What is Handheld Meter Reader - Global Market?

The handheld meter reader is a specialized device used globally for reading various types of utility meters, such as electricity, gas, and water meters. These devices are designed to streamline the process of meter reading by providing a portable, efficient, and accurate means of collecting data. The global market for handheld meter readers is driven by the increasing demand for efficient utility management and the need to reduce human error in meter reading. These devices are particularly useful in areas where traditional meter reading methods are either impractical or inefficient. They offer the advantage of real-time data collection and transmission, which helps utility companies in billing accuracy and customer service improvement. The market is characterized by a variety of products ranging from basic models that simply record meter readings to more advanced versions that offer features like GPS tracking, wireless data transmission, and integration with utility management software. As technology continues to advance, the handheld meter reader market is expected to evolve, offering even more sophisticated solutions to meet the growing needs of utility companies worldwide.

Basic Function, Full-Featured in the Handheld Meter Reader - Global Market:

Handheld meter readers come in two primary types: basic function and full-featured models. Basic function handheld meter readers are designed to perform the essential task of reading and recording meter data. These devices are typically lightweight, easy to use, and cost-effective, making them ideal for utility companies that require a simple solution for meter reading. They often come with a digital display and a keypad for inputting data, and some models may include basic connectivity options for data transfer. Despite their simplicity, basic function meter readers are reliable and efficient, providing accurate readings that help utility companies maintain billing accuracy and customer satisfaction. On the other hand, full-featured handheld meter readers offer a wide range of advanced functionalities that go beyond basic meter reading. These devices are equipped with features such as GPS tracking, which allows utility workers to easily locate meters and optimize their routes. They also often include wireless communication capabilities, enabling real-time data transmission to central systems for immediate processing and analysis. This feature is particularly beneficial for large utility companies that manage extensive networks of meters, as it allows for more efficient data management and quicker response times to any issues that may arise. Additionally, full-featured meter readers may come with integrated software that allows for seamless integration with existing utility management systems. This integration facilitates the automation of various processes, such as billing and reporting, thereby reducing the need for manual data entry and minimizing the risk of errors. Furthermore, some advanced models are equipped with rugged designs and weather-resistant features, making them suitable for use in harsh environments. This durability ensures that the devices can withstand the rigors of daily use in the field, providing reliable performance over time. Overall, the choice between basic function and full-featured handheld meter readers depends on the specific needs and budget of the utility company. While basic models offer a cost-effective solution for straightforward meter reading tasks, full-featured devices provide a comprehensive toolset for managing complex utility networks and improving operational efficiency. As the global market for handheld meter readers continues to grow, manufacturers are likely to develop even more innovative solutions to meet the evolving demands of utility companies worldwide.

Electricity Meter Reading, Gas Meter Reading, Civil Water Meter Reading in the Handheld Meter Reader - Global Market:

Handheld meter readers play a crucial role in the utility sector, particularly in the areas of electricity, gas, and civil water meter reading. In the electricity sector, these devices are used to accurately record consumption data from residential, commercial, and industrial meters. The portability of handheld meter readers allows utility workers to easily access meters located in various environments, from urban settings to remote rural areas. By providing precise readings, these devices help ensure that customers are billed accurately for their electricity usage, thereby enhancing customer satisfaction and trust. Additionally, the data collected by handheld meter readers can be used to analyze consumption patterns, identify potential issues such as energy theft or meter tampering, and optimize energy distribution across the grid. In the gas sector, handheld meter readers are employed to measure the volume of gas consumed by customers. Accurate gas meter readings are essential for ensuring fair billing and maintaining the safety and efficiency of the gas distribution network. Handheld meter readers equipped with advanced features such as GPS and wireless communication can streamline the process of locating and reading meters, particularly in densely populated urban areas where meters may be difficult to access. The real-time data transmission capabilities of these devices also enable utility companies to quickly detect and respond to any anomalies or leaks in the gas network, thereby enhancing safety and reducing the risk of accidents. In the civil water sector, handheld meter readers are used to monitor water consumption and manage water resources effectively. Accurate water meter readings are crucial for ensuring that customers are billed correctly for their water usage and for promoting water conservation efforts. Handheld meter readers can help utility companies identify leaks, unauthorized connections, and other issues that may lead to water loss or inefficiencies in the distribution system. By providing timely and accurate data, these devices support the sustainable management of water resources and contribute to the overall efficiency of the water supply network. In summary, handheld meter readers are indispensable tools in the utility sector, providing accurate and efficient solutions for electricity, gas, and water meter reading. Their ability to deliver real-time data and integrate with utility management systems makes them valuable assets for utility companies seeking to improve operational efficiency, enhance customer service, and promote sustainable resource management.

Handheld Meter Reader - Global Market Outlook:

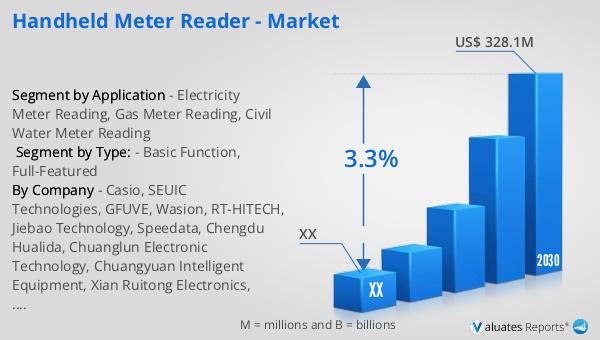

The global market for handheld meter readers was valued at approximately $246 million in 2023 and is projected to grow to a revised size of $328.1 million by 2030, with a compound annual growth rate (CAGR) of 3.3% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for efficient and accurate utility management solutions worldwide. The handheld meter reader market is benefiting from advancements in technology, which are enabling the development of more sophisticated devices with enhanced features such as GPS tracking, wireless communication, and integration with utility management software. These innovations are driving the adoption of handheld meter readers across various sectors, including electricity, gas, and water utilities. In addition to the growth in the handheld meter reader market, the construction machinery sector has also experienced significant expansion. According to data from our Construction Machinery research center, sales of construction machinery in Europe increased by 24% in 2021. In 2022, the construction machinery revenue in Europe was approximately $22 billion, while the U.S. market recorded sales of about $36 billion in construction machinery. This growth in the construction machinery sector reflects the broader trend of increasing investment in infrastructure and utility management solutions, which is likely to further support the expansion of the handheld meter reader market in the coming years.

| Report Metric | Details |

| Report Name | Handheld Meter Reader - Market |

| Forecasted market size in 2030 | US$ 328.1 million |

| CAGR | 3.3% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Casio, SEUIC Technologies, GFUVE, Wasion, RT-HITECH, Jiebao Technology, Speedata, Chengdu Hualida, Chuanglun Electronic Technology, Chuangyuan Intelligent Equipment, Xian Ruitong Electronics, Beijing Zhenzhong |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |