What is Global Rackmount IPC Market?

The Global Rackmount IPC Market refers to the industry focused on the production and distribution of rack-mounted industrial personal computers (IPCs). These specialized computers are designed to be mounted in standardized racks, which are commonly used in data centers and industrial environments. Rackmount IPCs are essential for applications that require robust computing power, reliability, and the ability to operate in challenging conditions. They are often used in sectors such as telecommunications, manufacturing, and automation, where they support critical operations by providing processing power for data analysis, control systems, and network management. The market for these devices is driven by the increasing demand for efficient data processing and storage solutions, as well as the need for systems that can withstand harsh industrial environments. As industries continue to digitize and automate their processes, the demand for rackmount IPCs is expected to grow, making this market an important component of the broader industrial computing landscape.

1U Rackmount Chassis, 2U Rackmount Chassis, 4U Rackmount Chassis in the Global Rackmount IPC Market:

In the Global Rackmount IPC Market, different sizes of rackmount chassis are available to meet various needs, including 1U, 2U, and 4U chassis. The "U" in these terms stands for "rack unit," which is a measure of vertical space in a rack. A 1U rackmount chassis is the smallest, occupying just 1.75 inches of vertical space. These compact units are ideal for environments where space is at a premium, such as in small data centers or server rooms. Despite their size, 1U chassis can house powerful computing components, making them suitable for applications that require high performance in a limited space. They are often used in network management, telecommunications, and small-scale industrial automation tasks.

Industrial, Commercial in the Global Rackmount IPC Market:

A 2U rackmount chassis, on the other hand, offers more space, occupying 3.5 inches of vertical rack space. This additional space allows for more powerful hardware configurations, including larger cooling systems and additional storage options. As a result, 2U chassis are often used in applications that require more processing power and storage capacity than a 1U chassis can provide. They are commonly found in medium-sized data centers and are used for tasks such as data processing, virtualization, and complex industrial control systems. The increased space also allows for better heat dissipation, which is crucial for maintaining system stability and performance in demanding environments.

Global Rackmount IPC Market Outlook:

The 4U rackmount chassis is the largest of the three, taking up 7 inches of vertical space in a rack. This size provides ample room for high-performance components, extensive storage solutions, and advanced cooling systems. 4U chassis are typically used in large-scale industrial applications and data centers where maximum performance and reliability are required. They can accommodate multiple processors, large amounts of RAM, and numerous hard drives, making them ideal for tasks such as big data analysis, cloud computing, and large-scale automation projects. The robust design of 4U chassis ensures they can handle the most demanding workloads while maintaining optimal performance and reliability.

| Report Metric | Details |

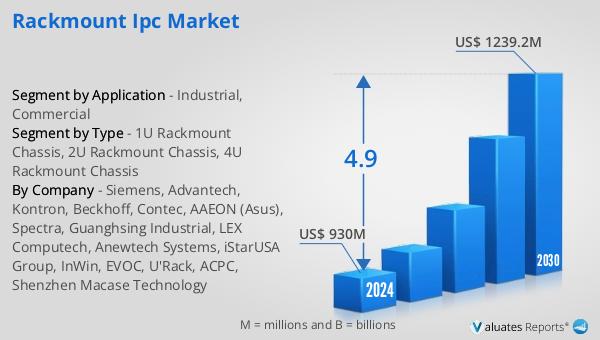

| Report Name | Rackmount IPC Market |

| Accounted market size in 2024 | US$ 930 million |

| Forecasted market size in 2030 | US$ 1239.2 million |

| CAGR | 4.9 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Siemens, Advantech, Kontron, Beckhoff, Contec, AAEON (Asus), Spectra, Guanghsing Industrial, LEX Computech, Anewtech Systems, iStarUSA Group, InWin, EVOC, U'Rack, ACPC, Shenzhen Macase Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |