What is Face Masks for Women - Global Market?

Face masks for women have become an essential part of skincare routines worldwide, driven by a growing awareness of skincare benefits and the desire for healthier, more radiant skin. The global market for these products is vast and diverse, encompassing a wide range of masks designed to address various skin concerns. From sheet masks to clay masks, the options are plentiful, catering to different skin types and needs. The market is fueled by innovations in skincare technology and ingredients, with manufacturers constantly developing new formulations to meet consumer demands. This market is not just about beauty; it's about self-care and wellness, as more women incorporate face masks into their regular skincare regimens. The popularity of face masks is also boosted by social media trends and endorsements by beauty influencers, making them a staple in beauty routines across the globe. As the market continues to grow, it reflects a broader trend towards personalized skincare solutions, where consumers seek products that cater specifically to their unique skin concerns and preferences. This dynamic market is characterized by its rapid growth and the continuous introduction of new and improved products that promise to deliver visible results.

Anti-Aging Mask, Moisturizing Mask, Whitening Mask in the Face Masks for Women - Global Market:

The global market for face masks for women includes a variety of products, each designed to target specific skin concerns. Among these, anti-aging masks, moisturizing masks, and whitening masks are particularly popular. Anti-aging masks are formulated to combat signs of aging such as wrinkles, fine lines, and sagging skin. They often contain ingredients like retinol, collagen, and hyaluronic acid, which are known for their ability to improve skin elasticity and promote a youthful appearance. These masks are highly sought after by women looking to maintain a youthful complexion and delay the visible effects of aging. Moisturizing masks, on the other hand, focus on hydrating the skin. They are ideal for women with dry or dehydrated skin, as they provide an intense moisture boost that helps to restore the skin's natural barrier. Ingredients like aloe vera, glycerin, and hyaluronic acid are commonly used in these masks to lock in moisture and leave the skin feeling soft and supple. Whitening masks are designed to brighten the complexion and reduce the appearance of dark spots and uneven skin tone. They often contain ingredients like vitamin C, niacinamide, and licorice extract, which are known for their skin-brightening properties. These masks are popular among women who want to achieve a more radiant and even skin tone. The demand for these masks is driven by a growing awareness of skincare benefits and the desire for products that deliver visible results. As women become more informed about the ingredients and benefits of different face masks, they are increasingly seeking out products that cater to their specific skin concerns. This has led to a surge in demand for specialized masks that offer targeted solutions for anti-aging, moisturizing, and whitening. The market for these masks is highly competitive, with numerous brands vying for consumer attention by offering innovative formulations and unique ingredients. As a result, consumers have a wide range of options to choose from, allowing them to find the perfect mask for their individual needs. This diversity in product offerings is a key factor driving the growth of the global face masks for women market, as it caters to the diverse needs and preferences of consumers worldwide.

Oily Skin, Dry Skin, Normal Skin in the Face Masks for Women - Global Market:

Face masks for women are designed to cater to different skin types, including oily, dry, and normal skin. For women with oily skin, face masks can help control excess oil production and reduce the appearance of pores. Clay masks, for example, are particularly effective for oily skin as they absorb excess oil and impurities, leaving the skin feeling clean and refreshed. Ingredients like kaolin and bentonite clay are commonly used in these masks for their oil-absorbing properties. Additionally, masks containing salicylic acid or tea tree oil can help to unclog pores and prevent breakouts, making them ideal for women with acne-prone oily skin. For women with dry skin, moisturizing masks are essential for providing the hydration needed to maintain a healthy skin barrier. These masks often contain ingredients like hyaluronic acid, glycerin, and aloe vera, which help to lock in moisture and soothe dry, flaky skin. Sheet masks are a popular choice for dry skin, as they deliver a concentrated dose of hydration and nutrients directly to the skin. Women with normal skin can benefit from a variety of face masks, depending on their specific skincare goals. For example, they may choose a brightening mask to enhance their natural glow or a detoxifying mask to remove impurities and maintain a clear complexion. Masks containing antioxidants like vitamin C or green tea extract can help to protect the skin from environmental damage and promote a healthy, radiant appearance. Regardless of skin type, face masks offer a convenient and effective way for women to address their skincare concerns and achieve their desired results. The global market for face masks for women continues to grow as more women recognize the benefits of incorporating these products into their skincare routines. With a wide range of masks available to suit different skin types and concerns, women have the flexibility to choose products that best meet their individual needs. This personalized approach to skincare is a key factor driving the popularity of face masks, as it allows women to tailor their skincare routines to achieve optimal results.

Face Masks for Women - Global Market Outlook:

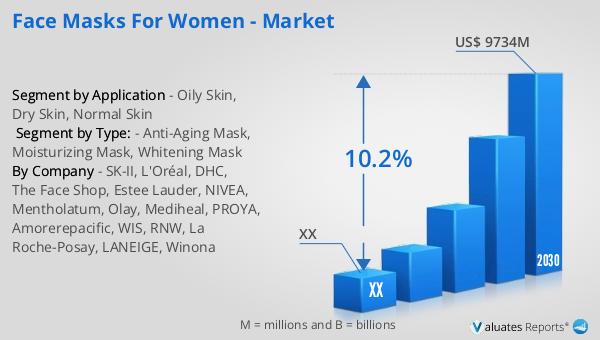

The global market for face masks for women was valued at approximately $5,059 million in 2023. This market is expected to experience significant growth, with projections indicating that it will reach an adjusted size of $9,734 million by 2030. This growth is driven by a compound annual growth rate (CAGR) of 10.2% during the forecast period from 2024 to 2030. In North America, the market for face masks for women was valued at a certain amount in 2023, and it is anticipated to grow to a specific value by 2030, maintaining a steady CAGR throughout the forecast period. This growth reflects the increasing demand for face masks as more women prioritize skincare and seek products that offer targeted solutions for their specific skin concerns. The market's expansion is also supported by advancements in skincare technology and the introduction of innovative products that cater to the diverse needs of consumers. As the market continues to evolve, it is expected to offer a wide range of options for women seeking effective and personalized skincare solutions. The growing popularity of face masks is a testament to the importance of self-care and wellness in today's fast-paced world, where women are increasingly investing in products that enhance their overall well-being and confidence.

| Report Metric | Details |

| Report Name | Face Masks for Women - Market |

| Forecasted market size in 2030 | US$ 9734 million |

| CAGR | 10.2% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | SK-II, L'Oréal, DHC, The Face Shop, Estee Lauder, NIVEA, Mentholatum, Olay, Mediheal, PROYA, Amorerepacific, WIS, RNW, La Roche-Posay, LANEIGE, Winona |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |