What is Blood Testing Services - Global Market?

Blood testing services are a crucial component of the global healthcare market, providing essential diagnostic information that aids in the detection, diagnosis, and management of various health conditions. These services encompass a wide range of tests that analyze blood samples to assess health status, detect diseases, and monitor treatment efficacy. The global market for blood testing services is driven by factors such as the increasing prevalence of chronic diseases, advancements in technology, and the growing demand for early and accurate diagnosis. Blood tests are used to measure different components of the blood, including red and white blood cells, platelets, hemoglobin, and various enzymes and proteins. This information is vital for healthcare providers to make informed decisions about patient care. The market is also influenced by the rising awareness of preventive healthcare and the need for regular health check-ups. As a result, blood testing services are becoming more accessible and affordable, contributing to their widespread adoption across different regions. The integration of advanced technologies, such as automation and artificial intelligence, is further enhancing the efficiency and accuracy of blood testing services, making them an indispensable part of modern healthcare.

Screen, Test, Evaluate in the Blood Testing Services - Global Market:

The process of screening, testing, and evaluating through blood testing services is a comprehensive approach that plays a pivotal role in the global healthcare landscape. Screening involves the initial step of identifying individuals who may be at risk of certain health conditions. This is often done through routine blood tests that check for common markers of diseases such as diabetes, high cholesterol, or anemia. These screenings are crucial for early detection, allowing for timely intervention and management of potential health issues. Once a potential risk is identified, more specific tests are conducted to confirm the presence of a disease or condition. This testing phase is more detailed and may involve a series of tests to pinpoint the exact nature of the health problem. For instance, if a screening test indicates high blood sugar levels, further tests like the HbA1c test may be conducted to diagnose diabetes. The evaluation phase involves analyzing the results of these tests to determine the severity of the condition and to formulate a treatment plan. This phase is critical as it helps healthcare providers understand the patient's health status and make informed decisions about the best course of action. Blood testing services are not only used for diagnosing diseases but also for monitoring the effectiveness of treatments. For example, patients undergoing treatment for conditions like cancer or heart disease may require regular blood tests to assess how well their body is responding to the treatment. This ongoing evaluation helps in adjusting treatment plans as needed to achieve the best possible outcomes. The global market for blood testing services is expanding as more people recognize the importance of regular health screenings and the role they play in maintaining overall health. Technological advancements are also contributing to this growth by making blood tests more accurate, efficient, and accessible. Automated systems and artificial intelligence are being integrated into blood testing processes, reducing the chances of human error and speeding up the time it takes to get results. This is particularly important in emergency situations where quick diagnosis can be life-saving. Moreover, the rise of personalized medicine is driving demand for more specialized blood tests that can provide insights into an individual's unique health profile. These tests can help tailor treatments to the specific needs of a patient, improving the effectiveness of healthcare interventions. As the global population continues to grow and age, the demand for blood testing services is expected to increase, making it a vital component of the healthcare industry. The integration of digital health technologies is also transforming the way blood testing services are delivered, with telemedicine and remote monitoring becoming more prevalent. This allows patients to access blood testing services from the comfort of their homes, making healthcare more convenient and accessible. Overall, the process of screening, testing, and evaluating through blood testing services is a dynamic and evolving field that is essential for the early detection, diagnosis, and management of health conditions.

Hospital, Clinic, Research Institute, Commonweal Organizations in the Blood Testing Services - Global Market:

Blood testing services are utilized in various settings, including hospitals, clinics, research institutes, and commonweal organizations, each serving distinct purposes. In hospitals, blood tests are a fundamental part of patient care, used for diagnosing diseases, monitoring treatment progress, and assessing overall health. They are crucial in emergency departments where rapid diagnosis can be life-saving. Blood tests in hospitals are often comprehensive, covering a wide range of parameters to provide a complete picture of a patient's health. In clinics, blood testing services are typically used for routine health check-ups and preventive care. Clinics often serve as the first point of contact for patients seeking medical attention, and blood tests help in the early detection of potential health issues. This allows for timely intervention and management, reducing the risk of complications. Clinics may also offer specialized blood tests for conditions like diabetes, thyroid disorders, and cardiovascular diseases, providing patients with targeted care. Research institutes utilize blood testing services for scientific studies and clinical trials. Blood tests are essential for understanding the biological mechanisms of diseases, developing new treatments, and evaluating the efficacy of drugs. Researchers rely on blood tests to gather data on biomarkers, genetic information, and immune responses, contributing to advancements in medical science. Blood testing in research settings often involves cutting-edge technologies and methodologies, pushing the boundaries of what is possible in diagnostics and treatment. Commonweal organizations, such as public health agencies and non-profit organizations, use blood testing services to monitor and improve community health. These organizations often conduct blood testing campaigns to screen for infectious diseases, nutritional deficiencies, and other public health concerns. Blood tests help in identifying at-risk populations and implementing targeted interventions to address health disparities. Commonweal organizations also play a crucial role in raising awareness about the importance of regular blood testing and preventive healthcare. They often collaborate with healthcare providers and government agencies to ensure that blood testing services are accessible to underserved communities. In summary, blood testing services are integral to various sectors of the healthcare system, each utilizing these services to meet specific needs. Hospitals focus on comprehensive diagnostics and treatment monitoring, clinics emphasize preventive care and early detection, research institutes drive scientific advancements, and commonweal organizations work towards improving public health. The widespread use of blood testing services across these settings highlights their importance in maintaining and improving health outcomes globally.

Blood Testing Services - Global Market Outlook:

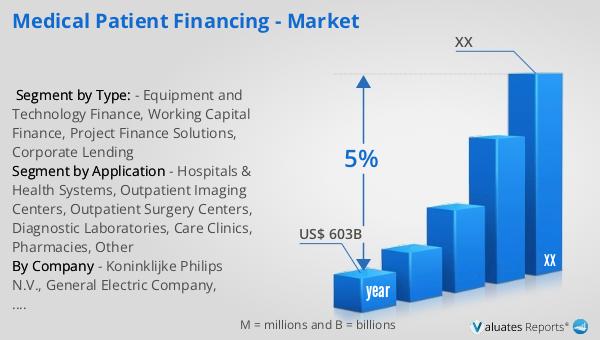

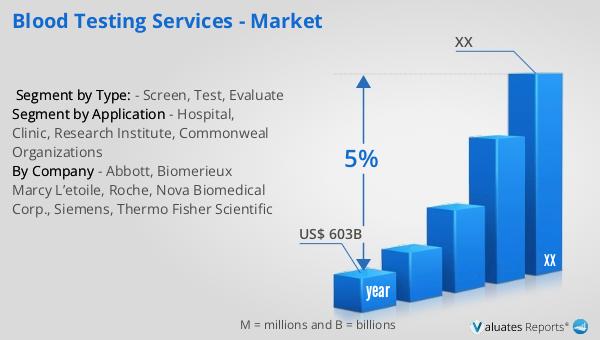

Our research indicates that the global market for medical devices, which includes blood testing services, is projected to reach approximately USD 603 billion in 2023. This market is expected to grow at a compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including the increasing prevalence of chronic diseases, advancements in medical technology, and the rising demand for early and accurate diagnosis. The medical device market encompasses a wide range of products, from diagnostic equipment to therapeutic devices, all of which play a crucial role in modern healthcare. Blood testing services, as a part of this market, are essential for diagnosing and managing various health conditions. The integration of advanced technologies, such as automation and artificial intelligence, is enhancing the efficiency and accuracy of blood testing services, contributing to their growing demand. Additionally, the shift towards personalized medicine is driving the need for more specialized blood tests that can provide insights into an individual's unique health profile. As the global population continues to grow and age, the demand for medical devices, including blood testing services, is expected to increase, making it a vital component of the healthcare industry. The market's growth is also supported by the increasing awareness of preventive healthcare and the need for regular health check-ups. As a result, blood testing services are becoming more accessible and affordable, contributing to their widespread adoption across different regions. Overall, the global market for medical devices, including blood testing services, is poised for significant growth in the coming years, driven by technological advancements and the increasing demand for quality healthcare.

| Report Metric | Details |

| Report Name | Blood Testing Services - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Abbott, Biomerieux Marcy L’etoile, Roche, Nova Biomedical Corp., Siemens, Thermo Fisher Scientific |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |