnerabilities that need to be monitored and managed. As organizations continue to digitize their operations, the importance of intrusion detection solutions in maintaining the integrity and security of their networks becomes ever more critical. The market's growth trajectory underscores the increasing recognition of the need for effective security measures to protect sensitive data and critical infrastructure from cyber threats.

| Report Metric | Details |

| Report Name | Intrusion Detection Solution - Market |

| Forecasted market size in 2030 | US$ 434.6 million |

| CAGR | 4.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Cisco, IBM, Check Point, HP, Netscout, AirWave, Extreme Networks, Fortinet, ForeScout, WatchGuard, Venustech, Topsec, Qihoo 360 |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |