What is Organic Phosphinate Flame Retardant - Global Market?

Organic phosphinate flame retardants are specialized chemicals used to enhance the fire resistance of various materials. These compounds are particularly valued for their ability to inhibit or slow down the spread of fire, making them crucial in industries where safety is paramount. The global market for organic phosphinate flame retardants is driven by increasing safety regulations and the growing demand for fire-resistant materials across various sectors. These flame retardants are primarily used in polymers and plastics, which are prevalent in numerous applications, from electronics to construction. The market is characterized by continuous research and development efforts aimed at improving the efficiency and environmental impact of these compounds. As industries strive to meet stringent safety standards, the demand for effective flame retardants like organic phosphinates is expected to rise. This market is also influenced by the push towards sustainable and non-toxic flame retardants, as consumers and regulators alike become more environmentally conscious. Overall, the organic phosphinate flame retardant market is poised for growth, driven by technological advancements and the increasing need for fire safety across various industries.

Phosphate, Phosphite in the Organic Phosphinate Flame Retardant - Global Market:

Phosphate and phosphite compounds are integral to the organic phosphinate flame retardant market, each playing a unique role in enhancing fire resistance. Phosphates are widely used due to their ability to form a protective char layer on the surface of materials when exposed to heat. This char layer acts as a barrier, slowing down the release of flammable gases and reducing the spread of flames. Phosphates are particularly effective in applications where long-term fire resistance is required, such as in construction materials and textiles. On the other hand, phosphites are known for their ability to scavenge free radicals, which are highly reactive species that can propagate the combustion process. By neutralizing these radicals, phosphites help to interrupt the chemical reactions that sustain a fire, thereby enhancing the flame-retardant properties of materials. In the global market, the demand for phosphate and phosphite-based flame retardants is driven by their effectiveness and versatility. These compounds are used in a wide range of applications, from electronics to automotive components, where fire safety is a critical concern. The market is also influenced by regulatory trends, as governments around the world implement stricter fire safety standards. This has led to increased research and development efforts aimed at improving the performance and environmental profile of phosphate and phosphite flame retardants. Manufacturers are focusing on developing new formulations that offer enhanced fire resistance while minimizing environmental impact. This includes the use of bio-based phosphates and phosphites, which are derived from renewable sources and offer a more sustainable alternative to traditional flame retardants. The global market for phosphate and phosphite-based flame retardants is also characterized by regional variations in demand. In North America and Europe, the market is driven by stringent fire safety regulations and the growing demand for eco-friendly flame retardants. In Asia-Pacific, the market is fueled by rapid industrialization and urbanization, which are driving the demand for fire-resistant materials in construction and manufacturing. Overall, the market for phosphate and phosphite-based flame retardants is poised for growth, driven by technological advancements and the increasing need for fire safety across various industries. As the market evolves, manufacturers are likely to focus on developing innovative solutions that meet the changing needs of consumers and regulators alike.

Wire and Cable, Electronic and Electrical, Automobile, Construction, Others in the Organic Phosphinate Flame Retardant - Global Market:

Organic phosphinate flame retardants are used in a variety of applications, each with its own set of requirements and challenges. In the wire and cable industry, these flame retardants are used to enhance the fire resistance of insulation materials. This is crucial in preventing the spread of fire in buildings and industrial facilities, where electrical cables are often a source of ignition. Organic phosphinate flame retardants help to reduce the flammability of these materials, thereby improving safety and compliance with fire safety regulations. In the electronics and electrical sector, these flame retardants are used in the production of circuit boards, connectors, and other components. The use of flame retardants in these applications is essential to prevent electrical fires, which can cause significant damage and pose a risk to human life. Organic phosphinate flame retardants are valued for their ability to provide effective fire resistance without compromising the performance of electronic components. In the automotive industry, these flame retardants are used in the production of interior components, such as seats, dashboards, and door panels. The use of flame retardants in these applications is critical to ensure the safety of passengers in the event of a fire. Organic phosphinate flame retardants are particularly effective in automotive applications due to their ability to provide long-lasting fire resistance and durability. In the construction industry, these flame retardants are used in the production of building materials, such as insulation, roofing, and flooring. The use of flame retardants in these applications is essential to meet fire safety regulations and ensure the safety of occupants. Organic phosphinate flame retardants are valued for their ability to provide effective fire resistance while maintaining the structural integrity of building materials. In addition to these applications, organic phosphinate flame retardants are also used in other industries, such as textiles and furniture. In these applications, flame retardants are used to enhance the fire resistance of fabrics and upholstery, thereby improving safety and compliance with fire safety regulations. Overall, the use of organic phosphinate flame retardants is driven by the need for effective fire resistance across a wide range of applications. As industries continue to prioritize safety and compliance with fire safety regulations, the demand for these flame retardants is expected to grow.

Organic Phosphinate Flame Retardant - Global Market Outlook:

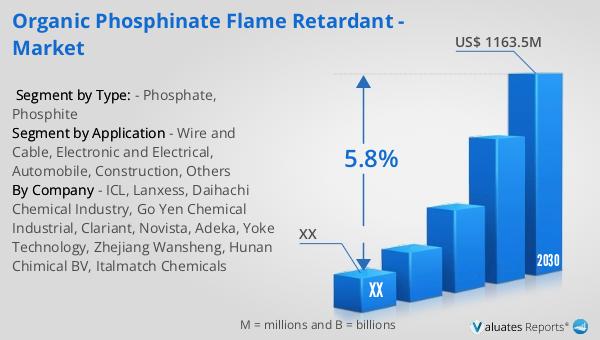

The global market for organic phosphinate flame retardants was valued at approximately $788.4 million in 2023. This market is projected to grow significantly, reaching an estimated size of $1,163.5 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 5.8% during the forecast period from 2024 to 2030. The North American market for organic phosphinate flame retardants is also anticipated to experience growth during this period. Although specific figures for the North American market in 2023 and 2030 are not provided, it is expected to follow a similar upward trend, driven by increasing demand for fire-resistant materials and stringent safety regulations. The growth of the global market for organic phosphinate flame retardants is influenced by several factors, including technological advancements, regulatory trends, and the increasing need for fire safety across various industries. As industries continue to prioritize safety and compliance with fire safety regulations, the demand for effective flame retardants like organic phosphinates is expected to rise. This market is also influenced by the push towards sustainable and non-toxic flame retardants, as consumers and regulators alike become more environmentally conscious. Overall, the organic phosphinate flame retardant market is poised for growth, driven by technological advancements and the increasing need for fire safety across various industries.

| Report Metric | Details |

| Report Name | Organic Phosphinate Flame Retardant - Market |

| Forecasted market size in 2030 | US$ 1163.5 million |

| CAGR | 5.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | ICL, Lanxess, Daihachi Chemical Industry, Go Yen Chemical Industrial, Clariant, Novista, Adeka, Yoke Technology, Zhejiang Wansheng, Hunan Chimical BV, Italmatch Chemicals |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |