What is Global Corrosion Resistant Dock Ladder Market?

The global Corrosion Resistant Dock Ladder market is a specialized segment within the broader marine and dock equipment industry. These ladders are designed to withstand harsh marine environments, where exposure to saltwater, humidity, and other corrosive elements is a constant challenge. Corrosion-resistant dock ladders are essential for ensuring safety and durability in various marine applications, including ports, marinas, and private docks. They are typically made from materials such as aluminum and stainless steel, which offer excellent resistance to rust and corrosion. The market for these ladders is driven by the increasing demand for durable and long-lasting marine infrastructure, as well as the growing awareness of safety standards in marine operations. With advancements in material science and manufacturing techniques, the global Corrosion Resistant Dock Ladder market is poised for steady growth, catering to the needs of both commercial and recreational marine sectors.

Aluminum Material, Stainless Steel Material in the Global Corrosion Resistant Dock Ladder Market:

Aluminum and stainless steel are the two primary materials used in the manufacturing of corrosion-resistant dock ladders, each offering distinct advantages. Aluminum is a lightweight yet strong material, making it an ideal choice for dock ladders that need to be easily maneuverable and installed without heavy lifting equipment. Its natural resistance to corrosion is enhanced through anodizing, a process that increases the thickness of the natural oxide layer on the surface, providing additional protection against the harsh marine environment. Aluminum dock ladders are also relatively low maintenance, requiring only occasional cleaning to remove salt deposits and other debris. On the other hand, stainless steel is renowned for its exceptional strength and durability. It is particularly well-suited for applications where the dock ladder will be subjected to heavy use or where additional structural integrity is required. Stainless steel's resistance to corrosion is due to the presence of chromium, which forms a passive layer of chromium oxide on the surface, preventing further oxidation. This makes stainless steel dock ladders highly resistant to rust, even in the most challenging marine conditions. Additionally, stainless steel ladders often have a polished finish, which not only enhances their aesthetic appeal but also makes them easier to clean and maintain. Both aluminum and stainless steel dock ladders are designed to meet stringent safety standards, ensuring that they provide reliable and secure access to and from the water. The choice between aluminum and stainless steel often comes down to specific application requirements, budget considerations, and personal preferences. While aluminum ladders are generally more affordable and easier to handle, stainless steel ladders offer superior strength and longevity, making them a worthwhile investment for high-traffic or commercial marine environments. Ultimately, the global Corrosion Resistant Dock Ladder market benefits from the unique properties of both materials, providing a range of options to meet the diverse needs of marine users.

Ports, Marinas, Other in the Global Corrosion Resistant Dock Ladder Market:

Corrosion-resistant dock ladders are widely used in various marine environments, including ports, marinas, and other waterfront areas. In ports, these ladders play a crucial role in ensuring the safety and efficiency of maritime operations. They provide secure access for personnel boarding and disembarking from ships, as well as for maintenance crews performing routine inspections and repairs. The durability and corrosion resistance of these ladders are particularly important in port settings, where they are exposed to constant use and harsh environmental conditions. In marinas, corrosion-resistant dock ladders are essential for both safety and convenience. They are commonly installed on docks and piers to facilitate easy access to and from boats and yachts. The non-corrosive properties of these ladders ensure that they remain functional and safe to use, even after prolonged exposure to saltwater and other corrosive elements. This is especially important in marinas, where the aesthetic appeal of the facilities is also a consideration, and the ladders need to maintain their appearance over time. Other waterfront areas, such as private docks, fishing piers, and recreational waterfronts, also benefit from the use of corrosion-resistant dock ladders. In these settings, the ladders provide a safe and reliable means of accessing the water for swimming, fishing, and other recreational activities. The low maintenance requirements of aluminum and stainless steel ladders make them an attractive option for private dock owners, who may not have the resources or inclination to perform frequent upkeep. Overall, the versatility and durability of corrosion-resistant dock ladders make them an indispensable component of marine infrastructure, enhancing safety and accessibility across a wide range of applications.

Global Corrosion Resistant Dock Ladder Market Outlook:

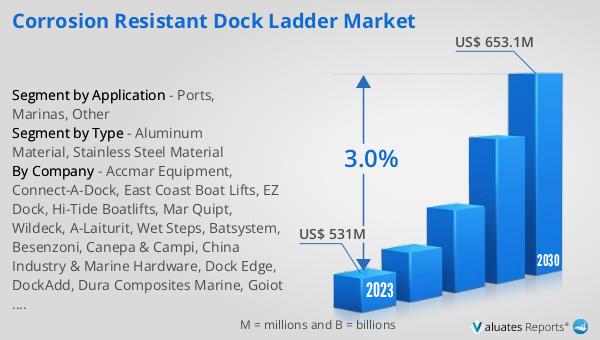

The global Corrosion Resistant Dock Ladder market was valued at US$ 531 million in 2023 and is anticipated to reach US$ 653.1 million by 2030, witnessing a CAGR of 3.0% during the forecast period 2024-2030. This market outlook highlights the steady growth trajectory of the industry, driven by the increasing demand for durable and long-lasting marine infrastructure. The market's expansion is supported by advancements in material science and manufacturing techniques, which have led to the development of more efficient and reliable corrosion-resistant dock ladders. As marine operations continue to prioritize safety and durability, the demand for high-quality dock ladders made from materials such as aluminum and stainless steel is expected to rise. These materials offer excellent resistance to rust and corrosion, ensuring that the ladders remain functional and safe to use even in the harshest marine environments. The market's growth is also fueled by the rising awareness of safety standards in marine operations, prompting both commercial and recreational marine sectors to invest in reliable and secure access solutions. With a projected CAGR of 3.0%, the global Corrosion Resistant Dock Ladder market is set to experience steady growth, catering to the diverse needs of marine users worldwide.

| Report Metric | Details |

| Report Name | Corrosion Resistant Dock Ladder Market |

| Accounted market size in 2023 | US$ 531 million |

| Forecasted market size in 2030 | US$ 653.1 million |

| CAGR | 3.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Accmar Equipment, Connect-A-Dock, East Coast Boat Lifts, EZ Dock, Hi-Tide Boatlifts, Mar Quipt, Wildeck, A-Laiturit, Wet Steps, Batsystem, Besenzoni, Canepa & Campi, China Industry & Marine Hardware, Dock Edge, DockAdd, Dura Composites Marine, Goiot Systems, Inland and Coastal Marina, Lindley Marinas, MarineMaster, MARTINI ALFREDO, NorSap AS |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |