What is Global EMI and EMP Protection Connectors Market?

The Global EMI and EMP Protection Connectors Market is a specialized segment within the broader electronics and electrical components industry. EMI stands for Electromagnetic Interference, and EMP stands for Electromagnetic Pulse. These connectors are designed to protect electronic devices and systems from the disruptive effects of electromagnetic interference and pulses, which can cause malfunctions or even permanent damage. The market for these connectors is driven by the increasing need for reliable and secure electronic systems in various sectors, including military, aerospace, industrial, and medical applications. As technology advances and the reliance on electronic systems grows, the demand for EMI and EMP protection connectors is expected to rise. These connectors are essential for ensuring the integrity and functionality of electronic systems in environments where electromagnetic interference is a concern. The market is characterized by a range of products, including circular connectors, rectangular connectors, and other specialized types, each designed to meet specific requirements and standards.

Circular Connectors, Rectangular Connectors, Others in the Global EMI and EMP Protection Connectors Market:

Circular connectors are a significant category within the Global EMI and EMP Protection Connectors Market. These connectors are characterized by their cylindrical shape and are commonly used in applications where space is limited, and a robust connection is required. Circular connectors are favored for their durability, ease of use, and ability to provide a secure connection in harsh environments. They are often used in military and defense applications, where reliability and performance are critical. These connectors are designed to withstand extreme conditions, including high levels of vibration, temperature fluctuations, and exposure to moisture and dust. In addition to military applications, circular connectors are also used in aerospace, industrial, and medical devices, where their compact size and robust design make them ideal for use in challenging environments. Rectangular connectors, on the other hand, are characterized by their rectangular shape and are typically used in applications where a higher density of connections is required. These connectors are often used in industrial and commercial applications, where space is less of a concern, and a large number of connections need to be made. Rectangular connectors are known for their versatility and ability to accommodate a wide range of connection types, including power, signal, and data connections. They are also designed to provide a high level of protection against EMI and EMP, ensuring the integrity of the connections in environments where electromagnetic interference is a concern. Other types of connectors in the Global EMI and EMP Protection Connectors Market include specialized connectors designed for specific applications. These may include connectors with unique shapes or features designed to meet the requirements of particular industries or applications. For example, connectors used in space applications may be designed to withstand the extreme conditions of space, including high levels of radiation and temperature fluctuations. Similarly, connectors used in medical devices may be designed to meet stringent safety and performance standards, ensuring the reliability and safety of the devices in which they are used. Overall, the Global EMI and EMP Protection Connectors Market is characterized by a wide range of products designed to meet the diverse needs of various industries and applications. Each type of connector offers unique features and benefits, making them suitable for use in different environments and applications. As the demand for reliable and secure electronic systems continues to grow, the market for EMI and EMP protection connectors is expected to expand, driven by the need for robust and reliable connections in a wide range of applications.

Military & Defense, Space Application, Aviation & UAV, Industrial Application, Medical Devices, Others in the Global EMI and EMP Protection Connectors Market:

The usage of Global EMI and EMP Protection Connectors Market spans across various critical sectors, each with unique requirements and challenges. In the Military & Defense sector, these connectors are indispensable due to the high stakes involved. Military operations often take place in environments with significant electromagnetic interference, which can disrupt communication and control systems. EMI and EMP protection connectors ensure that military equipment, from communication devices to weapon systems, operates reliably without interference. These connectors are designed to withstand harsh conditions, including extreme temperatures, vibrations, and exposure to contaminants, making them ideal for use in military applications. In Space Applications, the need for EMI and EMP protection connectors is equally critical. Spacecraft and satellites operate in an environment with high levels of radiation and electromagnetic interference. These connectors ensure the integrity of communication and control systems, which are vital for the success of space missions. They are designed to withstand the extreme conditions of space, including temperature fluctuations and radiation, ensuring the reliability and performance of space systems. In the Aviation & UAV sector, EMI and EMP protection connectors are used to ensure the reliability of avionics and communication systems. Aircraft and unmanned aerial vehicles (UAVs) operate in environments with significant electromagnetic interference, which can disrupt critical systems. These connectors provide a secure and reliable connection, ensuring the safety and performance of aviation systems. In Industrial Applications, EMI and EMP protection connectors are used in a wide range of equipment and systems, from manufacturing machinery to control systems. Industrial environments often have high levels of electromagnetic interference, which can disrupt the operation of equipment and systems. These connectors ensure the reliability and performance of industrial systems, reducing the risk of malfunctions and downtime. In Medical Devices, the need for EMI and EMP protection connectors is driven by the critical nature of medical equipment. Medical devices, from diagnostic equipment to life-support systems, must operate reliably without interference. These connectors ensure the integrity of connections, providing a secure and reliable connection in environments with significant electromagnetic interference. Other sectors that use EMI and EMP protection connectors include telecommunications, automotive, and consumer electronics. In each of these sectors, the need for reliable and secure connections is critical, driving the demand for EMI and EMP protection connectors. Overall, the usage of EMI and EMP protection connectors spans across various critical sectors, each with unique requirements and challenges. These connectors ensure the reliability and performance of electronic systems, providing a secure and reliable connection in environments with significant electromagnetic interference.

Global EMI and EMP Protection Connectors Market Outlook:

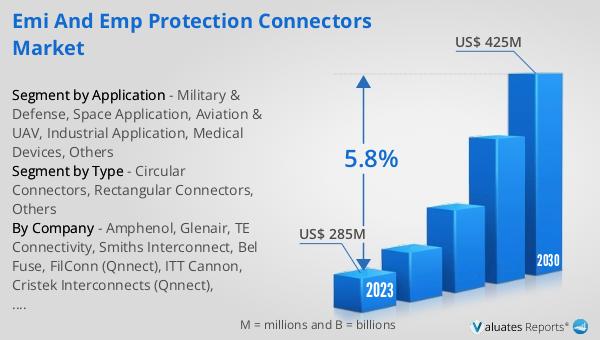

The global market for EMI and EMP Protection Connectors was valued at $285 million in 2023 and is projected to grow to $425 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.8% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for reliable and secure electronic systems across various sectors, including military, aerospace, industrial, and medical applications. As technology continues to advance and the reliance on electronic systems grows, the need for EMI and EMP protection connectors is expected to rise. These connectors play a crucial role in ensuring the integrity and functionality of electronic systems in environments where electromagnetic interference is a concern. The market is characterized by a range of products, including circular connectors, rectangular connectors, and other specialized types, each designed to meet specific requirements and standards. The growth of the market is also driven by the increasing adoption of advanced technologies and the need for robust and reliable connections in a wide range of applications. Overall, the global EMI and EMP Protection Connectors market is expected to experience significant growth in the coming years, driven by the increasing demand for reliable and secure electronic systems.

| Report Metric | Details |

| Report Name | EMI and EMP Protection Connectors Market |

| Accounted market size in 2023 | US$ 285 million |

| Forecasted market size in 2030 | US$ 425 million |

| CAGR | 5.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Amphenol, Glenair, TE Connectivity, Smiths Interconnect, Bel Fuse, FilConn (Qnnect), ITT Cannon, Cristek Interconnects (Qnnect), Souriau-Sunbank (Eaton), Carlisle Interconnect Technologies, AEF Solutions, Spectrum Control (formerly APITech), Quell Corporation, RF Immunity, Conesys (EMP Connectors), Mil-Con |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |