What is Global mmWave Filters Market?

The Global mmWave Filters Market refers to the market for filters that operate in the millimeter-wave (mmWave) frequency range, typically between 30 GHz and 300 GHz. These filters are essential components in various high-frequency applications, including telecommunications, radar systems, and satellite communications. They help in filtering out unwanted signals and noise, ensuring that only the desired frequencies are transmitted or received. The increasing demand for high-speed wireless communication, particularly with the advent of 5G technology, has significantly boosted the need for mmWave filters. These filters are crucial for enabling the high data rates and low latency required by modern communication systems. Additionally, the growing use of mmWave technology in military applications, such as radar and electronic warfare, further drives the market. The market is characterized by continuous advancements in filter design and materials, aimed at improving performance and reducing costs. As a result, the Global mmWave Filters Market is poised for substantial growth in the coming years, driven by technological innovations and expanding applications across various industries.

n258, n257, n260, n261 in the Global mmWave Filters Market:

The n258, n257, n260, and n261 are specific frequency bands allocated for 5G mmWave technology, each with unique characteristics and applications. The n258 band operates in the 24.25 GHz to 27.5 GHz range, making it suitable for urban and suburban deployments due to its relatively lower frequency within the mmWave spectrum. This band offers a good balance between coverage and capacity, making it ideal for enhancing mobile broadband services in densely populated areas. The n257 band, on the other hand, spans from 26.5 GHz to 29.5 GHz and is often used for fixed wireless access (FWA) and backhaul applications. Its higher frequency allows for greater data throughput, making it suitable for providing high-speed internet services to homes and businesses, especially in areas where laying fiber optic cables is impractical. The n260 band, covering 37 GHz to 40 GHz, is primarily used for ultra-high-capacity applications, such as large-scale events and stadiums, where a significant number of users require high-speed connectivity simultaneously. This band’s higher frequency enables it to support extremely high data rates, albeit with a shorter range compared to lower frequency bands. Lastly, the n261 band operates in the 27.5 GHz to 28.35 GHz range and is often utilized for both mobile and fixed wireless services. Its characteristics make it versatile for various applications, including enhancing mobile network capacity and providing high-speed internet in urban areas. The allocation and utilization of these bands are crucial for the successful deployment of 5G networks, as they enable the high-speed, low-latency communication required for modern applications. Each band’s unique properties allow network operators to tailor their services to specific needs, ensuring optimal performance and user experience. As the demand for high-speed wireless communication continues to grow, the importance of these mmWave bands in the Global mmWave Filters Market cannot be overstated.

5G mmWave Smart Phone, 5G mmWave Base Station, Military, VSAT & Satellite in the Global mmWave Filters Market:

The usage of Global mmWave Filters Market in 5G mmWave smartphones, 5G mmWave base stations, military applications, and VSAT & satellite communications is diverse and critical for the advancement of these technologies. In 5G mmWave smartphones, mmWave filters are essential for ensuring that the devices can handle the high-frequency signals required for ultra-fast data transmission. These filters help in isolating the desired mmWave frequencies from other signals, thereby enhancing the performance and reliability of the smartphones. The integration of mmWave technology in smartphones allows users to experience faster download and upload speeds, lower latency, and improved overall connectivity, which are crucial for applications such as streaming high-definition videos, online gaming, and augmented reality (AR) experiences. In 5G mmWave base stations, mmWave filters play a pivotal role in managing the high-frequency signals that are transmitted and received. These filters help in reducing interference and ensuring that the base stations can handle the large volumes of data traffic associated with 5G networks. By improving the efficiency and performance of base stations, mmWave filters contribute to the overall effectiveness of 5G networks, enabling them to support a higher number of connected devices and deliver faster and more reliable services. In military applications, mmWave filters are used in radar systems, electronic warfare, and secure communication systems. These filters help in enhancing the accuracy and reliability of radar systems by filtering out unwanted signals and noise, thereby improving target detection and tracking capabilities. In electronic warfare, mmWave filters are used to protect communication systems from jamming and interference, ensuring secure and reliable communication in hostile environments. In VSAT (Very Small Aperture Terminal) and satellite communications, mmWave filters are crucial for ensuring the integrity and reliability of the high-frequency signals used for data transmission. These filters help in isolating the desired frequencies from other signals, thereby reducing interference and improving the overall performance of satellite communication systems. By enabling high-speed data transmission and reliable connectivity, mmWave filters play a vital role in supporting various satellite-based applications, including remote sensing, weather forecasting, and global positioning systems (GPS). Overall, the usage of mmWave filters in these areas highlights their importance in enabling the high-speed, low-latency communication required for modern applications, and their role in driving the growth of the Global mmWave Filters Market.

Global mmWave Filters Market Outlook:

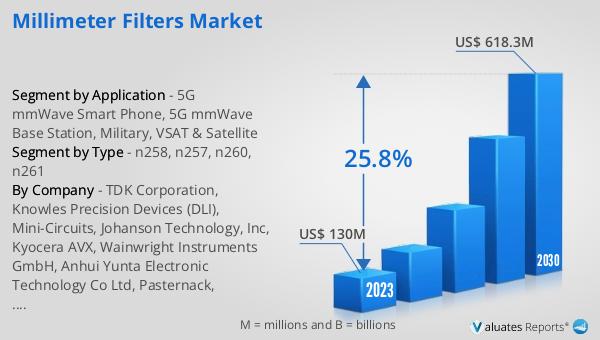

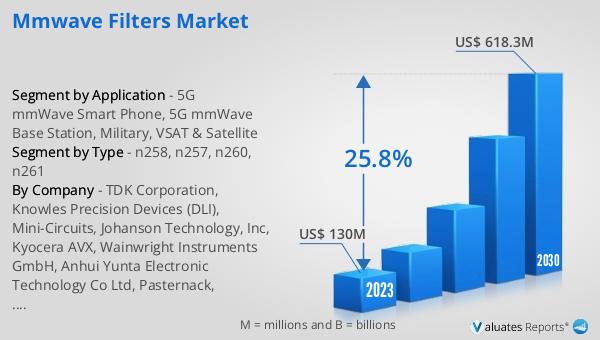

The global mmWave Filters market, valued at US$ 130 million in 2023, is projected to grow significantly, reaching an estimated US$ 618.3 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 25.8% during the forecast period from 2024 to 2030. This substantial increase in market value underscores the rising demand for mmWave filters across various applications, driven by the rapid advancements in 5G technology and the increasing need for high-speed, low-latency communication. The market's expansion is also fueled by the growing adoption of mmWave technology in military applications, satellite communications, and other high-frequency applications. As industries continue to embrace mmWave technology to meet the demands of modern communication systems, the Global mmWave Filters Market is poised for significant growth, reflecting the critical role these filters play in enabling advanced communication technologies.

| Report Metric | Details |

| Report Name | mmWave Filters Market |

| Accounted market size in 2023 | US$ 130 million |

| Forecasted market size in 2030 | US$ 618.3 million |

| CAGR | 25.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | TDK Corporation, Knowles Precision Devices (DLI), Mini-Circuits, Johanson Technology, Inc, Kyocera AVX, Wainwright Instruments GmbH, Anhui Yunta Electronic Technology Co Ltd, Pasternack, Benchmark Lark Technology, Mi-Wave, TMY Technology Inc |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |