What is Smart Street Lighting System - Global Market?

Smart street lighting systems represent a significant advancement in urban infrastructure, combining energy efficiency with cutting-edge technology to enhance public lighting. These systems utilize sensors, wireless communication, and data analytics to optimize street lighting, reducing energy consumption and maintenance costs while improving safety and visibility. By automatically adjusting the brightness based on the time of day, weather conditions, or the presence of pedestrians and vehicles, smart street lighting systems ensure optimal illumination at all times. They also offer remote monitoring and control, allowing city officials to manage lighting networks more effectively. This technology not only contributes to environmental sustainability by lowering carbon emissions but also supports smart city initiatives by integrating with other urban systems, such as traffic management and public safety networks. As cities worldwide strive to become more sustainable and efficient, the global market for smart street lighting systems is poised for significant growth, driven by increasing urbanization, government initiatives for energy conservation, and the rising adoption of IoT technologies. These systems are becoming a cornerstone of modern urban planning, offering a blend of functionality, efficiency, and environmental responsibility.

Wired Street Lighting System, Wireless Street Lighting System in the Smart Street Lighting System - Global Market:

The smart street lighting system market is broadly categorized into wired and wireless systems, each with distinct features and applications. Wired street lighting systems are traditional setups where lights are connected through physical cables. These systems are known for their reliability and stability, as they are less susceptible to interference and signal loss compared to wireless systems. Wired systems are often preferred in areas where consistent and uninterrupted power supply is crucial, such as in industrial zones or regions with high electromagnetic interference. They offer a straightforward approach to integrating smart technologies, allowing for centralized control and monitoring. However, the installation and maintenance of wired systems can be costly and labor-intensive, as they require extensive cabling and infrastructure.

On the other hand, wireless street lighting systems leverage advanced communication technologies like Zigbee, Wi-Fi, or LoRaWAN to connect and control street lights. These systems are more flexible and easier to install, as they eliminate the need for extensive cabling. Wireless systems are ideal for urban areas where infrastructure changes frequently or in locations where laying cables is impractical. They offer scalability, allowing cities to expand their lighting networks without significant additional costs. Wireless systems also enable real-time data collection and analysis, providing valuable insights into energy usage and system performance. This data-driven approach allows for predictive maintenance, reducing downtime and extending the lifespan of lighting fixtures.

Despite their advantages, wireless systems face challenges such as signal interference, security concerns, and the need for regular software updates. Ensuring robust cybersecurity measures is crucial to protect these systems from potential threats. Additionally, the performance of wireless systems can be affected by environmental factors like weather conditions or physical obstructions, which may impact signal strength and reliability.

Both wired and wireless smart street lighting systems contribute to energy efficiency and sustainability. They enable features like dimming, scheduling, and adaptive lighting, which adjust the brightness based on real-time conditions, thereby reducing energy consumption and light pollution. These systems also support integration with other smart city applications, such as traffic management, environmental monitoring, and public safety, enhancing the overall urban living experience.

In conclusion, the choice between wired and wireless smart street lighting systems depends on various factors, including the specific requirements of the area, budget constraints, and long-term urban planning goals. While wired systems offer reliability and stability, wireless systems provide flexibility and ease of deployment. As technology continues to evolve, the integration of advanced features like AI and machine learning will further enhance the capabilities of smart street lighting systems, making them an integral part of future urban landscapes.

Municipal, Industrial Park, Residential Areas in the Smart Street Lighting System - Global Market:

Smart street lighting systems are increasingly being adopted in various areas, including municipal, industrial parks, and residential areas, each with unique requirements and benefits. In municipal areas, smart street lighting plays a crucial role in enhancing public safety and reducing energy costs. By providing adaptive lighting that adjusts based on pedestrian and vehicular traffic, these systems ensure well-lit streets, reducing the risk of accidents and crime. Municipalities benefit from reduced energy bills and maintenance costs, as smart systems enable remote monitoring and control, allowing for quick identification and resolution of issues. Additionally, smart street lighting supports environmental sustainability goals by minimizing energy consumption and carbon emissions, aligning with broader city initiatives for green urban development.

In industrial parks, smart street lighting systems contribute to operational efficiency and safety. These areas often require consistent and reliable lighting to support round-the-clock operations and ensure the safety of workers and equipment. Smart systems provide the necessary illumination while optimizing energy usage through features like motion detection and scheduled dimming. By integrating with other smart technologies, such as surveillance cameras and access control systems, smart street lighting enhances security and operational management within industrial parks. The ability to remotely monitor and control lighting also reduces maintenance efforts and costs, allowing industrial facilities to focus resources on core operations.

Residential areas benefit from smart street lighting systems through improved safety, aesthetics, and energy efficiency. These systems provide well-lit streets and public spaces, enhancing the sense of security for residents and visitors. Smart lighting can be programmed to adjust brightness based on time of day or activity levels, ensuring comfortable and appropriate lighting for different scenarios. This adaptability not only improves the quality of life for residents but also contributes to energy savings and reduced utility bills. Furthermore, smart street lighting can be integrated with other smart home and community systems, creating a cohesive and interconnected living environment.

Overall, the adoption of smart street lighting systems in municipal, industrial, and residential areas underscores the growing importance of smart technologies in urban development. These systems offer a range of benefits, from energy efficiency and cost savings to enhanced safety and environmental sustainability. As cities and communities continue to embrace smart solutions, smart street lighting will play a pivotal role in shaping the future of urban living, providing a foundation for more connected, efficient, and sustainable environments.

Smart Street Lighting System - Global Market Outlook:

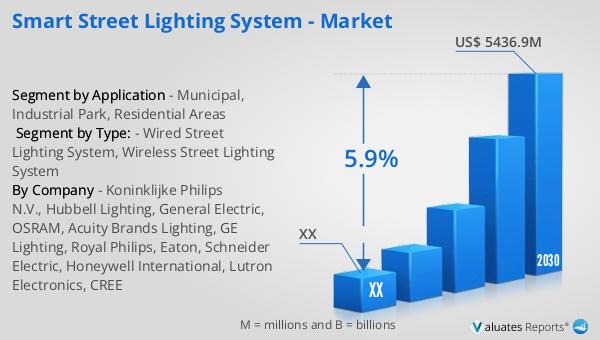

The global market for smart street lighting systems was valued at approximately $3,581.2 million in 2023 and is projected to grow to around $5,436.9 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.9% during the forecast period from 2024 to 2030. This growth is driven by increasing urbanization, government initiatives for energy conservation, and the rising adoption of IoT technologies. In North America, the market was valued at a significant amount in 2023 and is expected to continue its growth trajectory through 2030, although specific figures are not provided. The region's market expansion is supported by technological advancements, infrastructure development, and a strong focus on sustainability. As cities worldwide strive to become more efficient and environmentally friendly, the demand for smart street lighting systems is expected to rise, offering opportunities for innovation and investment in this sector. The market outlook highlights the potential for significant growth and transformation in urban lighting, driven by the need for smarter, more sustainable solutions.

| Report Metric |

Details |

| Report Name |

Smart Street Lighting System - Market |

| Forecasted market size in 2030 |

US$ 5436.9 million |

| CAGR |

5.9% |

| Forecasted years |

2024 - 2030 |

| Segment by Type: |

- Wired Street Lighting System

- Wireless Street Lighting System

|

| Segment by Application |

- Municipal

- Industrial Park

- Residential Areas

|

| By Region |

- North America (United States, Canada)

- Europe (Germany, France, UK, Italy, Russia) Rest of Europe

- Nordic Countries

- Asia-Pacific (China, Japan, South Korea)

- Southeast Asia (India, Australia)

- Rest of Asia

- Latin America (Mexico, Brazil)

- Rest of Latin America

- Middle East & Africa (Turkey, Saudi Arabia, UAE, Rest of MEA)

|

| By Company |

Koninklijke Philips N.V., Hubbell Lighting, General Electric, OSRAM, Acuity Brands Lighting, GE Lighting, Royal Philips, Eaton, Schneider Electric, Honeywell International, Lutron Electronics, CREE |

| Forecast units |

USD million in value |

| Report coverage |

Revenue and volume forecast, company share, competitive landscape, growth factors and trends |