What is Global High Performance Plastics for Semiconductor Equipment Market?

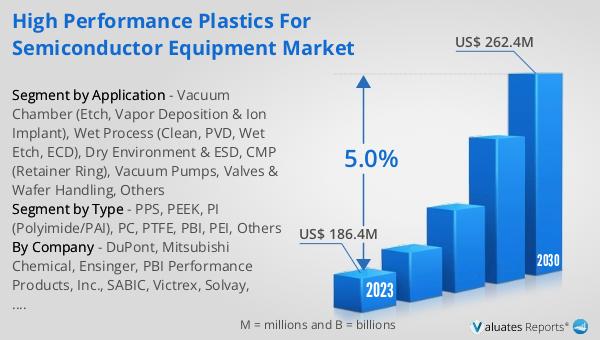

The global High Performance Plastics for Semiconductor Equipment market is a specialized sector focusing on advanced plastic materials used in the manufacturing and operation of semiconductor equipment. These high-performance plastics are essential due to their exceptional properties such as high thermal stability, chemical resistance, and mechanical strength, which are crucial for the demanding environments of semiconductor fabrication. The market for these materials was valued at US$ 186.4 million in 2023 and is projected to grow to US$ 262.4 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.0% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for semiconductor devices across various industries, including consumer electronics, automotive, and telecommunications. According to SEMI, worldwide sales of semiconductor manufacturing equipment increased by 5% from $102.6 billion in 2021 to a record $107.6 billion in 2022. Despite a 5% slowdown in investment pace, China remained the largest semiconductor equipment market in 2022, accounting for $28.3 billion in billings. This indicates a robust and growing market for high-performance plastics in semiconductor equipment, driven by technological advancements and increasing production capacities.

PPS, PEEK, PI (Polyimide/PAI), PC, PTFE, PBI, PEI, Others in the Global High Performance Plastics for Semiconductor Equipment Market:

High-performance plastics such as PPS (Polyphenylene Sulfide), PEEK (Polyether Ether Ketone), PI (Polyimide/PAI), PC (Polycarbonate), PTFE (Polytetrafluoroethylene), PBI (Polybenzimidazole), and PEI (Polyetherimide) play a crucial role in the semiconductor equipment market. PPS is known for its excellent chemical resistance and dimensional stability, making it ideal for components exposed to harsh chemicals and high temperatures. PEEK is highly regarded for its mechanical strength and thermal stability, often used in applications requiring high performance under extreme conditions. PI and PAI are valued for their exceptional thermal and chemical resistance, making them suitable for high-temperature applications. PC is widely used due to its impact resistance and optical clarity, essential for protective covers and transparent components. PTFE, commonly known as Teflon, is renowned for its low friction and high chemical resistance, making it ideal for seals and gaskets. PBI offers the highest heat resistance among thermoplastics, making it suitable for extreme temperature environments. PEI is known for its high strength and dimensional stability, often used in structural components. These materials are selected based on their unique properties to meet the specific demands of semiconductor manufacturing processes, ensuring reliability and efficiency in production.

Vacuum Chamber (Etch, Vapor Deposition & Ion Implant), Wet Process (Clean, PVD, Wet Etch, ECD), Dry Environment & ESD, CMP (Retainer Ring), Vacuum Pumps, Valves & Wafer Handling, Others in the Global High Performance Plastics for Semiconductor Equipment Market:

High-performance plastics are extensively used in various areas of semiconductor equipment, each serving a specific function to enhance the performance and reliability of the equipment. In vacuum chambers, which are used for processes like etching, vapor deposition, and ion implantation, materials like PEEK and PTFE are used due to their excellent vacuum compatibility and resistance to outgassing. For wet processes such as cleaning, physical vapor deposition (PVD), wet etching, and electrochemical deposition (ECD), plastics like PPS and PTFE are preferred for their chemical resistance and durability in corrosive environments. In dry environments and electrostatic discharge (ESD) applications, materials like PI and PAI are used for their high thermal stability and electrical insulating properties. For chemical mechanical planarization (CMP) processes, retainer rings made from PEEK or PEI are used due to their wear resistance and mechanical strength. Vacuum pumps and valves, which are critical for maintaining the vacuum environment in semiconductor manufacturing, often use PTFE and PBI for their sealing and high-temperature capabilities. Wafer handling equipment, which requires precision and cleanliness, uses materials like PC and PEI for their strength and low particulate generation. These high-performance plastics ensure that semiconductor equipment operates efficiently and reliably, meeting the stringent requirements of the semiconductor industry.

Global High Performance Plastics for Semiconductor Equipment Market Outlook:

The global High Performance Plastics for Semiconductor Equipment market was valued at US$ 186.4 million in 2023 and is anticipated to reach US$ 262.4 million by 2030, witnessing a CAGR of 5.0% during the forecast period from 2024 to 2030. According to SEMI, worldwide sales of semiconductor manufacturing equipment increased by 5% from $102.6 billion in 2021 to an all-time record of $107.6 billion in 2022. For the third consecutive year, China remained the largest semiconductor equipment market in 2022, despite a 5% slowdown in the pace of investments in the region year over year, accounting for $28.3 billion in billings. This growth is indicative of the increasing demand for semiconductor devices and the corresponding need for high-performance plastics that can withstand the rigorous conditions of semiconductor manufacturing. The market outlook suggests a robust growth trajectory driven by technological advancements and the expanding applications of semiconductors across various industries. The continued investment in semiconductor manufacturing equipment, particularly in regions like China, underscores the critical role of high-performance plastics in supporting the semiconductor industry's growth and innovation.

| Report Metric | Details |

| Report Name | High Performance Plastics for Semiconductor Equipment Market |

| Accounted market size in 2023 | US$ 186.4 million |

| Forecasted market size in 2030 | US$ 262.4 million |

| CAGR | 5.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | DuPont, Mitsubishi Chemical, Ensinger, PBI Performance Products, Inc., SABIC, Victrex, Solvay, Evonik Industries, 3M, Chemours, CDI Products |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |