What is Plant Incubators - Global Market?

Plant incubators are specialized devices designed to create controlled environments for the growth and development of plants. These incubators are essential tools in various fields, including agriculture, biology, and research, as they allow for precise regulation of temperature, humidity, light, and other environmental factors. By simulating optimal growing conditions, plant incubators enable researchers and farmers to study plant growth, conduct experiments, and improve crop yields. The global market for plant incubators is driven by the increasing demand for food production, advancements in agricultural technology, and the need for sustainable farming practices. As the world population continues to grow, the pressure on agricultural systems to produce more food with limited resources intensifies. Plant incubators offer a solution by enhancing the efficiency and productivity of plant growth, making them a valuable asset in the quest for food security. Additionally, the rise in research activities related to plant biology and genetics further fuels the demand for plant incubators, as scientists seek to understand plant behavior and develop new crop varieties. Overall, the plant incubators market is poised for significant growth as it addresses critical challenges in agriculture and research.

450μmol m-2 s-1(μE), 1000μmol m-2 s-1(μE) in the Plant Incubators - Global Market:

In the realm of plant incubators, the measurement of light intensity is crucial for optimizing plant growth, and this is often expressed in micromoles per square meter per second (μmol m-2 s-1), also known as microeinsteins (μE). Two common light intensity levels used in plant incubators are 450 μmol m-2 s-1 and 1000 μmol m-2 s-1. The 450 μmol m-2 s-1 level is typically used for plants that require moderate light conditions. This intensity is suitable for many leafy greens and herbs, which thrive under less intense light. It allows for steady growth without the risk of light stress, which can occur if the light is too intense for the plant species. On the other hand, the 1000 μmol m-2 s-1 level is used for plants that require high light conditions, such as tomatoes, peppers, and other fruiting plants. These plants have higher photosynthetic demands and benefit from the increased light intensity, which can lead to faster growth and higher yields. The ability to adjust light intensity in plant incubators is a significant advantage, as it allows for the customization of growing conditions to suit different plant species and stages of growth. This flexibility is particularly important in research settings, where precise control over environmental variables is necessary to conduct experiments and gather accurate data. In the global market, the demand for plant incubators with adjustable light intensity is on the rise, as researchers and growers seek to optimize plant growth and productivity. The ability to simulate different light conditions also supports the study of plant responses to varying environmental factors, contributing to advancements in plant science and agriculture. As technology continues to evolve, plant incubators are becoming more sophisticated, with features such as programmable light cycles, automated climate control, and remote monitoring capabilities. These advancements enhance the functionality and efficiency of plant incubators, making them indispensable tools in modern agriculture and research. The global market for plant incubators is expected to grow as these devices become more accessible and affordable, enabling a wider range of users to benefit from their capabilities. In summary, the use of specific light intensity levels in plant incubators is a key factor in optimizing plant growth and productivity, and the demand for these devices is driven by the need for precise control over growing conditions in various applications.

Biology, Agriculture, Research Room, Others in the Plant Incubators - Global Market:

Plant incubators play a crucial role in various fields, including biology, agriculture, research rooms, and other areas. In biology, plant incubators are used to study plant physiology, genetics, and development. They provide a controlled environment where researchers can manipulate variables such as light, temperature, and humidity to observe how plants respond to different conditions. This is essential for understanding plant behavior and developing new plant varieties with desirable traits. In agriculture, plant incubators are used to improve crop yields and enhance food production. By providing optimal growing conditions, these incubators enable farmers to grow crops more efficiently and sustainably. This is particularly important in regions with harsh climates or limited arable land, where traditional farming methods may not be feasible. In research rooms, plant incubators are used to conduct experiments and gather data on plant growth and development. They allow researchers to test hypotheses and explore new ideas in a controlled setting, leading to advancements in plant science and technology. Additionally, plant incubators are used in other areas such as horticulture, where they are used to propagate plants and produce high-quality seedlings. They are also used in educational settings, where students can learn about plant biology and conduct experiments in a hands-on environment. Overall, plant incubators are versatile tools that support a wide range of applications, from scientific research to commercial agriculture. Their ability to create controlled environments for plant growth makes them invaluable in the quest for sustainable food production and the advancement of plant science. As the global demand for food and agricultural products continues to rise, the use of plant incubators is expected to increase, driving growth in the global market.

Plant Incubators - Global Market Outlook:

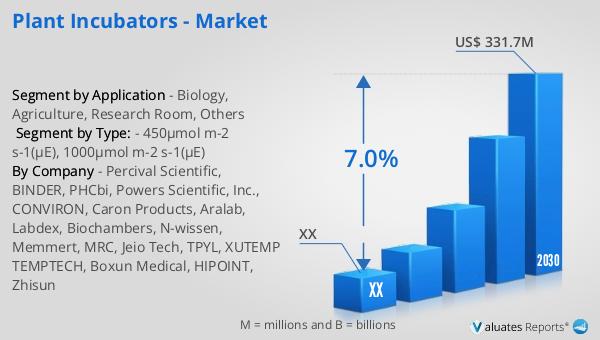

The global market for plant incubators was valued at approximately $203 million in 2023 and is projected to reach a revised size of $331.7 million by 2030, reflecting a compound annual growth rate (CAGR) of 7.0% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for plant incubators across various sectors, driven by the need for efficient and sustainable agricultural practices, as well as advancements in plant research and technology. In North America, the market for plant incubators was valued at a significant amount in 2023, with expectations of continued growth through 2030. The region's market dynamics are influenced by factors such as technological advancements, increased research activities, and the adoption of modern agricultural practices. The projected growth in the North American market underscores the importance of plant incubators in addressing challenges related to food security and sustainable agriculture. As the market continues to expand, manufacturers and suppliers of plant incubators are likely to focus on innovation and the development of advanced features to meet the evolving needs of their customers. Overall, the global market outlook for plant incubators is positive, with significant growth opportunities anticipated in the coming years.

| Report Metric | Details |

| Report Name | Plant Incubators - Market |

| Forecasted market size in 2030 | US$ 331.7 million |

| CAGR | 7.0% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Percival Scientific, BINDER, PHCbi, Powers Scientific, Inc., CONVIRON, Caron Products, Aralab, Labdex, Biochambers, N-wissen, Memmert, MRC, Jeio Tech, TPYL, XUTEMP TEMPTECH, Boxun Medical, HIPOINT, Zhisun |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |