What is Microwave Ceramic Chip Capacitors - Global Market?

Microwave ceramic chip capacitors are essential components in the global electronics market, playing a crucial role in various high-frequency applications. These capacitors are designed to store and release electrical energy in circuits, and their ceramic material allows them to operate efficiently at microwave frequencies. The global market for these capacitors is driven by their widespread use in telecommunications, aerospace, defense, and consumer electronics. As technology advances, the demand for smaller, more efficient, and higher-performing electronic components increases, propelling the growth of the microwave ceramic chip capacitors market. These capacitors are valued for their stability, reliability, and ability to function in extreme conditions, making them indispensable in modern electronic systems. The market is characterized by continuous innovation, with manufacturers striving to enhance the performance and reduce the size of these components to meet the evolving needs of various industries. As a result, the microwave ceramic chip capacitors market is poised for significant growth, driven by technological advancements and the increasing demand for high-frequency electronic devices.

Universal, Array Type, Multi-Electrode Type, Others in the Microwave Ceramic Chip Capacitors - Global Market:

In the realm of microwave ceramic chip capacitors, several types cater to different applications and requirements, including universal, array type, multi-electrode type, and others. Universal capacitors are versatile components used across a wide range of applications due to their general-purpose nature. They are designed to meet the basic requirements of most electronic circuits, providing reliable performance in various environments. These capacitors are often used in consumer electronics, telecommunications, and automotive industries, where they help stabilize voltage and filter noise in circuits. Array type capacitors, on the other hand, are designed to offer multiple capacitors in a single package, providing space-saving solutions for complex circuits. They are particularly useful in applications where board space is limited, such as in mobile devices and compact electronic systems. By integrating multiple capacitors into one package, array type capacitors reduce the overall footprint of the circuit, making them ideal for modern, miniaturized electronic devices. Multi-electrode type capacitors are engineered to provide enhanced performance by incorporating multiple electrodes within a single capacitor. This design allows for increased capacitance and improved frequency response, making them suitable for high-frequency applications such as RF and microwave circuits. These capacitors are often used in telecommunications and aerospace industries, where high performance and reliability are critical. Other types of microwave ceramic chip capacitors include specialized designs tailored for specific applications, such as high-voltage capacitors for power electronics or temperature-compensating capacitors for precision circuits. Each type of capacitor offers unique benefits and is chosen based on the specific requirements of the application, ensuring optimal performance and reliability in electronic systems. As the demand for advanced electronic devices continues to grow, the market for microwave ceramic chip capacitors is expected to expand, driven by the need for innovative solutions that meet the diverse needs of various industries.

Aerospace, Weaponry, 5G Communication, Optical Communication Equipment in the Microwave Ceramic Chip Capacitors - Global Market:

Microwave ceramic chip capacitors are integral to several high-tech industries, including aerospace, weaponry, 5G communication, and optical communication equipment. In the aerospace sector, these capacitors are used in various systems, including radar, navigation, and communication equipment. Their ability to operate reliably in extreme temperatures and high-vibration environments makes them ideal for aerospace applications, where performance and reliability are paramount. In weaponry, microwave ceramic chip capacitors are used in advanced guidance systems, electronic warfare equipment, and communication devices. Their high-frequency capabilities and robust design ensure that they can withstand the harsh conditions often encountered in military applications. The advent of 5G communication technology has further increased the demand for these capacitors, as they are essential components in the infrastructure that supports high-speed data transmission. In 5G networks, microwave ceramic chip capacitors are used in base stations, antennas, and other critical components to ensure efficient signal processing and transmission. Similarly, in optical communication equipment, these capacitors play a vital role in maintaining signal integrity and reducing noise in high-speed data transmission systems. Their ability to handle high frequencies and provide stable performance makes them indispensable in the rapidly evolving field of optical communications. As these industries continue to advance, the demand for microwave ceramic chip capacitors is expected to grow, driven by the need for reliable, high-performance components that can meet the challenges of modern technology.

Microwave Ceramic Chip Capacitors - Global Market Outlook:

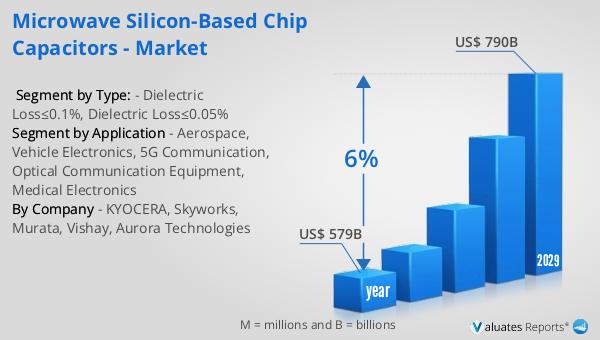

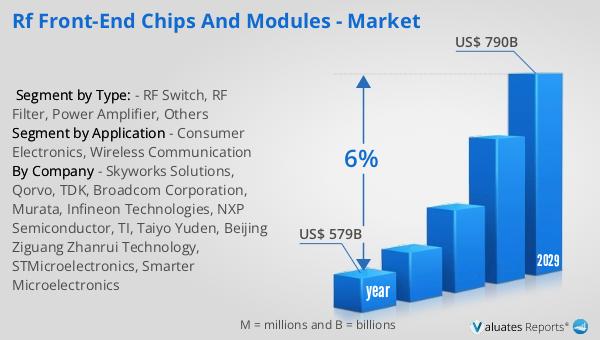

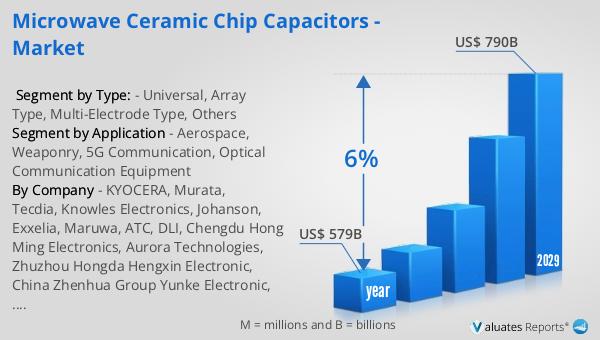

The global semiconductor market, which includes microwave ceramic chip capacitors, was valued at approximately US$ 579 billion in 2022. This market is projected to grow significantly, reaching an estimated value of US$ 790 billion by 2029. This growth represents a compound annual growth rate (CAGR) of 6% over the forecast period. The expansion of the semiconductor market is driven by the increasing demand for electronic devices across various industries, including telecommunications, consumer electronics, automotive, and industrial applications. As technology continues to evolve, the need for more advanced and efficient semiconductor components, such as microwave ceramic chip capacitors, is expected to rise. These components are crucial for the development of high-frequency electronic devices, which are becoming increasingly prevalent in today's digital world. The growth of the semiconductor market is also supported by ongoing research and development efforts aimed at enhancing the performance and reducing the size of electronic components. As a result, the market for microwave ceramic chip capacitors is poised for significant growth, driven by the increasing demand for high-performance electronic devices and the continuous advancement of semiconductor technology.

| Report Metric | Details |

| Report Name | Microwave Ceramic Chip Capacitors - Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2024 - 2029 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | KYOCERA, Murata, Tecdia, Knowles Electronics, Johanson, Exxelia, Maruwa, ATC, DLI, Chengdu Hong Ming Electronics, Aurora Technologies, Zhuzhou Hongda Hengxin Electronic, China Zhenhua Group Yunke Electronic, Hongke Electronic Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |