What is Global All-In-One Motor Drivers Market?

The Global All-In-One Motor Drivers Market is a rapidly evolving sector that plays a crucial role in various industries by providing integrated solutions for motor control. These motor drivers are designed to simplify the process of controlling motors by integrating multiple functions into a single chip, which reduces the complexity and cost of motor control systems. They are used in a wide range of applications, from consumer electronics to industrial machinery, due to their efficiency and compact design. The market is driven by the increasing demand for automation and the need for energy-efficient solutions. As industries continue to adopt smart technologies, the demand for all-in-one motor drivers is expected to grow. These drivers support various types of motors, including brushed DC (BDC), brushless DC (BLDC), stepper motors (STM), and gate drivers, each catering to specific application needs. The integration of advanced features such as overcurrent protection, thermal shutdown, and diagnostic capabilities further enhances their appeal. As a result, the Global All-In-One Motor Drivers Market is poised for significant growth, driven by technological advancements and the increasing adoption of smart devices across various sectors.

BDC, BLDC, STM, Gate Driver in the Global All-In-One Motor Drivers Market:

In the Global All-In-One Motor Drivers Market, different types of motor drivers cater to specific needs and applications. Brushed DC (BDC) motor drivers are among the simplest and most cost-effective solutions available. They are widely used in applications where precise control is not critical, such as in toys, small appliances, and automotive applications. BDC motors are easy to control and provide a good balance between performance and cost. On the other hand, Brushless DC (BLDC) motor drivers offer higher efficiency and reliability compared to BDC motors. They are commonly used in applications that require precise control and high efficiency, such as in drones, electric vehicles, and industrial automation. BLDC motors have a longer lifespan and require less maintenance, making them ideal for applications where reliability is crucial. Stepper Motor (STM) drivers are used in applications that require precise positioning and control, such as in 3D printers, CNC machines, and robotics. They offer excellent control over motor position and speed, making them suitable for applications that require high precision. Gate drivers are used to control power transistors in high-power applications. They are essential in applications that require high-speed switching and efficient power management, such as in power supplies, inverters, and motor control systems. Gate drivers ensure that power transistors operate efficiently and reliably, reducing power loss and improving overall system performance. Each type of motor driver has its unique advantages and is chosen based on the specific requirements of the application. The integration of these drivers into all-in-one solutions simplifies the design process and reduces the overall cost of motor control systems. As the demand for smart and energy-efficient solutions continues to grow, the Global All-In-One Motor Drivers Market is expected to expand, offering innovative solutions for a wide range of applications.

Smart Home, Intelligent Three-ammeters (Water, Electricity and Gas Meter), 3D Printer, Massage Equip, Others in the Global All-In-One Motor Drivers Market:

The Global All-In-One Motor Drivers Market finds extensive usage in various areas, including smart homes, intelligent three-ammeters, 3D printers, massage equipment, and more. In smart homes, these motor drivers are used to control various devices such as automated blinds, smart locks, and HVAC systems. They enable seamless integration and control of these devices, enhancing the overall smart home experience. The ability to control multiple devices with a single driver simplifies the design and reduces the cost of smart home systems. In intelligent three-ammeters, which include water, electricity, and gas meters, all-in-one motor drivers play a crucial role in ensuring accurate measurement and control. They enable precise control of the metering mechanisms, ensuring accurate readings and efficient operation. This is particularly important in smart grid applications, where accurate data collection and control are essential for efficient energy management. In 3D printers, all-in-one motor drivers are used to control the stepper motors that drive the printer's axes. They provide precise control over the motor's position and speed, ensuring accurate and high-quality prints. The integration of advanced features such as microstepping and current control enhances the performance of 3D printers, making them more efficient and reliable. In massage equipment, these motor drivers are used to control the motors that drive the massage mechanisms. They enable smooth and precise control of the massage movements, enhancing the overall user experience. The ability to integrate multiple functions into a single driver simplifies the design and reduces the cost of massage equipment. Other applications of all-in-one motor drivers include robotics, automotive systems, and industrial automation. In each of these areas, the integration of multiple functions into a single driver simplifies the design, reduces the cost, and enhances the performance of the system. As the demand for smart and energy-efficient solutions continues to grow, the Global All-In-One Motor Drivers Market is expected to expand, offering innovative solutions for a wide range of applications.

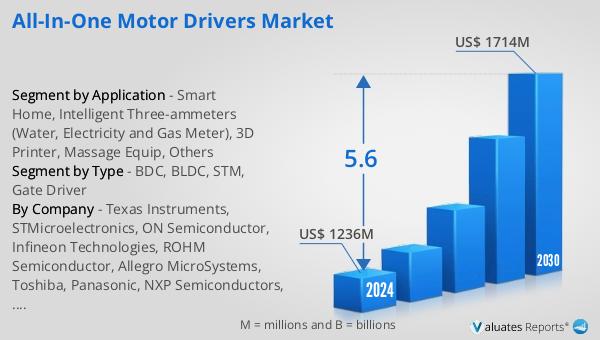

Global All-In-One Motor Drivers Market Outlook:

The global All-In-One Motor Drivers market is anticipated to expand from $1,236 million in 2024 to $1,714 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 5.6% over the forecast period. This growth is indicative of the increasing demand for integrated motor control solutions across various industries. Meanwhile, the global semiconductor market, which was valued at $579 billion in 2022, is projected to reach $790 billion by 2029, growing at a CAGR of 6% during the same period. This growth in the semiconductor market underscores the rising demand for advanced electronic components, including motor drivers. In terms of regional sales, the Americas reported sales of $142.1 billion, marking a 17.0% increase year-on-year. Europe saw sales of $53.8 billion, up 12.6% year-on-year, while Japan recorded sales of $48.1 billion, reflecting a 10.0% increase year-on-year. These figures highlight the robust growth and increasing adoption of semiconductor technologies across different regions, driven by advancements in technology and the growing need for efficient and reliable electronic components. As industries continue to embrace automation and smart technologies, the demand for all-in-one motor drivers is expected to rise, contributing to the overall growth of the market.

| Report Metric | Details |

| Report Name | All-In-One Motor Drivers Market |

| Accounted market size in 2024 | US$ 1236 in million |

| Forecasted market size in 2030 | US$ 1714 million |

| CAGR | 5.6 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Texas Instruments, STMicroelectronics, ON Semiconductor, Infineon Technologies, ROHM Semiconductor, Allegro MicroSystems, Toshiba, Panasonic, NXP Semiconductors, Maxim Integrated, Microchip Technology, Diodes Incorporated, Melexis, New Japan Radio, Fortior Tech, ICOFCHINA, Dialog Semiconductor, H&M Semiconductor, Trinamic, MPS, Diodes |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |