What is Global Automatic Robotic Nozzle Cleaning Stations Market?

The Global Automatic Robotic Nozzle Cleaning Stations Market refers to the industry focused on the development, production, and distribution of automated systems designed to clean nozzles used in various industrial applications. These systems utilize robotic technology to ensure precision and efficiency in cleaning processes, which is crucial for maintaining the performance and longevity of equipment. The market encompasses a wide range of products, including electric and pneumatic cleaning stations, each tailored to meet specific industry needs. The demand for these systems is driven by the need for improved operational efficiency, reduced downtime, and enhanced safety in industrial environments. As industries continue to adopt automation and advanced technologies, the market for automatic robotic nozzle cleaning stations is expected to grow, offering innovative solutions to meet the evolving needs of various sectors.

Electric Cleaning Stations, Pneumatic Cleaning Stations in the Global Automatic Robotic Nozzle Cleaning Stations Market:

Electric cleaning stations and pneumatic cleaning stations are two primary types of systems within the Global Automatic Robotic Nozzle Cleaning Stations Market. Electric cleaning stations utilize electrical power to operate the robotic mechanisms that clean the nozzles. These systems are known for their precision and reliability, making them suitable for applications where consistent and thorough cleaning is required. Electric cleaning stations often feature advanced control systems that allow for easy programming and customization of cleaning cycles, ensuring that nozzles are cleaned to the exact specifications needed for optimal performance. On the other hand, pneumatic cleaning stations use compressed air to power the robotic cleaning mechanisms. These systems are typically more robust and can handle harsher environments where electrical systems might be less effective. Pneumatic cleaning stations are often preferred in industries where there is a risk of electrical hazards or where the use of compressed air is more practical. Both types of cleaning stations offer unique advantages and are chosen based on the specific requirements of the application. For instance, in industries where precision and control are paramount, electric cleaning stations might be the preferred choice. In contrast, in environments where durability and resistance to harsh conditions are critical, pneumatic cleaning stations might be more suitable. The choice between electric and pneumatic cleaning stations ultimately depends on factors such as the nature of the nozzles being cleaned, the operating environment, and the specific needs of the industry. As the market continues to evolve, manufacturers are developing more advanced and versatile cleaning stations that can cater to a broader range of applications, further driving the growth of the Global Automatic Robotic Nozzle Cleaning Stations Market.

Automotive & Transportation, Construction, Aerospace & Defense, Metals & Machinery, Others in the Global Automatic Robotic Nozzle Cleaning Stations Market:

The usage of Global Automatic Robotic Nozzle Cleaning Stations Market spans across various industries, including automotive and transportation, construction, aerospace and defense, metals and machinery, and others. In the automotive and transportation sector, these cleaning stations are essential for maintaining the performance of spray nozzles used in painting and coating processes. By ensuring that nozzles are free from clogs and contaminants, these systems help achieve a high-quality finish on vehicles and components, reducing the need for rework and improving overall efficiency. In the construction industry, automatic robotic nozzle cleaning stations are used to clean nozzles in equipment such as concrete sprayers and coating machines. This ensures that the equipment operates smoothly and consistently, reducing downtime and maintenance costs. In the aerospace and defense sector, the precision and reliability of nozzle cleaning are critical for applications such as aircraft painting and coating. These cleaning stations help maintain the performance of nozzles, ensuring that coatings are applied evenly and effectively, which is crucial for the safety and performance of aircraft. In the metals and machinery industry, automatic robotic nozzle cleaning stations are used to clean nozzles in welding and cutting equipment. This helps maintain the quality of welds and cuts, reducing defects and improving the overall efficiency of manufacturing processes. Other industries that benefit from these cleaning stations include food and beverage, pharmaceuticals, and electronics, where the cleanliness and performance of nozzles are critical for product quality and safety. Overall, the Global Automatic Robotic Nozzle Cleaning Stations Market plays a vital role in enhancing the efficiency, reliability, and safety of various industrial processes, driving the demand for these advanced cleaning solutions across multiple sectors.

Global Automatic Robotic Nozzle Cleaning Stations Market Outlook:

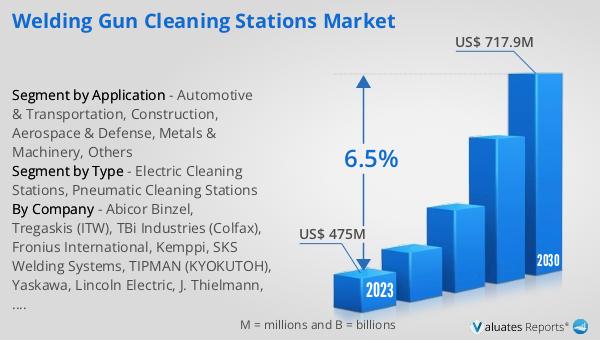

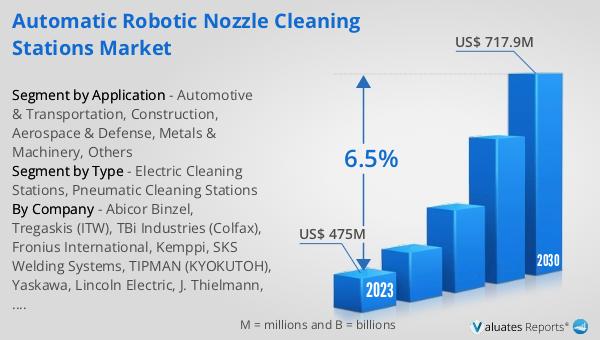

The global Automatic Robotic Nozzle Cleaning Stations market was valued at US$ 475 million in 2023 and is anticipated to reach US$ 717.9 million by 2030, witnessing a CAGR of 6.5% during the forecast period from 2024 to 2030. This significant growth reflects the increasing demand for automated cleaning solutions across various industries. As companies strive to improve operational efficiency and reduce downtime, the adoption of robotic nozzle cleaning stations is expected to rise. These systems offer numerous benefits, including enhanced precision, reduced maintenance costs, and improved safety, making them an attractive investment for businesses looking to optimize their processes. The market's growth is also driven by advancements in robotic technology and the development of more versatile and efficient cleaning stations. As industries continue to embrace automation and advanced technologies, the Global Automatic Robotic Nozzle Cleaning Stations Market is poised for substantial expansion, offering innovative solutions to meet the evolving needs of various sectors.

| Report Metric | Details |

| Report Name | Automatic Robotic Nozzle Cleaning Stations Market |

| Accounted market size in 2023 | US$ 475 million |

| Forecasted market size in 2030 | US$ 717.9 million |

| CAGR | 6.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Abicor Binzel, Tregaskis (ITW), TBi Industries (Colfax), Fronius International, Kemppi, SKS Welding Systems, TIPMAN (KYOKUTOH), Yaskawa, Lincoln Electric, J. Thielmann, ELCo Enterprises, Tokin Corporation, OTC Daihen, CM Industries, DINSE, Sumig, American Weldquip, Wuxi Gushi, Aotai Electric, RM Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |