What is Hospital Acquired Infection Testing - Global Market?

Hospital-acquired infection (HAI) testing is a crucial component of the global healthcare market, focusing on identifying infections that patients acquire during their stay in hospitals or healthcare facilities. These infections can occur in various parts of the body and are often resistant to antibiotics, making them challenging to treat. The global market for HAI testing encompasses a range of diagnostic tools and technologies designed to detect these infections early, thereby preventing their spread and improving patient outcomes. This market is driven by the increasing prevalence of HAIs, the growing awareness about infection control, and the need for rapid and accurate diagnostic methods. The market includes various testing methods such as molecular diagnostics, blood tests, and urinalysis, each offering unique benefits in identifying specific types of infections. As healthcare systems worldwide strive to improve patient safety and reduce healthcare costs, the demand for effective HAI testing solutions continues to grow. This market is also influenced by advancements in technology, which have led to the development of more sophisticated and efficient testing methods. Overall, the hospital-acquired infection testing market plays a vital role in enhancing healthcare quality and patient safety globally.

Molecular Diagnostics, Blood Tests, Urinalysis in the Hospital Acquired Infection Testing - Global Market:

Molecular diagnostics, blood tests, and urinalysis are key components of the hospital-acquired infection testing market, each offering distinct advantages in detecting and managing infections. Molecular diagnostics involve the analysis of DNA, RNA, and proteins to identify pathogens responsible for infections. This method is highly sensitive and specific, allowing for the rapid detection of a wide range of infectious agents. Molecular diagnostics are particularly useful in identifying antibiotic-resistant strains, which are a significant concern in hospital settings. Techniques such as polymerase chain reaction (PCR) and next-generation sequencing (NGS) are commonly used in molecular diagnostics, providing precise and timely results that aid in effective treatment planning. Blood tests are another critical tool in HAI testing, used to detect infections that affect the bloodstream. These tests can identify the presence of bacteria, viruses, or fungi in the blood, helping to diagnose conditions such as sepsis, which can be life-threatening if not treated promptly. Blood tests are often used in conjunction with other diagnostic methods to provide a comprehensive assessment of a patient's condition. Urinalysis is a simple yet effective method for detecting infections in the urinary tract, which are among the most common types of HAIs. This test involves analyzing a urine sample for the presence of pathogens, white blood cells, and other indicators of infection. Urinalysis is non-invasive and provides quick results, making it an essential tool in the early detection and management of urinary tract infections. Each of these testing methods plays a crucial role in the hospital-acquired infection testing market, contributing to improved patient outcomes and enhanced infection control measures. As the demand for accurate and efficient diagnostic solutions continues to rise, these testing methods are expected to remain integral to the global HAI testing market.

Urinary Tract Infections, Pneumonia, Surgical Site Infections, Bloodstream Infections, Other Hospital Infections in the Hospital Acquired Infection Testing - Global Market:

Hospital-acquired infection testing is vital in managing and preventing various types of infections that occur in healthcare settings, including urinary tract infections (UTIs), pneumonia, surgical site infections (SSIs), bloodstream infections, and other hospital-related infections. UTIs are among the most common HAIs, often resulting from catheter use. Testing for UTIs typically involves urinalysis, which can quickly identify the presence of pathogens and guide appropriate treatment. Pneumonia acquired in hospitals, particularly ventilator-associated pneumonia, poses significant risks to patients. Molecular diagnostics play a crucial role in identifying the specific pathogens responsible for pneumonia, enabling targeted antibiotic therapy. Surgical site infections occur at the site of surgery and can lead to severe complications if not promptly addressed. Blood tests and molecular diagnostics are often used to detect infections in surgical wounds, allowing for timely intervention and reducing the risk of further complications. Bloodstream infections, such as sepsis, are life-threatening conditions that require immediate attention. Blood tests are essential in diagnosing these infections, providing critical information about the presence of bacteria or fungi in the blood. Other hospital-related infections, such as those affecting the gastrointestinal tract or skin, also require accurate testing methods to ensure effective treatment. The global market for HAI testing encompasses a wide range of diagnostic tools and technologies designed to address these diverse infection types. By providing rapid and accurate results, these testing methods help healthcare providers implement effective infection control measures, ultimately improving patient safety and outcomes. As the prevalence of HAIs continues to rise, the demand for comprehensive testing solutions is expected to grow, driving advancements in diagnostic technologies and enhancing the overall quality of healthcare.

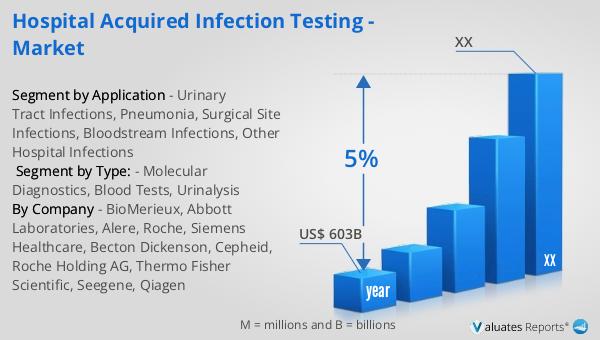

Hospital Acquired Infection Testing - Global Market Outlook:

Based on our research, the global market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth is driven by several factors, including technological advancements, increasing healthcare needs, and a growing emphasis on improving patient outcomes. The medical device market encompasses a wide range of products, from diagnostic equipment and surgical instruments to wearable health monitors and implantable devices. As healthcare systems worldwide strive to enhance the quality of care and reduce costs, the demand for innovative medical devices continues to rise. This market growth is also supported by the increasing prevalence of chronic diseases, an aging population, and the expansion of healthcare infrastructure in emerging economies. Additionally, the integration of digital technologies, such as artificial intelligence and the Internet of Things, into medical devices is transforming the industry, offering new opportunities for personalized medicine and remote patient monitoring. As a result, the global medical device market is poised for significant expansion, driven by the need for advanced healthcare solutions and the continuous evolution of medical technology.

| Report Metric | Details |

| Report Name | Hospital Acquired Infection Testing - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | BioMerieux, Abbott Laboratories, Alere, Roche, Siemens Healthcare, Becton Dickenson, Cepheid, Roche Holding AG, Thermo Fisher Scientific, Seegene, Qiagen |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |