What is Biopharmaceutical Aggregation Analysis System - Global Market?

Biopharmaceutical Aggregation Analysis System is a crucial tool in the global market, primarily focusing on the study and evaluation of protein aggregation in biopharmaceutical products. This system is essential because protein aggregation can significantly impact the safety, efficacy, and stability of biopharmaceuticals, which include therapeutic proteins, monoclonal antibodies, and vaccines. Aggregation can lead to reduced therapeutic effectiveness and increased immunogenicity, posing risks to patient safety. The global market for these systems is driven by the increasing demand for biopharmaceuticals, advancements in analytical technologies, and stringent regulatory requirements for product safety and quality. Companies and research institutions are investing in advanced aggregation analysis systems to ensure the development of safe and effective biopharmaceutical products. These systems employ various techniques such as light scattering, microscopy, and spectroscopy to detect and quantify aggregates at different stages of the drug development process. As the biopharmaceutical industry continues to grow, the demand for sophisticated aggregation analysis systems is expected to rise, making them an integral part of the drug development and quality assurance processes.

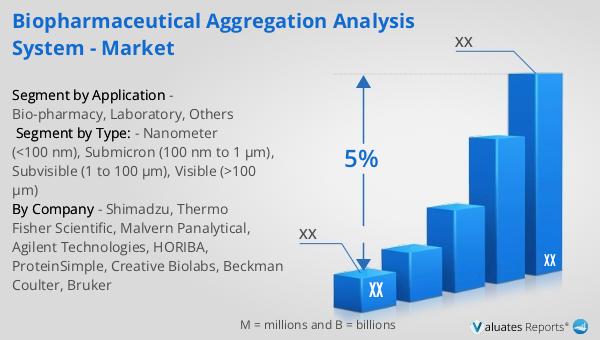

Nanometer (<100 nm), Submicron (100 nm to 1 μm), Subvisible (1 to 100 μm), Visible (>100 μm) in the Biopharmaceutical Aggregation Analysis System - Global Market:

In the realm of biopharmaceutical aggregation analysis, understanding the size and nature of aggregates is crucial for ensuring the safety and efficacy of therapeutic products. Aggregates are typically categorized based on their size: nanometer (<100 nm), submicron (100 nm to 1 μm), subvisible (1 to 100 μm), and visible (>100 μm). Nanometer-sized aggregates are often the result of protein-protein interactions at the molecular level and can be challenging to detect due to their small size. These aggregates can influence the pharmacokinetics and pharmacodynamics of a drug, potentially leading to altered therapeutic outcomes. Submicron aggregates, slightly larger, can form through various mechanisms, including physical stress or chemical reactions during manufacturing and storage. These aggregates are more easily detected than nanometer-sized ones but still require sophisticated analytical techniques for accurate characterization. Subvisible aggregates, ranging from 1 to 100 μm, are of particular concern in biopharmaceuticals because they can trigger immune responses in patients. Regulatory agencies often require detailed analysis of subvisible particles to ensure product safety. Visible aggregates, larger than 100 μm, are typically the result of severe aggregation and are easily detectable by the naked eye. These aggregates can significantly impact the perceived quality of a product and are usually considered unacceptable in final formulations. The biopharmaceutical aggregation analysis system employs a variety of techniques to detect and characterize these aggregates, including dynamic light scattering, size-exclusion chromatography, and flow imaging microscopy. Each technique offers unique insights into the size, distribution, and nature of aggregates, allowing researchers to optimize formulations and manufacturing processes to minimize aggregation. As the biopharmaceutical industry continues to evolve, the ability to accurately detect and characterize aggregates across these size ranges will remain a critical component of ensuring product safety and efficacy.

Bio-pharmacy, Laboratory, Others in the Biopharmaceutical Aggregation Analysis System - Global Market:

The Biopharmaceutical Aggregation Analysis System plays a vital role in various sectors, including bio-pharmacy, laboratories, and other related fields. In bio-pharmacy, these systems are used to ensure the safety and efficacy of biopharmaceutical products by detecting and analyzing protein aggregates. Aggregation can affect the stability and therapeutic effectiveness of drugs, making it essential to monitor and control during the development and manufacturing processes. By employing advanced analytical techniques, bio-pharmaceutical companies can optimize formulations and improve product quality, ultimately enhancing patient safety. In laboratory settings, aggregation analysis systems are used for research and development purposes. Scientists and researchers utilize these systems to study the mechanisms of protein aggregation, develop new therapeutic strategies, and improve existing formulations. The ability to accurately detect and characterize aggregates allows researchers to gain insights into the factors influencing aggregation and develop strategies to mitigate its impact. Additionally, these systems are used in quality control laboratories to ensure that biopharmaceutical products meet regulatory standards and specifications. Beyond bio-pharmacy and laboratories, aggregation analysis systems find applications in other fields such as biotechnology and academia. In biotechnology, these systems are used to develop and optimize bioprocesses, ensuring the production of high-quality biopharmaceuticals. Academic institutions use aggregation analysis systems for educational and research purposes, training the next generation of scientists and researchers in the field of biopharmaceuticals. Overall, the Biopharmaceutical Aggregation Analysis System is an essential tool across various sectors, contributing to the development of safe and effective biopharmaceutical products.

Biopharmaceutical Aggregation Analysis System - Global Market Outlook:

The outlook for the Biopharmaceutical Aggregation Analysis System in the global market is closely tied to the broader pharmaceutical industry trends. In 2022, the global pharmaceutical market was valued at approximately 1,475 billion USD, with an expected compound annual growth rate (CAGR) of 5% over the next six years. This growth is indicative of the increasing demand for pharmaceutical products, including biopharmaceuticals, which are driving the need for advanced aggregation analysis systems. In comparison, the chemical drug market experienced growth from 1,005 billion USD in 2018 to 1,094 billion USD in 2022. This growth highlights the expanding market for chemical drugs, which, while significant, is outpaced by the rapid advancements and increasing demand in the biopharmaceutical sector. The need for sophisticated aggregation analysis systems is further emphasized by the stringent regulatory requirements for product safety and quality in the biopharmaceutical industry. As the market continues to grow, companies and research institutions are investing in advanced technologies to ensure the development of safe and effective biopharmaceutical products. The Biopharmaceutical Aggregation Analysis System is expected to play a crucial role in this growth, providing the necessary tools and techniques to detect and characterize protein aggregates, optimize formulations, and ensure product quality.

| Report Metric | Details |

| Report Name | Biopharmaceutical Aggregation Analysis System - Market |

| CAGR | 5% |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Shimadzu, Thermo Fisher Scientific, Malvern Panalytical, Agilent Technologies, HORIBA, ProteinSimple, Creative Biolabs, Beckman Coulter, Bruker |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |