What is Bulk Handling System - Global Market?

Bulk handling systems are essential components in industries that require the efficient movement and management of large quantities of materials. These systems are designed to handle bulk materials such as grains, minerals, coal, and other raw materials, facilitating their transportation, storage, and processing. The global market for bulk handling systems is driven by the increasing demand for automation and efficiency in material handling processes across various industries. These systems include conveyors, elevators, hoppers, and other equipment that streamline the movement of bulk materials, reducing manual labor and enhancing productivity. The market is characterized by technological advancements that improve the efficiency and reliability of these systems, making them indispensable in sectors like agriculture, mining, construction, and manufacturing. As industries continue to expand and seek more efficient ways to manage their resources, the demand for bulk handling systems is expected to grow, offering significant opportunities for manufacturers and suppliers in this market. The integration of smart technologies and IoT in bulk handling systems is also anticipated to drive market growth, providing real-time data and analytics to optimize operations and reduce downtime. Overall, the bulk handling system global market is poised for steady growth, driven by the need for efficient and automated material handling solutions.

Forklift Loading (FL) Type, Dedicated Hoist Load (DH) Type in the Bulk Handling System - Global Market:

In the realm of bulk handling systems, two prominent types are the Forklift Loading (FL) Type and the Dedicated Hoist Load (DH) Type. The Forklift Loading Type is widely used in industries where flexibility and mobility are crucial. Forklifts are versatile machines that can easily maneuver in tight spaces, making them ideal for loading and unloading bulk materials in warehouses, construction sites, and manufacturing facilities. They are equipped with forks or attachments that can lift and transport heavy loads, providing a cost-effective solution for material handling. The FL type is particularly beneficial in environments where materials need to be moved quickly and efficiently, reducing the time and labor required for manual handling. On the other hand, the Dedicated Hoist Load Type is designed for more specialized applications where precision and control are paramount. Hoists are used to lift and lower heavy loads with the help of a drum or lift-wheel around which rope or chain wraps. This type of bulk handling system is commonly used in industries such as mining, oil and gas, and construction, where heavy materials need to be lifted to significant heights or lowered into deep shafts. The DH type offers enhanced safety and control, making it suitable for handling delicate or hazardous materials. Both types of bulk handling systems have their unique advantages and are chosen based on the specific needs and requirements of the industry. The global market for these systems is driven by the increasing demand for efficient and reliable material handling solutions across various sectors. As industries continue to evolve and seek more advanced technologies, the FL and DH types are expected to see significant growth, offering opportunities for innovation and development in the bulk handling system market.

Construction, Storehouse, Mining, Oil and Gas, Others in the Bulk Handling System - Global Market:

Bulk handling systems play a crucial role in various industries, including construction, storehouse management, mining, oil and gas, and others. In the construction industry, these systems are used to transport and manage materials such as sand, gravel, cement, and other building materials. They help streamline the construction process by ensuring that materials are delivered to the right place at the right time, reducing delays and improving efficiency. In storehouse management, bulk handling systems are used to move and store large quantities of goods, optimizing space and improving inventory management. They enable the efficient loading and unloading of goods, reducing the time and labor required for manual handling. In the mining industry, bulk handling systems are essential for transporting raw materials such as coal, ore, and minerals from the extraction site to processing facilities. They help improve safety and efficiency by reducing the need for manual labor and minimizing the risk of accidents. In the oil and gas industry, bulk handling systems are used to transport and manage materials such as crude oil, natural gas, and other petroleum products. They help ensure the safe and efficient movement of these materials, reducing the risk of spills and environmental damage. Other industries that benefit from bulk handling systems include agriculture, manufacturing, and logistics, where they are used to transport and manage a wide range of materials. Overall, bulk handling systems are essential for improving efficiency, safety, and productivity in various industries, making them a vital component of modern industrial operations.

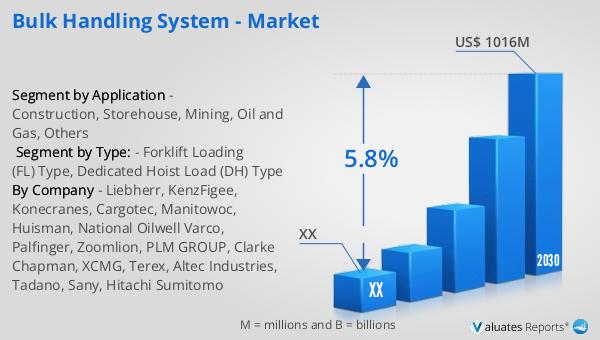

Bulk Handling System - Global Market Outlook:

The global market for bulk handling systems was valued at approximately $645.5 million in 2023. This market is projected to grow significantly, reaching an estimated size of $1,016 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 5.8% during the forecast period from 2024 to 2030. The North American market for bulk handling systems also shows promising growth potential. Although specific figures for the North American market in 2023 and 2030 are not provided, it is anticipated to experience a steady increase in demand, driven by the need for efficient and automated material handling solutions across various industries. The growth in the global and North American markets can be attributed to several factors, including the increasing demand for automation, technological advancements, and the need for efficient material handling solutions in industries such as agriculture, mining, construction, and manufacturing. As industries continue to expand and seek more efficient ways to manage their resources, the demand for bulk handling systems is expected to grow, offering significant opportunities for manufacturers and suppliers in this market. The integration of smart technologies and IoT in bulk handling systems is also anticipated to drive market growth, providing real-time data and analytics to optimize operations and reduce downtime. Overall, the bulk handling system global market is poised for steady growth, driven by the need for efficient and automated material handling solutions.

| Report Metric | Details |

| Report Name | Bulk Handling System - Market |

| Forecasted market size in 2030 | US$ 1016 million |

| CAGR | 5.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Liebherr, KenzFigee, Konecranes, Cargotec, Manitowoc, Huisman, National Oilwell Varco, Palfinger, Zoomlion, PLM GROUP, Clarke Chapman, XCMG, Terex, Altec Industries, Tadano, Sany, Hitachi Sumitomo |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |