What is Medical DR System - Global Market?

The Medical DR System, or Digital Radiography System, is a cutting-edge technology used in the medical field for capturing digital images of the internal structures of the body. Unlike traditional X-ray systems that use film, DR systems utilize digital sensors to produce high-quality images instantly. This advancement not only enhances the clarity and detail of the images but also significantly reduces the time required for image processing. The global market for Medical DR Systems is expanding rapidly due to the increasing demand for advanced diagnostic tools in healthcare. Factors such as the rising prevalence of chronic diseases, advancements in medical imaging technology, and the growing need for efficient and accurate diagnostic procedures are driving this growth. Additionally, the shift towards digital healthcare solutions and the integration of artificial intelligence in imaging systems are further propelling the market. As healthcare providers seek to improve patient outcomes and streamline operations, the adoption of Medical DR Systems is becoming increasingly prevalent worldwide. This trend is expected to continue as more healthcare facilities recognize the benefits of digital radiography in enhancing diagnostic accuracy and patient care.

Mobile DR System, Fixed DR System in the Medical DR System - Global Market:

Mobile DR Systems and Fixed DR Systems are two primary categories within the Medical DR System market, each serving distinct purposes and offering unique advantages. Mobile DR Systems are designed for flexibility and convenience, allowing healthcare professionals to perform radiographic examinations at the patient's bedside or in various locations within a healthcare facility. These systems are particularly beneficial in emergency rooms, intensive care units, and during surgical procedures where immediate imaging is required. The portability of Mobile DR Systems ensures that patients who are unable to be moved can still receive timely and accurate diagnostic imaging. These systems are equipped with wireless capabilities, enabling seamless integration with hospital networks and electronic medical records. This connectivity facilitates quick access to patient data and enhances the efficiency of the diagnostic process. On the other hand, Fixed DR Systems are stationary units typically installed in dedicated radiology departments. These systems are known for their superior image quality and advanced imaging capabilities, making them ideal for comprehensive diagnostic evaluations. Fixed DR Systems are often equipped with larger detectors and more powerful imaging software, allowing for detailed examinations of complex anatomical structures. They are commonly used in specialized medical fields such as orthopedics, cardiology, and oncology, where precise imaging is crucial for accurate diagnosis and treatment planning. The choice between Mobile and Fixed DR Systems depends on the specific needs of the healthcare facility and the types of examinations performed. While Mobile DR Systems offer the advantage of mobility and rapid deployment, Fixed DR Systems provide unparalleled image quality and advanced diagnostic features. Both systems play a vital role in modern healthcare, contributing to improved patient outcomes and streamlined clinical workflows. As the demand for efficient and accurate diagnostic imaging continues to grow, the adoption of both Mobile and Fixed DR Systems is expected to increase, further driving the expansion of the Medical DR System market globally.

Dental, Orthopedics, General Surgery, Veterinarian, Others in the Medical DR System - Global Market:

The usage of Medical DR Systems spans various medical fields, each benefiting from the enhanced imaging capabilities and efficiency these systems provide. In the field of dentistry, DR Systems are used to capture detailed images of teeth, gums, and jaw structures, aiding in the diagnosis and treatment of dental conditions. The high-resolution images produced by DR Systems allow dentists to detect cavities, fractures, and other abnormalities with greater accuracy, leading to more effective treatment plans. In orthopedics, DR Systems are essential for evaluating bone structures and joint conditions. The ability to produce clear and detailed images of bones and soft tissues enables orthopedic specialists to diagnose fractures, dislocations, and degenerative conditions accurately. This precision is crucial for developing effective treatment strategies and monitoring the progress of healing. General surgery also benefits from the use of Medical DR Systems, as they provide surgeons with real-time imaging during procedures. This capability allows for better visualization of the surgical area, enhancing the precision and safety of surgical interventions. In veterinary medicine, DR Systems are used to diagnose and monitor conditions in animals, providing veterinarians with the tools needed to deliver high-quality care. The versatility of DR Systems allows for their application in various species, from small pets to large livestock. Other areas where Medical DR Systems are utilized include emergency medicine, where rapid imaging is critical for assessing trauma and acute conditions, and pediatrics, where the reduced radiation exposure of DR Systems is particularly beneficial for young patients. The widespread adoption of Medical DR Systems across these diverse fields underscores their importance in modern healthcare, as they contribute to improved diagnostic accuracy, patient safety, and overall clinical efficiency.

Medical DR System - Global Market Outlook:

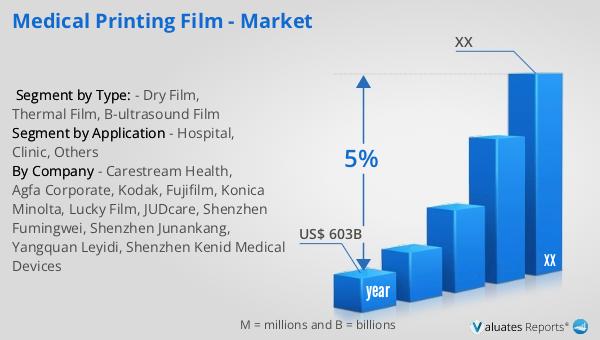

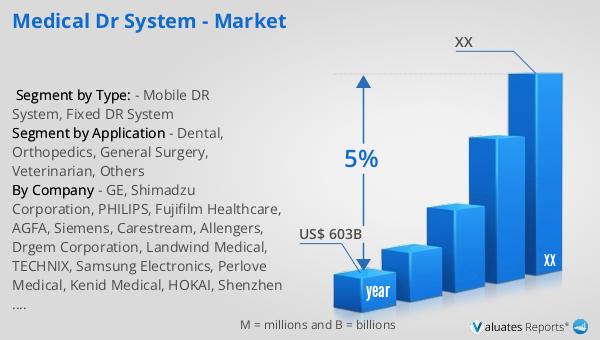

Our research indicates that the global market for medical devices, including Medical DR Systems, is projected to reach approximately $603 billion in 2023. This substantial market size reflects the growing demand for advanced medical technologies and the continuous innovation within the healthcare sector. Over the next six years, the market is expected to grow at a compound annual growth rate (CAGR) of 5%. This steady growth trajectory highlights the increasing reliance on medical devices to enhance patient care and improve healthcare outcomes. The expansion of the medical device market is driven by several factors, including the rising prevalence of chronic diseases, the aging global population, and the ongoing advancements in medical technology. As healthcare systems worldwide strive to provide more efficient and effective care, the adoption of innovative medical devices, such as Medical DR Systems, is becoming increasingly important. These devices play a crucial role in improving diagnostic accuracy, streamlining clinical workflows, and enhancing patient safety. The projected growth of the medical device market underscores the critical role that these technologies play in shaping the future of healthcare. As the market continues to evolve, the demand for cutting-edge medical devices is expected to rise, further driving innovation and development in the industry.

| Report Metric | Details |

| Report Name | Medical DR System - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | GE, Shimadzu Corporation, PHILIPS, Fujifilm Healthcare, AGFA, Siemens, Carestream, Allengers, Drgem Corporation, Landwind Medical, TECHNIX, Samsung Electronics, Perlove Medical, Kenid Medical, HOKAI, Shenzhen Browiner, Shanghai United Imaging Healthcare, Del Medical, Konica, Italray Srl, Wandong Meidcal, Shenzhen Angell Technology, Kodak, Mindray, JPI Healthcare, ALLPRO Imaging, Shanghai Electric Kangda, SHINVA, Shenzhen Lanmage, Shenzhen SONTU Medical Imaging Equipment |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |