What is Biotechnological Breeding - Global Market?

Biotechnological breeding refers to the application of advanced biological techniques to enhance the genetic makeup of plants and animals, aiming to improve their traits for agricultural and industrial purposes. This global market is driven by the increasing demand for food security, sustainable agriculture, and the need to address climate change challenges. Biotechnological breeding encompasses various methods such as genetic engineering, molecular breeding, and genome editing, which allow for precise modifications in the genetic material of organisms. These techniques enable the development of crops and livestock with improved yield, resistance to diseases and pests, and adaptability to environmental stresses. The global market for biotechnological breeding is expanding as more countries recognize the potential of these technologies to revolutionize agriculture and meet the growing food demands of the world's population. As a result, investments in research and development, along with supportive government policies, are propelling the growth of this market, making it a crucial component of modern agriculture.

Hybrid Breeding, Molecular Breeding, Genetic Engineering, Genome Editing in the Biotechnological Breeding - Global Market:

Hybrid breeding, molecular breeding, genetic engineering, and genome editing are key components of the biotechnological breeding market, each offering unique advantages and applications. Hybrid breeding involves the cross-breeding of two genetically distinct plants or animals to produce offspring with desirable traits from both parents. This method has been used for centuries to improve crop yields and livestock productivity. However, it is a time-consuming process that relies on natural genetic variation. Molecular breeding, on the other hand, utilizes molecular biology tools to identify and select specific genes associated with desired traits. This approach accelerates the breeding process by allowing breeders to focus on genetic markers linked to traits such as disease resistance, drought tolerance, and improved nutritional content. Genetic engineering takes a more direct approach by introducing or modifying specific genes within an organism's genome. This technique has been instrumental in developing genetically modified organisms (GMOs) that exhibit enhanced traits, such as herbicide resistance or increased nutritional value. Genome editing, particularly through technologies like CRISPR-Cas9, offers unprecedented precision in altering an organism's DNA. It allows for targeted modifications, enabling the correction of genetic defects or the introduction of new traits without the need for foreign DNA. These biotechnological breeding methods are transforming agriculture by providing tools to address challenges such as climate change, food security, and sustainable farming practices. As the global market for biotechnological breeding continues to grow, these technologies are expected to play a pivotal role in shaping the future of agriculture, offering solutions that are both innovative and sustainable.

Cereals, Fruits & Vegetables, Oilseeds & Pulses, Others in the Biotechnological Breeding - Global Market:

The application of biotechnological breeding in various agricultural sectors is revolutionizing the way we produce food and other essential crops. In the realm of cereals, biotechnological breeding techniques are being used to develop varieties that are more resistant to diseases, pests, and environmental stresses such as drought and salinity. This is crucial for ensuring food security, as cereals like rice, wheat, and maize are staple foods for a large portion of the global population. By enhancing the resilience and yield of these crops, biotechnological breeding helps to stabilize food supplies and reduce the risk of shortages. In the fruits and vegetables sector, biotechnological breeding is employed to improve the nutritional content, shelf life, and taste of produce. Techniques such as genetic engineering and genome editing allow for the development of fruits and vegetables with higher levels of vitamins and antioxidants, as well as improved resistance to spoilage and pathogens. This not only benefits consumers by providing healthier food options but also reduces food waste and increases the profitability of farmers. For oilseeds and pulses, biotechnological breeding focuses on enhancing oil content, protein quality, and resistance to biotic and abiotic stresses. This is particularly important for crops like soybeans, canola, and lentils, which are key sources of vegetable oils and plant-based proteins. By improving the quality and yield of these crops, biotechnological breeding supports the growing demand for plant-based foods and biofuels. Additionally, biotechnological breeding is applied to other crops such as fiber plants, medicinal herbs, and ornamental plants, where it helps to improve traits like fiber strength, active compound content, and aesthetic appeal. Overall, the use of biotechnological breeding across these diverse agricultural sectors is driving innovation and sustainability, ensuring that we can meet the needs of a growing global population while minimizing the environmental impact of farming.

Biotechnological Breeding - Global Market Outlook:

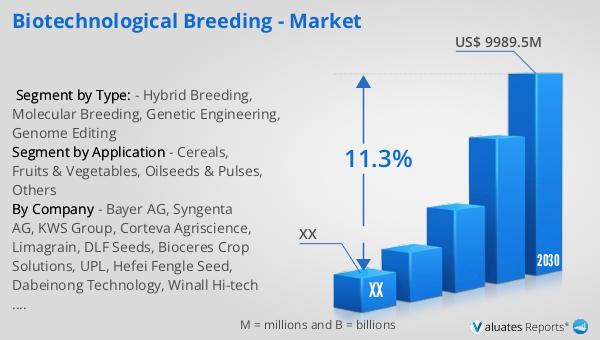

The global market for biotechnological breeding was valued at approximately $4,792 million in 2023, with projections indicating a significant expansion to around $9,989.5 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 11.3% from 2024 to 2030. The North American segment of this market also shows promising potential, although specific figures for 2023 and 2030 are not provided. The anticipated growth in this region is driven by advancements in biotechnological breeding techniques and increasing investments in agricultural biotechnology. The market's expansion is fueled by the rising demand for improved crop varieties and livestock breeds that can withstand environmental challenges and meet the nutritional needs of a growing population. As countries across the globe recognize the importance of sustainable agriculture and food security, the adoption of biotechnological breeding methods is expected to rise, further propelling market growth. This market outlook underscores the critical role that biotechnological breeding plays in modern agriculture, offering innovative solutions to enhance productivity and sustainability in the face of global challenges.

| Report Metric | Details |

| Report Name | Biotechnological Breeding - Market |

| Forecasted market size in 2030 | US$ 9989.5 million |

| CAGR | 11.3% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Bayer AG, Syngenta AG, KWS Group, Corteva Agriscience, Limagrain, DLF Seeds, Bioceres Crop Solutions, UPL, Hefei Fengle Seed, Dabeinong Technology, Winall Hi-tech Seed, Yuan Longping High-tech Agriculture, Shennong Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |