What is Treatment Dental Equipment - Global Market?

Treatment dental equipment refers to the various tools and devices used by dental professionals to diagnose, treat, and manage oral health conditions. This equipment is essential for performing a wide range of dental procedures, from routine cleanings to complex surgeries. The global market for treatment dental equipment is vast and continually evolving, driven by advancements in technology, increasing awareness of oral health, and the growing demand for cosmetic dentistry. Key components of this market include diagnostic equipment like X-ray machines, treatment devices such as dental lasers and drills, and auxiliary equipment like sterilization units. The market is also influenced by factors such as the aging population, rising disposable incomes, and the increasing prevalence of dental diseases. As dental practices strive to offer more efficient and effective treatments, the demand for advanced dental equipment continues to rise. This market is characterized by a high level of innovation, with manufacturers constantly developing new products to meet the changing needs of dental professionals and patients. Overall, the treatment dental equipment market plays a crucial role in enhancing the quality of dental care worldwide.

Soft Tissue Lasers, All Tissue Lasers in the Treatment Dental Equipment - Global Market:

Soft tissue lasers and all tissue lasers are integral components of the treatment dental equipment market, each serving distinct yet overlapping purposes in dental care. Soft tissue lasers are primarily used for procedures involving the gums and other soft tissues in the mouth. They offer precision and control, allowing dentists to perform tasks such as gum reshaping, removing excess tissue, and treating periodontal disease with minimal discomfort to the patient. The use of soft tissue lasers reduces bleeding, speeds up recovery time, and minimizes the risk of infection, making them a preferred choice for many dental procedures. On the other hand, all tissue lasers are versatile tools capable of working on both soft and hard tissues, including teeth and bone. This versatility makes them invaluable in a wide range of dental treatments, from cavity preparation and root canal therapy to bone contouring and implant placement. All tissue lasers provide a high degree of accuracy, reducing the need for anesthesia and enhancing patient comfort. The adoption of laser technology in dentistry is driven by the desire for minimally invasive procedures that offer faster healing times and improved outcomes. Both soft tissue and all tissue lasers represent significant advancements in dental technology, offering benefits such as reduced chair time, increased precision, and enhanced patient satisfaction. As the global market for treatment dental equipment continues to grow, the demand for laser technology is expected to rise, driven by the increasing emphasis on patient-centered care and the ongoing development of new laser applications. Dental professionals are increasingly recognizing the advantages of incorporating laser technology into their practices, not only for its clinical benefits but also for its ability to attract patients seeking modern, efficient dental care. The integration of lasers into dental treatment plans reflects a broader trend towards adopting innovative technologies that improve the quality and efficiency of care. As research and development in this field continue, we can expect to see further advancements in laser technology, expanding its applications and enhancing its effectiveness in dental practice. The global market for treatment dental equipment, including soft tissue and all tissue lasers, is poised for continued growth as dental professionals and patients alike recognize the value of these cutting-edge tools in delivering superior oral health care.

Hospital, Clinics, Dental Laboratories in the Treatment Dental Equipment - Global Market:

The usage of treatment dental equipment varies across different settings, including hospitals, clinics, and dental laboratories, each with its unique requirements and applications. In hospitals, dental equipment is often used in specialized departments that handle complex cases requiring multidisciplinary care. Hospitals may have advanced imaging equipment, surgical tools, and anesthesia machines to support oral and maxillofacial surgeries, trauma care, and other intricate procedures. The integration of dental equipment in hospitals ensures comprehensive care for patients with complex medical and dental needs, facilitating collaboration between dental specialists and other healthcare professionals. In clinics, treatment dental equipment is primarily used for routine dental care and minor surgical procedures. Clinics typically have a range of equipment, including dental chairs, X-ray machines, and sterilization units, to support general dentistry, orthodontics, and cosmetic procedures. The focus in clinics is often on providing efficient, patient-centered care, with an emphasis on preventive treatments and early intervention. Dental clinics are increasingly adopting advanced technologies, such as digital imaging and laser equipment, to enhance diagnostic accuracy and treatment outcomes. In dental laboratories, treatment dental equipment is used to fabricate dental prosthetics, such as crowns, bridges, and dentures. Laboratories rely on precision equipment, including CAD/CAM systems and 3D printers, to create custom dental appliances that meet the specific needs of patients. The use of advanced equipment in dental laboratories ensures high-quality, durable prosthetics that improve patient satisfaction and oral health outcomes. The global market for treatment dental equipment is driven by the diverse needs of these settings, with manufacturers developing specialized products to meet the demands of hospitals, clinics, and laboratories. As the dental industry continues to evolve, the integration of innovative technologies and equipment across these settings is essential for delivering high-quality, efficient dental care. The ongoing development of new treatment dental equipment reflects the industry's commitment to improving patient outcomes and enhancing the overall quality of oral health care.

Treatment Dental Equipment - Global Market Outlook:

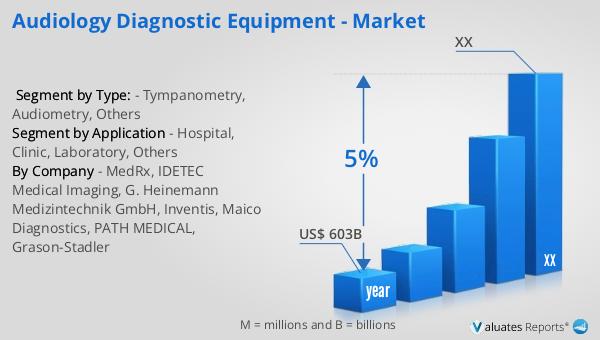

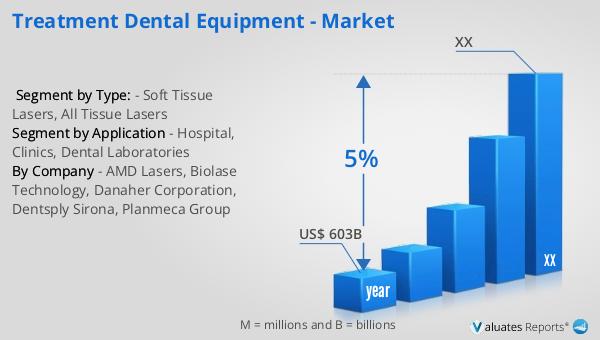

According to our research, the global market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth is indicative of the increasing demand for advanced medical technologies and the expanding healthcare needs of populations worldwide. The medical device market encompasses a wide range of products, including diagnostic equipment, surgical instruments, and treatment devices, each playing a crucial role in modern healthcare delivery. The projected growth rate reflects the ongoing innovation and development within the industry, as manufacturers strive to create more effective, efficient, and patient-friendly solutions. Factors contributing to this growth include the rising prevalence of chronic diseases, an aging global population, and the increasing emphasis on early diagnosis and preventive care. Additionally, technological advancements, such as the integration of artificial intelligence and digital health solutions, are driving the evolution of medical devices, enhancing their capabilities and expanding their applications. As the market continues to grow, stakeholders across the healthcare ecosystem, including providers, payers, and patients, stand to benefit from improved access to cutting-edge medical technologies that enhance the quality and efficiency of care. The global medical device market's robust growth trajectory underscores the critical role these technologies play in shaping the future of healthcare, offering new opportunities for innovation and collaboration across the industry.

| Report Metric | Details |

| Report Name | Treatment Dental Equipment - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | AMD Lasers, Biolase Technology, Danaher Corporation, Dentsply Sirona, Planmeca Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |