What is Chronic Graft-versus-host Disease (cGVHD) Treatment - Global Market?

Chronic Graft-versus-host Disease (cGVHD) is a complex condition that arises when donor cells attack the recipient's body following a stem cell or bone marrow transplant. This condition can affect various organs, including the skin, liver, and gastrointestinal tract, leading to significant morbidity and mortality. The global market for cGVHD treatment is driven by the increasing number of transplants and advancements in medical research. As of 2023, the market was valued at approximately US$ 1425 million and is projected to grow significantly by 2030. This growth is fueled by the development of novel therapies and an increasing understanding of the disease's pathophysiology. The market's expansion is also supported by the rising prevalence of hematological malignancies, which necessitate transplants. The treatment landscape for cGVHD is evolving, with a focus on improving patient outcomes and quality of life. This involves a multidisciplinary approach, combining pharmacological treatments with supportive care. The global market is characterized by a competitive landscape, with numerous pharmaceutical companies investing in research and development to introduce innovative therapies. The increasing awareness and diagnosis of cGVHD are expected to further drive market growth, making it a critical area of focus in the healthcare sector.

Corticosteroids, mTOR Inhibitors, Tyrosine Kinase Inhibitors, Monoclonal Antibodies, Others in the Chronic Graft-versus-host Disease (cGVHD) Treatment - Global Market:

Corticosteroids are often the first line of treatment for cGVHD due to their potent anti-inflammatory and immunosuppressive properties. They work by reducing the immune system's activity, thereby alleviating the symptoms of cGVHD. However, long-term use of corticosteroids can lead to significant side effects, such as osteoporosis, hypertension, and diabetes, which necessitates the development of alternative therapies. mTOR inhibitors, such as sirolimus, are another class of drugs used in cGVHD treatment. These drugs work by inhibiting the mTOR pathway, which plays a crucial role in cell growth and proliferation. By targeting this pathway, mTOR inhibitors help reduce the immune response and inflammation associated with cGVHD. Tyrosine kinase inhibitors (TKIs) are also gaining attention in the cGVHD treatment landscape. These drugs target specific enzymes involved in the signaling pathways that regulate cell division and survival. By inhibiting these enzymes, TKIs can help control the abnormal immune response seen in cGVHD. Monoclonal antibodies represent a more targeted approach to cGVHD treatment. These biologic agents are designed to bind to specific proteins on the surface of immune cells, thereby modulating their activity. For instance, rituximab, a monoclonal antibody targeting CD20, has shown promise in treating cGVHD by depleting B cells, which are implicated in the disease's pathogenesis. Other emerging therapies for cGVHD include JAK inhibitors, which target the Janus kinase signaling pathway involved in immune cell activation. These inhibitors have shown efficacy in reducing the symptoms of cGVHD and are being actively investigated in clinical trials. Additionally, extracorporeal photopheresis (ECP) is a non-pharmacological treatment option that involves the removal and treatment of blood cells outside the body to modulate the immune response. This therapy has been used successfully in patients with steroid-refractory cGVHD. The global market for cGVHD treatment is witnessing a shift towards personalized medicine, with a focus on tailoring therapies to individual patient profiles. This approach aims to optimize treatment efficacy while minimizing adverse effects. The development of biomarkers for cGVHD is also an area of active research, as these markers can help predict disease progression and response to therapy. Overall, the cGVHD treatment landscape is characterized by a diverse array of therapeutic options, each with its own mechanism of action and potential benefits. The ongoing research and development efforts in this field are expected to yield new and improved therapies, offering hope to patients affected by this challenging condition.

Hospitals Pharmacies, Retail Pharmacies, Online Pharmacies in the Chronic Graft-versus-host Disease (cGVHD) Treatment - Global Market:

The usage of cGVHD treatments varies across different types of pharmacies, each playing a crucial role in ensuring patient access to necessary medications. Hospitals pharmacies are integral to the management of cGVHD, as they are often the first point of contact for patients undergoing treatment. These pharmacies are equipped to handle complex medication regimens and provide specialized care tailored to the needs of cGVHD patients. Hospital pharmacists work closely with healthcare teams to ensure that patients receive the most appropriate therapies, monitor for potential drug interactions, and manage side effects. Retail pharmacies also play a significant role in the distribution of cGVHD treatments. These pharmacies provide a convenient option for patients to access their medications, particularly for those who require long-term therapy. Retail pharmacists are trained to offer counseling on medication adherence and management of side effects, ensuring that patients are well-informed about their treatment plans. The availability of cGVHD treatments in retail pharmacies helps improve accessibility for patients, particularly in areas where hospital pharmacies may not be readily accessible. Online pharmacies have emerged as a growing trend in the distribution of cGVHD treatments, offering patients the convenience of ordering medications from the comfort of their homes. This option is particularly beneficial for patients with mobility issues or those living in remote areas. Online pharmacies often provide detailed information about medications, including potential side effects and interactions, enabling patients to make informed decisions about their treatment. Additionally, many online pharmacies offer home delivery services, further enhancing accessibility for patients. The global market for cGVHD treatment is supported by a robust distribution network that includes hospitals, retail, and online pharmacies. Each of these channels plays a vital role in ensuring that patients have access to the medications they need to manage their condition effectively. The collaboration between healthcare providers and pharmacies is essential in optimizing treatment outcomes for cGVHD patients, as it facilitates the timely and efficient delivery of therapies. As the market for cGVHD treatment continues to grow, the role of pharmacies in supporting patient care is expected to become increasingly important.

Chronic Graft-versus-host Disease (cGVHD) Treatment - Global Market Outlook:

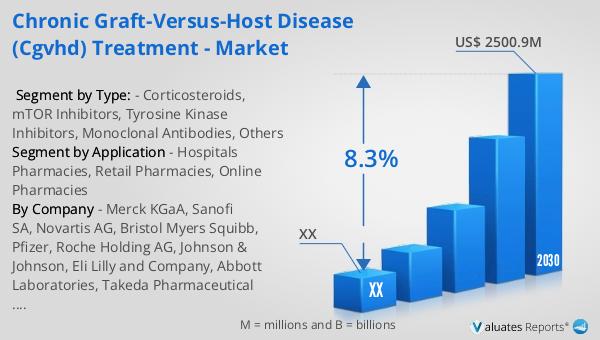

The global market for Chronic Graft-versus-host Disease (cGVHD) treatment was valued at approximately US$ 1425 million in 2023. It is anticipated to reach a revised size of US$ 2500.9 million by 2030, reflecting a compound annual growth rate (CAGR) of 8.3% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for effective cGVHD treatments and the ongoing advancements in therapeutic options. In comparison, the global pharmaceutical market was valued at US$ 1475 billion in 2022, with a projected CAGR of 5% over the next six years. This highlights the dynamic nature of the pharmaceutical industry, driven by innovation and the development of new therapies. The chemical drug market, a significant segment of the pharmaceutical industry, was estimated to grow from US$ 1005 billion in 2018 to US$ 1094 billion in 2022. This growth underscores the importance of chemical drugs in the overall pharmaceutical landscape, despite the increasing focus on biologics and personalized medicine. The cGVHD treatment market is a specialized segment within the broader pharmaceutical industry, characterized by its focus on addressing the unique challenges posed by this complex condition. The projected growth of the cGVHD treatment market reflects the increasing recognition of the need for targeted therapies and the ongoing efforts to improve patient outcomes. As the market continues to evolve, it is expected to play a significant role in shaping the future of the pharmaceutical industry.

| Report Metric | Details |

| Report Name | Chronic Graft-versus-host Disease (cGVHD) Treatment - Market |

| Forecasted market size in 2030 | US$ 2500.9 million |

| CAGR | 8.3% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Merck KGaA, Sanofi SA, Novartis AG, Bristol Myers Squibb, Pfizer, Roche Holding AG, Johnson & Johnson, Eli Lilly and Company, Abbott Laboratories, Takeda Pharmaceutical Company |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |