What is Global Low Voltage IGBT Module Market?

The Global Low Voltage IGBT Module Market is a significant segment within the power electronics industry, focusing on Insulated Gate Bipolar Transistor (IGBT) modules that operate at low voltage levels. These modules are crucial components in various applications, providing efficient power management and conversion. IGBT modules are semiconductor devices that combine the high-efficiency and fast-switching features of a MOSFET with the high-current and low-saturation-voltage capability of a bipolar transistor. The low voltage IGBT modules are typically used in applications where the voltage requirements are below 1,000 volts. They are essential in industries such as consumer electronics, automotive, and industrial control systems, where they help in reducing power loss and improving overall system efficiency. The market for these modules is driven by the increasing demand for energy-efficient electronic devices and the growing adoption of electric vehicles, which require reliable and efficient power management solutions. As technology advances, the performance and capabilities of low voltage IGBT modules continue to improve, making them an integral part of modern electronic systems. The market is characterized by continuous innovation and development, aiming to meet the evolving needs of various industries.

500V, 600V, Others in the Global Low Voltage IGBT Module Market:

In the Global Low Voltage IGBT Module Market, the voltage ratings such as 500V, 600V, and others play a crucial role in determining the suitability of these modules for different applications. The 500V IGBT modules are typically used in applications that require moderate power levels and are often found in consumer electronics and small industrial equipment. These modules offer a good balance between performance and cost, making them an attractive option for manufacturers looking to optimize their products' efficiency without significantly increasing production costs. On the other hand, the 600V IGBT modules are designed for slightly higher power applications and are commonly used in more demanding industrial environments and automotive applications. These modules provide enhanced performance and reliability, which are critical in applications where consistent power delivery and minimal downtime are essential. The "others" category includes IGBT modules with voltage ratings that do not fall within the standard 500V or 600V classifications. These modules are often customized to meet specific requirements of niche applications, offering tailored solutions for unique power management challenges. The diversity in voltage ratings allows manufacturers to choose the most appropriate module for their specific needs, ensuring optimal performance and efficiency. As the demand for energy-efficient solutions continues to grow, the development of IGBT modules with varying voltage ratings will likely expand, providing more options for industries seeking to enhance their power management capabilities. The versatility of these modules makes them suitable for a wide range of applications, from simple consumer devices to complex industrial systems, highlighting their importance in the modern technological landscape. The continuous advancement in IGBT technology is expected to drive further innovation in voltage ratings, enabling even more efficient and reliable power management solutions for various industries. As a result, the Global Low Voltage IGBT Module Market is poised for significant growth, driven by the increasing need for efficient power management solutions across different sectors.

Consumer Appliances, Industrial Control, Automotive, Others in the Global Low Voltage IGBT Module Market:

The Global Low Voltage IGBT Module Market finds extensive usage across various sectors, including consumer appliances, industrial control, automotive, and others, due to its ability to efficiently manage and convert power. In consumer appliances, low voltage IGBT modules are used to enhance the energy efficiency of devices such as refrigerators, air conditioners, and washing machines. These modules help in reducing power consumption, leading to lower electricity bills and a smaller carbon footprint. In industrial control systems, IGBT modules are crucial for managing the power supply to machinery and equipment, ensuring smooth and efficient operation. They are used in applications such as motor drives, inverters, and power supplies, where precise control of power is essential for maintaining productivity and reducing operational costs. In the automotive sector, low voltage IGBT modules are integral to the development of electric and hybrid vehicles. They are used in powertrains, battery management systems, and charging stations, where they help in optimizing power usage and extending the range of electric vehicles. The ability of IGBT modules to handle high currents and voltages while maintaining efficiency makes them ideal for automotive applications, where reliability and performance are critical. Other applications of low voltage IGBT modules include renewable energy systems, such as solar inverters and wind turbines, where they help in converting and managing the power generated from renewable sources. The versatility and efficiency of low voltage IGBT modules make them indispensable in a wide range of applications, contributing to the growing demand for these components in the global market. As industries continue to seek energy-efficient solutions, the usage of low voltage IGBT modules is expected to increase, driving further innovation and development in this market.

Global Low Voltage IGBT Module Market Outlook:

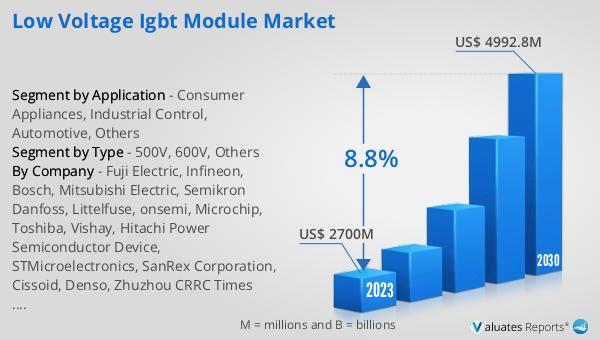

The outlook for the Global Low Voltage IGBT Module Market is promising, with significant growth anticipated over the coming years. In 2023, the market was valued at approximately US$ 2,700 million, reflecting the strong demand for efficient power management solutions across various industries. By 2030, the market is expected to reach an impressive US$ 4,992.8 million, driven by a compound annual growth rate (CAGR) of 8.8% during the forecast period from 2024 to 2030. This growth is indicative of the increasing adoption of low voltage IGBT modules in applications such as consumer electronics, automotive, and industrial control systems, where the need for energy-efficient and reliable power management solutions is paramount. The market's expansion is also fueled by technological advancements in IGBT module design and manufacturing, which are enhancing the performance and capabilities of these components. As industries continue to prioritize energy efficiency and sustainability, the demand for low voltage IGBT modules is expected to rise, supporting the market's robust growth trajectory. The positive outlook for the Global Low Voltage IGBT Module Market underscores the importance of these components in modern electronic systems and highlights the ongoing innovation and development within this sector.

| Report Metric | Details |

| Report Name | Low Voltage IGBT Module Market |

| Accounted market size in 2023 | US$ 2700 million |

| Forecasted market size in 2030 | US$ 4992.8 million |

| CAGR | 8.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Fuji Electric, Infineon, Bosch, Mitsubishi Electric, Semikron Danfoss, Littelfuse, onsemi, Microchip, Toshiba, Vishay, Hitachi Power Semiconductor Device, STMicroelectronics, SanRex Corporation, Cissoid, Denso, Zhuzhou CRRC Times Electric |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |