What is Metal Bonding Wire for LED and Semiconductor - Global Market?

Metal bonding wire is a crucial component in the global market for LEDs and semiconductors. These wires are used to connect the semiconductor chip to its external circuitry, ensuring the efficient transmission of electrical signals. The market for metal bonding wire is driven by the increasing demand for miniaturized electronic devices and advancements in semiconductor technology. As the electronics industry continues to evolve, the need for reliable and efficient bonding solutions becomes more critical. Metal bonding wires are typically made from materials like gold, silver, copper, and aluminum, each offering unique properties that cater to specific applications. Gold wires, for instance, are known for their excellent conductivity and resistance to corrosion, making them ideal for high-reliability applications. Silver wires offer similar benefits but at a lower cost. Copper wires are favored for their excellent electrical and thermal conductivity, while aluminum wires are lightweight and cost-effective. The global market for metal bonding wire is poised for growth as the demand for advanced electronic devices continues to rise. This growth is further fueled by the increasing adoption of LEDs in various applications, from consumer electronics to automotive lighting. As technology advances, the role of metal bonding wire in ensuring the performance and reliability of electronic devices becomes increasingly significant.

Golden Bonding Wire, Silver Bonding Wire, Copper Bonding Wire, Aluminum Bonding Wire in the Metal Bonding Wire for LED and Semiconductor - Global Market:

Golden bonding wire is a staple in the semiconductor and LED industries due to its superior electrical conductivity and resistance to oxidation. Gold's inherent properties make it an ideal choice for applications requiring high reliability and performance. It is often used in high-frequency and high-power devices where signal integrity is paramount. Despite its higher cost, the benefits of using gold bonding wire, such as its excellent bondability and long-term stability, often outweigh the expense, especially in critical applications. Silver bonding wire, on the other hand, offers a cost-effective alternative to gold while still providing excellent electrical conductivity. Silver's thermal conductivity is also noteworthy, making it suitable for applications where heat dissipation is a concern. However, silver is more prone to oxidation than gold, which can affect its long-term reliability. To mitigate this, silver bonding wires are often coated or alloyed with other materials to enhance their performance. Copper bonding wire has gained popularity due to its excellent electrical and thermal conductivity, coupled with its lower cost compared to gold and silver. Copper's mechanical strength also makes it suitable for fine-pitch applications, where wire diameter is a critical factor. However, copper is more susceptible to oxidation, which can impact its performance over time. To address this, copper wires are often coated or used in controlled environments to prevent degradation. Aluminum bonding wire is another cost-effective option, known for its lightweight and corrosion-resistant properties. It is commonly used in power devices and applications where weight is a concern. Aluminum's lower melting point compared to other metals can be a limitation in high-temperature applications, but its affordability and availability make it a popular choice in many sectors. Each type of metal bonding wire offers distinct advantages and challenges, and the choice of wire often depends on the specific requirements of the application, including cost, performance, and environmental considerations. As the global market for LEDs and semiconductors continues to expand, the demand for these diverse bonding wire solutions is expected to grow, driven by the need for efficient and reliable electronic components.

Semiconductor Separate Components, Lighting Diode (LED), Integrated Circuit, Others in the Metal Bonding Wire for LED and Semiconductor - Global Market:

Metal bonding wires play a vital role in various applications within the LED and semiconductor industries. In semiconductor separate components, these wires are used to connect individual semiconductor devices, such as diodes and transistors, to their respective circuits. This connection is crucial for the proper functioning of the device, as it ensures the efficient transmission of electrical signals. The choice of bonding wire material can significantly impact the performance and reliability of these components, with factors such as conductivity, thermal performance, and mechanical strength being key considerations. In the realm of lighting diodes (LEDs), metal bonding wires are essential for connecting the LED chip to its package. This connection is critical for the efficient operation of the LED, as it affects both the electrical and thermal performance of the device. The use of high-quality bonding wires can enhance the brightness and longevity of LEDs, making them more appealing for a wide range of applications, from consumer electronics to automotive lighting. Integrated circuits (ICs) also rely heavily on metal bonding wires for their operation. These wires connect the various components within the IC, ensuring the seamless transmission of electrical signals between them. The choice of bonding wire material can influence the overall performance of the IC, with factors such as signal integrity, power consumption, and thermal management being key considerations. In addition to these specific applications, metal bonding wires are used in a variety of other areas within the semiconductor and LED industries. These include applications such as sensors, power devices, and microelectromechanical systems (MEMS), where the reliability and performance of the bonding wire are critical to the overall functionality of the device. As the demand for advanced electronic devices continues to grow, the importance of metal bonding wires in ensuring the performance and reliability of these devices cannot be overstated. The global market for metal bonding wire is poised for growth, driven by the increasing adoption of LEDs and semiconductors in various applications.

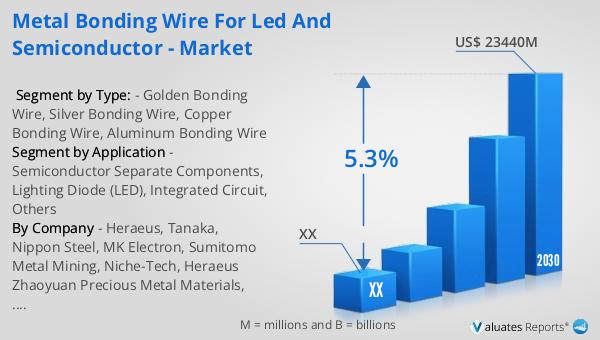

Metal Bonding Wire for LED and Semiconductor - Global Market Outlook:

The global market for metal bonding wire used in LEDs and semiconductors was valued at approximately $16.24 billion in 2023. This market is projected to grow to a revised size of $23.44 billion by 2030, reflecting a compound annual growth rate (CAGR) of 5.3% over the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for advanced electronic devices and the critical role that metal bonding wires play in their functionality. In parallel, the semiconductor market was estimated at $579 billion in 2022 and is expected to reach $790 billion by 2029, growing at a CAGR of 6% during the forecast period. This growth underscores the expanding applications of semiconductors across various industries, from consumer electronics to automotive and industrial sectors. The increasing complexity and miniaturization of electronic devices are driving the demand for reliable and efficient bonding solutions, further fueling the growth of the metal bonding wire market. As technology continues to advance, the importance of metal bonding wires in ensuring the performance and reliability of electronic devices will only become more pronounced. This growth trajectory highlights the critical role that metal bonding wires play in the global electronics industry and their potential for continued expansion in the coming years.

| Report Metric | Details |

| Report Name | Metal Bonding Wire for LED and Semiconductor - Market |

| Forecasted market size in 2030 | US$ 23440 million |

| CAGR | 5.3% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Heraeus, Tanaka, Nippon Steel, MK Electron, Sumitomo Metal Mining, Niche-Tech, Heraeus Zhaoyuan Precious Metal Materials, Ningbo Kangqiang Electronics, Yantai Zhaojin Kanfort Precious Metals Incorporated Company, Yantai Yesno Electronic Materials, Bejing Doublink Solders, Shanghai Wonsung Alloy Material, Shanghai Matfron Technology, Jiangsu Jincan Electronics Technology, Shangdong Ke Da Ding Xin Electronic Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |