What is Fitness Treadmills - Global Market?

Fitness treadmills are a significant component of the global fitness equipment market, serving as a popular choice for cardiovascular exercise. These machines are designed to simulate walking, jogging, or running indoors, providing users with a convenient and controlled environment for their workouts. The global market for fitness treadmills is driven by increasing health awareness, rising obesity rates, and the growing trend of home fitness. As more people prioritize their health and wellness, the demand for fitness equipment, including treadmills, has surged. Technological advancements have also played a crucial role in the market's growth, with modern treadmills offering features like heart rate monitors, interactive displays, and connectivity with fitness apps. Additionally, the market is influenced by the expansion of fitness centers and gyms, which require high-quality treadmills to meet the needs of their members. The global fitness treadmill market is diverse, with various models catering to different user preferences and budgets, ranging from basic manual treadmills to advanced motorized versions with multiple functions. Overall, the fitness treadmill market is poised for continued growth as more individuals and institutions invest in health and fitness solutions.

Single Function Treadmill, Multifunctional Treadmill in the Fitness Treadmills - Global Market:

In the realm of fitness treadmills, there are two primary categories: single function treadmills and multifunctional treadmills. Single function treadmills are designed primarily for walking, jogging, or running. They are straightforward machines that focus on providing a reliable platform for cardiovascular exercise. These treadmills are often favored by individuals who prefer simplicity and are looking for a cost-effective solution for their home workouts. They typically feature basic controls for speed and incline, allowing users to adjust their workout intensity. Single function treadmills are ideal for those who want to focus solely on their running or walking routine without the distraction of additional features. On the other hand, multifunctional treadmills offer a broader range of features and capabilities. These treadmills are equipped with advanced technology and additional functionalities that enhance the workout experience. They may include features such as built-in workout programs, heart rate monitors, and interactive displays that provide real-time feedback on performance metrics. Some multifunctional treadmills also offer connectivity options, allowing users to sync their workouts with fitness apps or participate in virtual training sessions. These treadmills are designed to cater to fitness enthusiasts who seek a more engaging and versatile workout experience. Multifunctional treadmills are often found in commercial settings, such as gyms and fitness centers, where users expect a comprehensive range of features to support their fitness goals. The global market for fitness treadmills is influenced by the demand for both single function and multifunctional models. While single function treadmills appeal to budget-conscious consumers and those with specific workout preferences, multifunctional treadmills attract users who value technology and versatility in their fitness equipment. Manufacturers in the treadmill market continue to innovate, introducing new features and designs to meet the evolving needs of consumers. As a result, the market offers a wide array of options, ensuring that there is a treadmill to suit every user's requirements and preferences. The choice between single function and multifunctional treadmills ultimately depends on individual fitness goals, budget considerations, and the desired level of engagement during workouts.

Home, Commercial in the Fitness Treadmills - Global Market:

Fitness treadmills are widely used in both home and commercial settings, each offering unique benefits and catering to different user needs. In the home environment, treadmills provide a convenient and accessible way for individuals to maintain their fitness routines without the need to visit a gym. Home treadmills are particularly popular among those with busy schedules, as they allow users to exercise at their convenience, regardless of weather conditions or time constraints. The availability of compact and foldable treadmill models has further increased their appeal for home use, as they can be easily stored when not in use. Home users often appreciate the privacy and comfort of exercising in their own space, and the ability to customize their workout environment to suit personal preferences. On the commercial side, fitness treadmills are a staple in gyms, fitness centers, and health clubs. These establishments require durable and high-performance treadmills to accommodate the diverse needs of their members. Commercial treadmills are built to withstand frequent use and are equipped with advanced features to enhance the workout experience. They often include a variety of pre-set workout programs, heart rate monitoring, and connectivity options to engage users and support their fitness goals. In commercial settings, treadmills are essential for attracting and retaining members, as they are one of the most popular pieces of equipment for cardiovascular exercise. The global market for fitness treadmills is shaped by the demand from both home and commercial users. While home users prioritize convenience, affordability, and space-saving designs, commercial users focus on durability, performance, and advanced features. Manufacturers continue to innovate to meet the specific needs of each segment, offering a range of models that cater to different preferences and budgets. The versatility of fitness treadmills makes them a valuable addition to any fitness regimen, whether at home or in a commercial setting, providing users with an effective and efficient way to achieve their health and fitness goals.

Fitness Treadmills - Global Market Outlook:

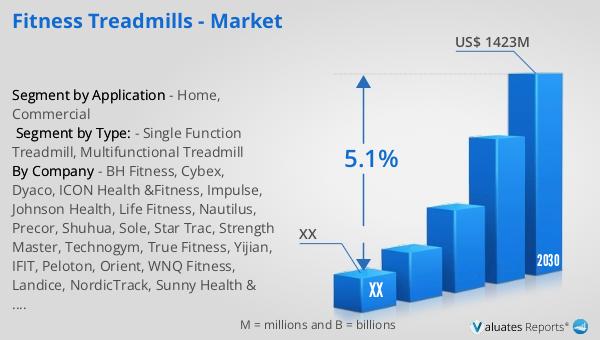

The global market for fitness treadmills was valued at approximately $1,025.6 million in 2023. This market is projected to grow, reaching an estimated size of $1,423 million by 2030, with a compound annual growth rate (CAGR) of 5.1% during the forecast period from 2024 to 2030. This growth reflects the increasing demand for fitness equipment as more individuals and institutions prioritize health and wellness. In particular, the fitness industry in China has shown significant growth, with health industry revenue reaching 8.0 trillion yuan in 2021, marking an increase of 8.1%. This trend highlights the expanding market opportunities for fitness treadmills, driven by rising health awareness and the growing popularity of home and commercial fitness solutions. As consumers continue to invest in their health, the demand for fitness treadmills is expected to rise, supported by technological advancements and the development of innovative features that enhance the user experience. The global fitness treadmill market is poised for continued growth, offering a wide range of options to meet the diverse needs of consumers worldwide.

| Report Metric | Details |

| Report Name | Fitness Treadmills - Market |

| Forecasted market size in 2030 | US$ 1423 million |

| CAGR | 5.1% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | BH Fitness, Cybex, Dyaco, ICON Health &Fitness, Impulse, Johnson Health, Life Fitness, Nautilus, Precor, Shuhua, Sole, Star Trac, Strength Master, Technogym, True Fitness, Yijian, IFIT, Peloton, Orient, WNQ Fitness, Landice, NordicTrack, Sunny Health & Fitness, Goplus, SereneLife |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |