What is Global Ceramic Nanochemicals Market?

The Global Ceramic Nanochemicals Market is a rapidly evolving sector that focuses on the production and application of nanochemicals derived from ceramics. These nanochemicals are extremely small particles, often less than 100 nanometers in size, and they exhibit unique properties that make them highly valuable in various industries. The market for these materials is driven by their exceptional mechanical, thermal, and electrical properties, which are significantly different from their bulk counterparts. These properties make ceramic nanochemicals ideal for use in advanced manufacturing processes, high-performance materials, and cutting-edge technologies. The demand for ceramic nanochemicals is increasing due to their applications in sectors such as electronics, pharmaceuticals, energy, and more. As industries continue to seek materials that offer superior performance and efficiency, the global ceramic nanochemicals market is expected to grow, driven by innovations and advancements in nanotechnology.

Metallic Compounds, Nonmetallic Compounds in the Global Ceramic Nanochemicals Market:

Metallic compounds and nonmetallic compounds are two primary categories within the Global Ceramic Nanochemicals Market, each offering distinct advantages and applications. Metallic compounds in ceramic nanochemicals typically include materials like titanium dioxide, zinc oxide, and aluminum oxide. These compounds are known for their excellent electrical conductivity, high thermal stability, and strong mechanical properties. Titanium dioxide, for example, is widely used in the production of semiconductors and electronic devices due to its high refractive index and strong UV light absorption capabilities. Zinc oxide is another metallic compound that finds extensive use in the electronics industry, particularly in the manufacturing of transparent conductive films and sensors. Aluminum oxide, on the other hand, is valued for its hardness and is often used in abrasive applications and as a catalyst in chemical reactions. Nonmetallic compounds in ceramic nanochemicals include materials such as silicon dioxide, boron nitride, and silicon carbide. Silicon dioxide, commonly known as silica, is a versatile material used in various industries, including electronics, pharmaceuticals, and food and agriculture. In electronics, silica is used as an insulating material in integrated circuits and as a component in optical fibers. Boron nitride is another nonmetallic compound that is highly valued for its thermal conductivity and electrical insulation properties. It is often used in high-temperature applications and as a lubricant in various industrial processes. Silicon carbide is known for its exceptional hardness and thermal stability, making it ideal for use in high-performance ceramics and as a semiconductor material in power electronics. The unique properties of both metallic and nonmetallic compounds in ceramic nanochemicals make them indispensable in modern technology and industrial applications. Metallic compounds, with their superior electrical and thermal properties, are essential in the development of advanced electronic devices and high-performance materials. Nonmetallic compounds, with their versatility and stability, are crucial in a wide range of applications, from pharmaceuticals to energy storage. The ongoing research and development in the field of nanotechnology continue to expand the potential uses of these compounds, driving innovation and growth in the Global Ceramic Nanochemicals Market. As industries increasingly adopt nanotechnology to enhance product performance and efficiency, the demand for both metallic and nonmetallic ceramic nanochemicals is expected to rise, further propelling the market forward.

Semiconductors & Electronics, Pharmaceuticals, Food & Agriculture, Energy, Textiles, Others in the Global Ceramic Nanochemicals Market:

The Global Ceramic Nanochemicals Market finds extensive usage across various sectors, including semiconductors and electronics, pharmaceuticals, food and agriculture, energy, textiles, and others. In the semiconductors and electronics industry, ceramic nanochemicals are used to enhance the performance and efficiency of electronic devices. Materials like titanium dioxide and zinc oxide are employed in the production of semiconductors, sensors, and transparent conductive films. These nanochemicals improve the electrical conductivity, thermal stability, and overall performance of electronic components, making them essential in the manufacturing of advanced electronic devices. In the pharmaceutical industry, ceramic nanochemicals play a crucial role in drug delivery systems and medical diagnostics. Silicon dioxide, for example, is used as a carrier for drug delivery, enhancing the bioavailability and stability of pharmaceutical compounds. The unique properties of ceramic nanochemicals, such as their high surface area and biocompatibility, make them ideal for use in targeted drug delivery and imaging applications. These materials are also used in the development of biosensors and diagnostic tools, providing accurate and efficient detection of various medical conditions. The food and agriculture sector also benefits from the use of ceramic nanochemicals. These materials are used in food packaging to improve the shelf life and safety of food products. Nanochemicals like zinc oxide and silicon dioxide are incorporated into packaging materials to provide antimicrobial properties, preventing the growth of harmful bacteria and extending the freshness of food. In agriculture, ceramic nanochemicals are used in the development of advanced fertilizers and pesticides, enhancing crop yield and reducing the environmental impact of agricultural practices. In the energy sector, ceramic nanochemicals are used in the development of advanced energy storage and conversion systems. Materials like silicon carbide and boron nitride are employed in the production of high-performance batteries, fuel cells, and supercapacitors. These nanochemicals improve the efficiency, stability, and lifespan of energy storage devices, contributing to the advancement of renewable energy technologies. The unique properties of ceramic nanochemicals, such as their high thermal conductivity and electrical insulation, make them ideal for use in energy applications. The textile industry also utilizes ceramic nanochemicals to enhance the properties of fabrics and textiles. Nanochemicals like titanium dioxide and zinc oxide are used to impart antimicrobial, UV-protective, and self-cleaning properties to textiles. These materials are incorporated into fabrics to provide added functionality and durability, making them suitable for use in various applications, including medical textiles, sportswear, and protective clothing. In addition to these sectors, ceramic nanochemicals find applications in other industries, such as automotive, aerospace, and construction. The unique properties of these materials, including their high strength, thermal stability, and electrical conductivity, make them valuable in the development of advanced materials and technologies. As industries continue to seek innovative solutions to improve product performance and efficiency, the demand for ceramic nanochemicals is expected to grow, driving the expansion of the Global Ceramic Nanochemicals Market.

Global Ceramic Nanochemicals Market Outlook:

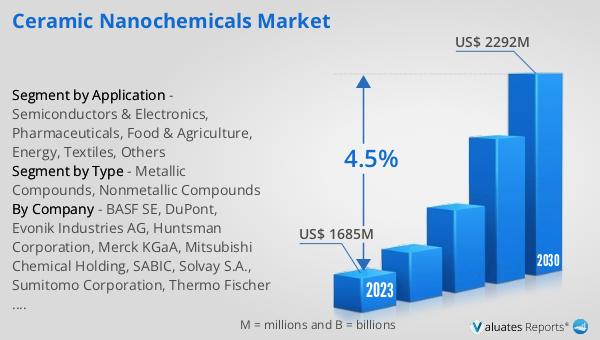

The global Ceramic Nanochemicals market experienced significant growth, with its valuation reaching US$ 1685 million in 2023. This market is projected to continue its upward trajectory, aiming to achieve a valuation of US$ 2292 million by 2030. This growth is anticipated to occur at a compound annual growth rate (CAGR) of 4.5% during the forecast period from 2024 to 2030. The steady increase in market value highlights the rising demand and expanding applications of ceramic nanochemicals across various industries. The unique properties of these nanochemicals, such as their enhanced mechanical, thermal, and electrical characteristics, make them highly sought after in sectors like electronics, pharmaceuticals, energy, and more. As industries continue to innovate and integrate advanced materials into their products and processes, the global Ceramic Nanochemicals market is poised for sustained growth and development.

| Report Metric | Details |

| Report Name | Ceramic Nanochemicals Market |

| Accounted market size in 2023 | US$ 1685 million |

| Forecasted market size in 2030 | US$ 2292 million |

| CAGR | 4.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | BASF SE, DuPont, Evonik Industries AG, Huntsman Corporation, Merck KGaA, Mitsubishi Chemical Holding, SABIC, Solvay S.A., Sumitomo Corporation, Thermo Fischer Scientific |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |