What is Organic Matter Power Generation - Global Market?

Organic matter power generation is an innovative approach to producing energy by utilizing organic materials such as plant and animal waste. This method is gaining traction globally as it offers a sustainable alternative to traditional fossil fuels, which are finite and contribute significantly to environmental pollution. Organic matter power generation involves converting organic waste into energy through various processes like combustion, anaerobic digestion, and gasification. These processes help in reducing the volume of waste, thereby addressing waste management issues while simultaneously generating electricity. The global market for organic matter power generation is expanding as more countries recognize the dual benefits of waste reduction and renewable energy production. This market is driven by increasing environmental awareness, government incentives, and technological advancements that make the conversion processes more efficient and cost-effective. As the world continues to seek sustainable energy solutions, organic matter power generation stands out as a promising option that aligns with global efforts to combat climate change and promote a circular economy.

Solid Biofuels, Biogas, Municipal Waste, Others in the Organic Matter Power Generation - Global Market:

Solid biofuels, biogas, municipal waste, and other organic materials are key components of the organic matter power generation market. Solid biofuels, such as wood pellets, agricultural residues, and other plant-based materials, are used extensively in power generation due to their high energy content and renewability. These materials are typically combusted to produce heat, which is then converted into electricity. The use of solid biofuels is particularly popular in regions with abundant agricultural and forestry resources, as it provides a way to utilize waste products that would otherwise be discarded. Biogas, on the other hand, is produced through the anaerobic digestion of organic matter, such as animal manure, food waste, and sewage sludge. This process generates methane-rich gas that can be used to produce electricity and heat. Biogas is a versatile energy source that can be used in various applications, from small-scale residential systems to large industrial plants. Municipal waste, which includes household and commercial waste, is another significant source of organic matter for power generation. Waste-to-energy plants use advanced technologies to convert municipal waste into electricity, reducing landfill use and greenhouse gas emissions. Other organic materials, such as algae and industrial by-products, are also being explored for their potential in power generation. These materials offer unique advantages, such as rapid growth rates and high energy content, making them attractive options for sustainable energy production. The global market for organic matter power generation is diverse and dynamic, with different regions focusing on different feedstocks based on their availability and economic viability. As technology continues to advance, the efficiency and cost-effectiveness of converting organic matter into energy are expected to improve, further driving the growth of this market.

Residential, Industrial, Commercial, Others in the Organic Matter Power Generation - Global Market:

The usage of organic matter power generation spans various sectors, including residential, industrial, commercial, and others, each benefiting from the unique advantages of this renewable energy source. In the residential sector, organic matter power generation provides households with a sustainable and cost-effective energy solution. Homeowners can utilize small-scale biogas systems to convert kitchen waste and other organic materials into electricity and heat, reducing their reliance on grid power and lowering energy bills. This approach not only promotes energy independence but also encourages waste reduction and environmental responsibility among residents. In the industrial sector, organic matter power generation offers a reliable and efficient energy source for manufacturing processes. Industries with high energy demands, such as food processing and agriculture, can benefit from using organic waste generated on-site to produce electricity and heat. This not only reduces operational costs but also minimizes waste disposal issues and carbon emissions. The commercial sector, including businesses and public institutions, can also leverage organic matter power generation to meet their energy needs sustainably. By adopting waste-to-energy technologies, commercial entities can reduce their environmental footprint while achieving significant cost savings. Additionally, organic matter power generation can be used in remote or off-grid areas where traditional energy infrastructure is lacking. This provides communities with access to reliable and clean energy, improving their quality of life and supporting economic development. Overall, the versatility and sustainability of organic matter power generation make it an attractive option for various sectors, contributing to a cleaner and more resilient energy future.

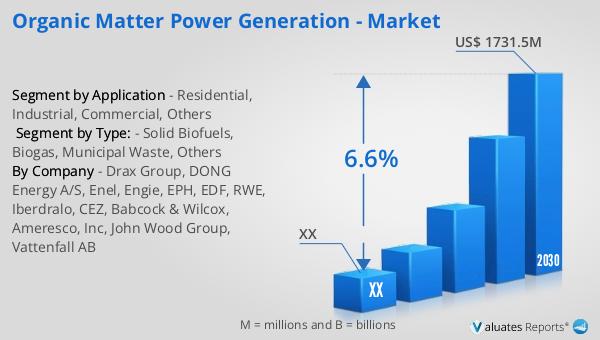

Organic Matter Power Generation - Global Market Outlook:

The global market for organic matter power generation was valued at approximately $1,161 million in 2023 and is projected to grow to around $1,731.5 million by 2030, reflecting a compound annual growth rate (CAGR) of 6.6% during the forecast period from 2024 to 2030. This growth is indicative of the increasing recognition of organic matter power generation as a viable and sustainable energy solution. In China, for instance, the National Bureau of Statistics reported that power generation reached 8.8 trillion kWh in 2022, marking a year-on-year increase of 3.7%. The per capita electricity consumption of residents was recorded at 947 kW. Additionally, China's installed power generation capacity was approximately 2.56 billion kilowatts in 2022, with a year-on-year increase of 7.8%. These statistics highlight the growing demand for energy and the potential for organic matter power generation to play a significant role in meeting this demand. As countries continue to seek sustainable energy solutions, the global market for organic matter power generation is poised for substantial growth, driven by technological advancements, government support, and increasing environmental awareness.

| Report Metric | Details |

| Report Name | Organic Matter Power Generation - Market |

| Forecasted market size in 2030 | US$ 1731.5 million |

| CAGR | 6.6% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Drax Group, DONG Energy A/S, Enel, Engie, EPH, EDF, RWE, Iberdralo, CEZ, Babcock & Wilcox, Ameresco, Inc, John Wood Group, Vattenfall AB |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |