What is Global Vehicle Display OCA Optical Adhesive Market?

The Global Vehicle Display OCA Optical Adhesive Market is a specialized segment within the broader automotive and adhesive industries, focusing on the use of optical clear adhesives (OCA) in vehicle displays. These adhesives are crucial for bonding display components, such as touchscreens and instrument panels, to ensure clarity, durability, and functionality. As vehicles become more technologically advanced, with features like infotainment systems and digital dashboards, the demand for high-quality display adhesives has increased. OCA adhesives are preferred due to their excellent optical properties, which enhance display visibility and performance. They also offer benefits like resistance to yellowing, high transparency, and strong adhesion, making them ideal for automotive applications. The market is driven by the growing adoption of advanced display technologies in vehicles, as well as the increasing consumer demand for enhanced in-car experiences. As a result, manufacturers are investing in research and development to create innovative adhesive solutions that meet the evolving needs of the automotive industry. This market is expected to grow significantly as more vehicles incorporate sophisticated display systems, highlighting the importance of OCA adhesives in modern automotive design and manufacturing.

Liquid OCA Glue, OCA Optical Film in the Global Vehicle Display OCA Optical Adhesive Market:

Liquid OCA Glue and OCA Optical Film are two critical components in the Global Vehicle Display OCA Optical Adhesive Market, each playing a unique role in the assembly and performance of vehicle displays. Liquid OCA Glue is a type of adhesive that is applied in a liquid form, allowing it to fill gaps and create a seamless bond between display layers. This adhesive is particularly valued for its ability to provide excellent optical clarity, ensuring that displays remain bright and easy to read under various lighting conditions. Liquid OCA Glue is also known for its flexibility, which helps it accommodate the thermal expansion and contraction that can occur in automotive environments. This flexibility reduces the risk of delamination and other issues that could compromise display performance. On the other hand, OCA Optical Film is a pre-formed adhesive film that is used to bond display components. This film is typically applied using a lamination process, which involves pressing the film onto the display layers to create a strong, uniform bond. OCA Optical Film is prized for its ease of use and consistency, as it provides a uniform thickness and adhesive strength across the entire display surface. This consistency is crucial for maintaining the optical quality of vehicle displays, as any variations in adhesive thickness can lead to distortions or other visual defects. Both Liquid OCA Glue and OCA Optical Film are designed to meet the demanding requirements of automotive applications, including resistance to temperature extremes, humidity, and UV exposure. These adhesives must also be compatible with a wide range of display materials, such as glass, plastic, and metal, to ensure reliable performance in diverse vehicle environments. As the automotive industry continues to evolve, with increasing emphasis on digital displays and touch interfaces, the demand for high-performance OCA adhesives is expected to grow. Manufacturers are continually developing new formulations and technologies to enhance the properties of these adhesives, ensuring they can meet the challenges of modern vehicle design. This includes improving the durability and longevity of adhesives, as well as enhancing their environmental resistance to ensure displays remain clear and functional throughout the vehicle's lifespan. The Global Vehicle Display OCA Optical Adhesive Market is thus a dynamic and rapidly evolving field, driven by the need for innovative solutions that can support the next generation of automotive displays.

Passenger Vehicle, Commercial Vehicle in the Global Vehicle Display OCA Optical Adhesive Market:

The usage of Global Vehicle Display OCA Optical Adhesive Market in passenger vehicles and commercial vehicles highlights the versatility and importance of these adhesives in the automotive industry. In passenger vehicles, OCA adhesives are primarily used in infotainment systems, digital dashboards, and touchscreens. These components are integral to the modern driving experience, providing drivers and passengers with access to navigation, entertainment, and vehicle information. OCA adhesives ensure that these displays are clear, responsive, and durable, enhancing the overall quality and functionality of the vehicle's interior. The demand for advanced display technologies in passenger vehicles is driven by consumer expectations for high-tech features and seamless connectivity, making OCA adhesives a critical component in meeting these demands. In commercial vehicles, the use of OCA adhesives is equally important, though the applications may differ slightly. Commercial vehicles, such as trucks and buses, often require robust and reliable display systems for navigation, fleet management, and driver assistance. OCA adhesives play a crucial role in ensuring these displays can withstand the rigors of commercial use, including exposure to harsh environmental conditions and extended periods of operation. The durability and optical clarity provided by OCA adhesives are essential for maintaining the performance and reliability of these systems, which are vital for the safe and efficient operation of commercial vehicles. Additionally, as commercial vehicles increasingly incorporate advanced technologies, such as telematics and autonomous driving systems, the demand for high-quality display adhesives is expected to grow. The Global Vehicle Display OCA Optical Adhesive Market thus serves a wide range of applications across both passenger and commercial vehicles, highlighting the importance of these adhesives in supporting the automotive industry's ongoing technological advancements. As vehicle displays become more sophisticated and integral to the driving experience, the role of OCA adhesives in ensuring their performance and reliability will continue to be a key focus for manufacturers and industry stakeholders.

Global Vehicle Display OCA Optical Adhesive Market Outlook:

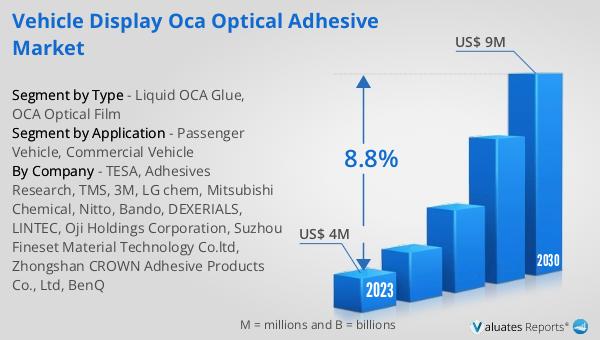

The global Vehicle Display OCA Optical Adhesive market, valued at approximately US$ 4 million in 2023, is projected to experience significant growth, reaching an estimated US$ 9 million by 2030. This growth trajectory reflects a compound annual growth rate (CAGR) of 8.8% over the forecast period from 2024 to 2030. This upward trend is indicative of the increasing demand for advanced display technologies in the automotive sector, driven by consumer preferences for enhanced in-car experiences and the integration of digital interfaces in vehicles. The market's expansion is supported by the continuous advancements in automotive display systems, which require high-performance adhesives to ensure clarity, durability, and functionality. As vehicles become more technologically advanced, with features such as infotainment systems, digital dashboards, and touchscreens, the need for reliable and effective optical adhesives becomes more pronounced. Manufacturers are investing in research and development to create innovative adhesive solutions that can meet the evolving needs of the automotive industry, further fueling market growth. The projected increase in market value underscores the importance of OCA adhesives in modern vehicle design and manufacturing, as they play a crucial role in enhancing the performance and reliability of vehicle displays. This growth also highlights the dynamic nature of the Global Vehicle Display OCA Optical Adhesive Market, as it adapts to the changing demands and technological advancements within the automotive industry.

| Report Metric | Details |

| Report Name | Vehicle Display OCA Optical Adhesive Market |

| Accounted market size in 2023 | US$ 4 million |

| Forecasted market size in 2030 | US$ 9 million |

| CAGR | 8.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | TESA, Adhesives Research, TMS, 3M, LG chem, Mitsubishi Chemical, Nitto, Bando, DEXERIALS, LINTEC, Oji Holdings Corporation, Suzhou Fineset Material Technology Co.ltd, Zhongshan CROWN Adhesive Products Co., Ltd, BenQ |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |