What is Global PET Laminating Film Market?

The Global PET Laminating Film Market refers to the worldwide industry focused on the production, distribution, and utilization of PET (Polyethylene Terephthalate) laminating films. These films are widely used for their excellent clarity, durability, and protective properties. PET laminating films are primarily employed to enhance the appearance and longevity of printed materials, packaging, and various other products. They provide a protective layer that guards against moisture, dust, and physical damage, thereby extending the lifespan of the laminated items. The market encompasses a diverse range of applications, including packaging, printing, and other industrial uses. The demand for PET laminating films is driven by their superior performance characteristics, such as high tensile strength, chemical resistance, and thermal stability. Additionally, the market is influenced by factors like technological advancements, increasing consumer awareness about product protection, and the growing need for sustainable packaging solutions. Overall, the Global PET Laminating Film Market plays a crucial role in various industries by offering reliable and efficient solutions for product enhancement and protection.

Glossy, Matte in the Global PET Laminating Film Market:

Glossy and matte finishes are two popular types of PET laminating films used in the Global PET Laminating Film Market. Glossy PET laminating films are known for their high shine and reflective surface, which enhances the visual appeal of printed materials by making colors appear more vibrant and images more striking. This type of finish is often preferred for applications where a premium look is desired, such as in marketing materials, book covers, and high-end packaging. The glossy surface not only improves the aesthetic appeal but also provides a smooth texture that is pleasant to touch. On the other hand, matte PET laminating films offer a non-reflective, satin-like finish that reduces glare and provides a more subdued and elegant appearance. This type of finish is ideal for applications where readability and a professional look are important, such as in business cards, menus, and instructional materials. Matte films are also less prone to showing fingerprints and smudges, making them a practical choice for frequently handled items. Both glossy and matte PET laminating films provide excellent protection against moisture, dust, and physical damage, ensuring the longevity of the laminated products. The choice between glossy and matte finishes depends on the specific requirements of the application, including the desired visual effect, the level of protection needed, and the type of material being laminated. In the Global PET Laminating Film Market, manufacturers offer a wide range of options in both finishes to cater to the diverse needs of various industries. Technological advancements have also led to the development of specialized PET laminating films with additional features, such as UV protection, anti-static properties, and enhanced adhesion. These innovations further expand the applications and benefits of PET laminating films, making them a versatile and valuable solution for product enhancement and protection. Overall, the availability of both glossy and matte PET laminating films in the market provides consumers with the flexibility to choose the most suitable option for their specific needs, ensuring optimal performance and aesthetic appeal.

Packaging, Printing, Other in the Global PET Laminating Film Market:

The Global PET Laminating Film Market finds extensive usage in various areas, including packaging, printing, and other industrial applications. In the packaging industry, PET laminating films are widely used to enhance the durability and visual appeal of packaging materials. They provide a protective barrier that shields products from moisture, dust, and physical damage, thereby extending their shelf life. PET laminating films are commonly used in food packaging, where they help maintain the freshness and quality of the products. They are also used in the packaging of consumer goods, pharmaceuticals, and electronics, where product protection and presentation are crucial. In the printing industry, PET laminating films are used to enhance the appearance and durability of printed materials. They are applied to book covers, brochures, posters, and other printed items to provide a glossy or matte finish that enhances the visual appeal and protects the printed surface from wear and tear. PET laminating films also improve the rigidity and strength of printed materials, making them more resistant to bending and creasing. In addition to packaging and printing, PET laminating films are used in various other industrial applications. They are employed in the production of labels, ID cards, and security documents, where durability and protection are essential. PET laminating films are also used in the automotive and construction industries, where they provide protective coatings for surfaces exposed to harsh environmental conditions. The versatility and superior performance characteristics of PET laminating films make them a valuable solution for a wide range of applications, ensuring product protection and enhancement across various industries.

Global PET Laminating Film Market Outlook:

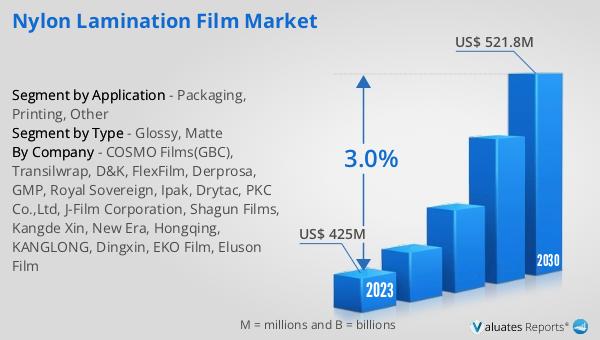

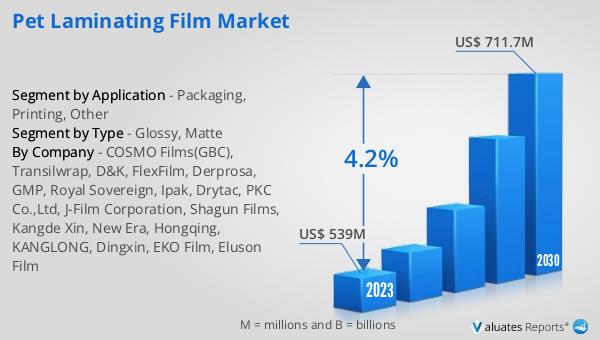

The global PET Laminating Film market was valued at US$ 539 million in 2023 and is anticipated to reach US$ 711.7 million by 2030, witnessing a CAGR of 4.2% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory for the PET laminating film industry, driven by increasing demand for high-quality, durable, and protective laminating solutions across various sectors. The projected growth reflects the rising awareness among consumers and businesses about the benefits of PET laminating films, including their excellent clarity, chemical resistance, and thermal stability. As industries continue to seek reliable and efficient solutions for product enhancement and protection, the demand for PET laminating films is expected to grow. The market's expansion is also supported by technological advancements and the development of innovative laminating films with additional features, such as UV protection and anti-static properties. These innovations cater to the evolving needs of different industries, further driving the market's growth. Overall, the positive market outlook for the global PET Laminating Film market underscores the importance of these films in various applications and highlights their potential for continued growth and development in the coming years.

| Report Metric | Details |

| Report Name | PET Laminating Film Market |

| Accounted market size in 2023 | US$ 539 million |

| Forecasted market size in 2030 | US$ 711.7 million |

| CAGR | 4.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | COSMO Films(GBC), Transilwrap, D&K, FlexFilm, Derprosa, GMP, Royal Sovereign, Ipak, Drytac, PKC Co.,Ltd, J-Film Corporation, Shagun Films, Kangde Xin, New Era, Hongqing, KANGLONG, Dingxin, EKO Film, Eluson Film |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |