What is Global Architecture Solar Control Film Market?

The Global Architecture Solar Control Film Market refers to the industry focused on producing and distributing films that are applied to windows in buildings to control the amount of solar energy that enters. These films are designed to reduce heat, glare, and ultraviolet (UV) radiation, thereby enhancing the comfort and energy efficiency of buildings. They are used in both residential and commercial settings to improve indoor environments and reduce energy costs associated with air conditioning. The market encompasses various types of films, including dyed, metalized, and ceramic films, each offering different levels of performance and aesthetic appeal. The demand for solar control films is driven by the growing awareness of energy conservation, the need for improved indoor comfort, and the desire to protect interiors from UV damage. Additionally, advancements in film technology and increasing regulations promoting energy efficiency in buildings are contributing to the market's growth. The global architecture solar control film market is a dynamic and evolving sector, with manufacturers continually innovating to meet the diverse needs of consumers and comply with environmental standards.

Common Coated, Vacuum Coated in the Global Architecture Solar Control Film Market:

Common Coated and Vacuum Coated films are two primary types of solar control films used in the global architecture market. Common Coated films are typically produced by applying a thin layer of metal or dye onto a polyester base. This coating helps to reflect or absorb solar energy, thereby reducing heat and glare inside buildings. These films are relatively cost-effective and offer a good balance between performance and price. They are widely used in both residential and commercial buildings due to their ease of installation and effectiveness in improving indoor comfort. On the other hand, Vacuum Coated films are manufactured using a more advanced process where metal or ceramic particles are deposited onto the film in a vacuum chamber. This method allows for a more uniform and durable coating, resulting in superior performance in terms of heat rejection and UV protection. Vacuum Coated films are often preferred for high-end applications where maximum efficiency and longevity are required. They are particularly popular in commercial buildings with large glass facades, as they can significantly reduce cooling costs and enhance the building's overall energy efficiency. Both types of films play a crucial role in the global architecture solar control film market, catering to different segments based on performance requirements and budget constraints. The choice between Common Coated and Vacuum Coated films depends on various factors, including the specific needs of the building, the local climate, and the desired level of solar control. As technology continues to advance, the performance gap between these two types of films is narrowing, offering consumers more options to choose from. Manufacturers are also focusing on developing eco-friendly coatings and improving the aesthetic appeal of these films to meet the growing demand for sustainable and visually pleasing building solutions. Overall, both Common Coated and Vacuum Coated films are essential components of the global architecture solar control film market, each offering unique benefits and catering to a wide range of applications.

Commercial Building, Residential Building in the Global Architecture Solar Control Film Market:

The usage of Global Architecture Solar Control Film Market in commercial buildings is extensive and multifaceted. In commercial settings, these films are primarily used to enhance energy efficiency and improve indoor comfort. By reducing the amount of solar heat that enters the building, solar control films help to lower cooling costs, which can be a significant expense for large commercial spaces. Additionally, these films reduce glare on computer screens and other electronic devices, creating a more comfortable and productive working environment for employees. They also protect interior furnishings, such as carpets, furniture, and artwork, from fading due to UV exposure. In high-rise office buildings with extensive glass facades, solar control films are particularly beneficial as they help to maintain a consistent indoor temperature, reducing the strain on HVAC systems and contributing to overall energy savings. In residential buildings, the use of solar control films is equally important. Homeowners install these films to create a more comfortable living environment by reducing heat and glare from the sun. This is especially beneficial in regions with hot climates, where excessive solar heat can make indoor spaces uncomfortable and increase reliance on air conditioning. Solar control films also provide privacy by reducing the visibility from outside without compromising the view from inside. Moreover, they protect household items, such as curtains, upholstery, and flooring, from UV damage, thereby extending their lifespan. The aesthetic appeal of solar control films is another factor driving their adoption in residential buildings. They are available in various shades and finishes, allowing homeowners to choose a film that complements their interior design while providing the desired level of solar control. Overall, the application of solar control films in both commercial and residential buildings offers numerous benefits, including energy savings, improved comfort, UV protection, and enhanced privacy, making them a valuable addition to modern architecture.

Global Architecture Solar Control Film Market Outlook:

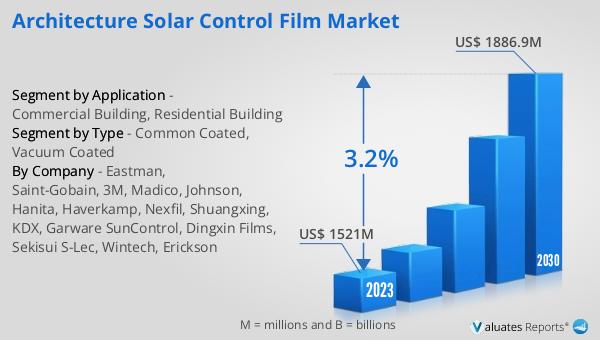

The global Architecture Solar Control Film market was valued at US$ 1521 million in 2023 and is anticipated to reach US$ 1886.9 million by 2030, witnessing a CAGR of 3.2% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory driven by increasing awareness of energy efficiency and the benefits of solar control films. The rising demand for sustainable building solutions and the need to reduce energy consumption in both residential and commercial buildings are key factors contributing to this growth. As more building owners and developers recognize the advantages of solar control films, such as reduced cooling costs, improved indoor comfort, and protection against UV damage, the market is expected to expand further. Additionally, advancements in film technology and the development of new, more efficient coatings are likely to enhance the performance and appeal of these films, attracting a broader customer base. The market's growth is also supported by regulatory initiatives promoting energy-efficient building practices and the increasing adoption of green building standards. Overall, the global architecture solar control film market is poised for significant growth in the coming years, driven by the ongoing demand for energy-efficient and sustainable building solutions.

| Report Metric | Details |

| Report Name | Architecture Solar Control Film Market |

| Accounted market size in 2023 | US$ 1521 million |

| Forecasted market size in 2030 | US$ 1886.9 million |

| CAGR | 3.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Eastman, Saint-Gobain, 3M, Madico, Johnson, Hanita, Haverkamp, Nexfil, Shuangxing, KDX, Garware SunControl, Dingxin Films, Sekisui S-Lec, Wintech, Erickson |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |