What is Digital Diabetes Care - Global Market?

Digital Diabetes Care is a rapidly evolving sector within the global healthcare market, focusing on the integration of digital technology to manage and treat diabetes more effectively. This market encompasses a wide range of products and services, including mobile applications, connected devices, and other digital tools designed to monitor blood glucose levels, provide personalized health insights, and facilitate communication between patients and healthcare providers. The primary goal of digital diabetes care is to enhance patient outcomes by enabling more precise and timely management of diabetes, ultimately reducing the risk of complications associated with the disease. As the prevalence of diabetes continues to rise globally, driven by factors such as aging populations and lifestyle changes, the demand for innovative digital solutions is increasing. These technologies not only empower patients to take control of their health but also offer healthcare professionals valuable data to tailor treatment plans more effectively. The global market for digital diabetes care is poised for significant growth as advancements in technology continue to drive innovation and improve accessibility for patients worldwide.

Apps, Connected Devices, Other in the Digital Diabetes Care - Global Market:

In the realm of digital diabetes care, mobile applications, connected devices, and other digital tools play a crucial role in transforming how diabetes is managed. Mobile applications are at the forefront, offering a range of functionalities that cater to both patients and healthcare providers. These apps often include features such as blood glucose tracking, medication reminders, dietary recommendations, and even virtual coaching. By providing real-time data and insights, these applications empower patients to make informed decisions about their health and lifestyle. Moreover, they facilitate seamless communication with healthcare professionals, enabling timely interventions and personalized care plans. Connected devices, such as continuous glucose monitors (CGMs) and smart insulin pens, are revolutionizing diabetes management by providing accurate and continuous data on blood glucose levels. These devices often sync with mobile apps, creating a comprehensive ecosystem that allows for real-time monitoring and analysis. CGMs, for instance, provide patients with a constant stream of glucose data, alerting them to potential highs or lows and enabling proactive management. Smart insulin pens, on the other hand, help ensure accurate dosing and track insulin usage, reducing the risk of errors and improving adherence to treatment plans. Other digital tools in the market include telemedicine platforms and wearable devices. Telemedicine has gained significant traction, especially in the wake of the COVID-19 pandemic, as it allows patients to consult with healthcare providers remotely. This is particularly beneficial for diabetes patients who require regular monitoring and adjustments to their treatment plans. Wearable devices, such as fitness trackers and smartwatches, also contribute to diabetes care by monitoring physical activity, heart rate, and other vital signs. These devices provide valuable data that can be integrated into diabetes management plans, helping patients maintain a healthy lifestyle. The integration of artificial intelligence and machine learning into digital diabetes care is another exciting development. These technologies enable predictive analytics, allowing for early detection of potential complications and personalized treatment recommendations. By analyzing vast amounts of data, AI-driven tools can identify patterns and trends that may not be immediately apparent to patients or healthcare providers. This level of insight can lead to more effective interventions and improved patient outcomes. Overall, the digital diabetes care market is characterized by a diverse range of products and services that cater to the unique needs of diabetes patients. As technology continues to advance, the potential for innovation in this field is immense, promising to enhance the quality of life for millions of individuals living with diabetes worldwide.

Diabetes, Obesity, High Blood Pressure, Depression in the Digital Diabetes Care - Global Market:

Digital diabetes care is not only transforming the management of diabetes but also addressing related health conditions such as obesity, high blood pressure, and depression. For diabetes, digital tools provide patients with the ability to monitor their blood glucose levels continuously, receive personalized feedback, and adjust their lifestyle and treatment plans accordingly. This proactive approach helps prevent complications and improves overall health outcomes. In the context of obesity, digital diabetes care solutions often include features that promote weight management through dietary tracking, exercise monitoring, and virtual coaching. By encouraging healthy habits and providing real-time feedback, these tools support patients in achieving and maintaining a healthy weight, which is crucial for managing diabetes effectively. High blood pressure, a common comorbidity in diabetes patients, can also be managed through digital solutions. Many digital diabetes care platforms offer blood pressure monitoring features, allowing patients to track their readings and identify trends over time. This data can be shared with healthcare providers, enabling timely interventions and adjustments to treatment plans. Additionally, lifestyle recommendations provided by these platforms, such as dietary changes and exercise routines, can help patients manage their blood pressure more effectively. Depression is another significant concern for individuals with diabetes, as the stress of managing a chronic condition can take a toll on mental health. Digital diabetes care solutions often include mental health support features, such as mood tracking, mindfulness exercises, and access to mental health professionals. By addressing the psychological aspects of diabetes management, these tools help patients maintain a positive outlook and improve their overall well-being. The integration of digital diabetes care into the management of these related conditions highlights the holistic approach that these technologies offer. By providing comprehensive support for both physical and mental health, digital diabetes care solutions empower patients to take control of their health and improve their quality of life. As the global market for digital diabetes care continues to grow, the potential for these technologies to address a wide range of health concerns is becoming increasingly apparent.

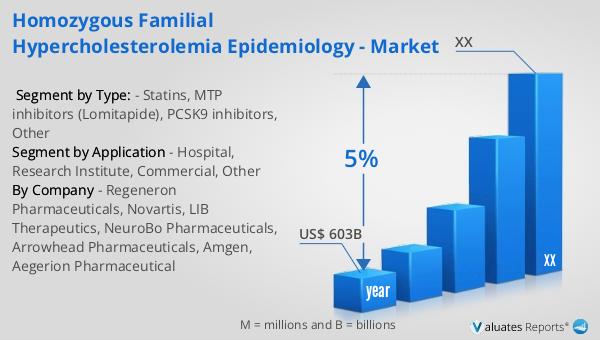

Digital Diabetes Care - Global Market Outlook:

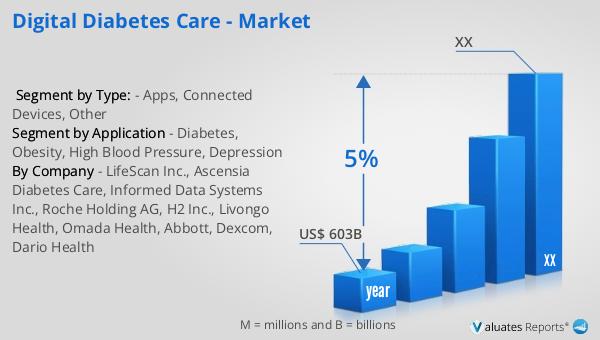

Our research indicates that the global market for medical devices, including digital diabetes care solutions, is projected to reach approximately $603 billion in 2023. This market is expected to experience a steady growth rate, with a compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including the increasing prevalence of chronic diseases such as diabetes, advancements in technology, and the growing demand for personalized healthcare solutions. As more individuals are diagnosed with diabetes and related conditions, the need for innovative and effective management tools becomes more critical. Digital diabetes care solutions, which encompass a wide range of products and services, are well-positioned to meet this demand by offering patients and healthcare providers the tools they need to manage the disease more effectively. The integration of digital technology into diabetes care not only enhances patient outcomes but also reduces healthcare costs by preventing complications and improving adherence to treatment plans. As the market continues to expand, the potential for digital diabetes care solutions to transform the healthcare landscape is immense, promising to improve the quality of life for millions of individuals worldwide.

| Report Metric | Details |

| Report Name | Digital Diabetes Care - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | LifeScan Inc., Ascensia Diabetes Care, Informed Data Systems Inc., Roche Holding AG, H2 Inc., Livongo Health, Omada Health, Abbott, Dexcom, Dario Health |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |