What is Global Laser Beam Diagnostic Devices Market?

The Global Laser Beam Diagnostic Devices Market refers to the worldwide industry focused on the development, production, and sale of devices used to analyze and measure laser beams. These devices are essential for ensuring the quality and performance of laser systems across various applications. They help in assessing parameters such as beam profile, power, wavelength, and divergence, which are crucial for optimizing laser performance and ensuring safety. The market encompasses a wide range of products, including beam profilers, power meters, spectrum analyzers, and wavefront sensors. These devices are used in diverse fields such as industrial manufacturing, medical diagnostics, telecommunications, and scientific research. The growing adoption of laser technology in these sectors is driving the demand for advanced diagnostic tools. Additionally, technological advancements and the increasing need for precision and accuracy in laser applications are further propelling market growth. Companies operating in this market are continuously innovating to offer more sophisticated and user-friendly diagnostic solutions. The market is characterized by a mix of established players and emerging startups, all striving to cater to the evolving needs of their customers.

Camera Type, Scanning Type in the Global Laser Beam Diagnostic Devices Market:

In the Global Laser Beam Diagnostic Devices Market, there are primarily two types of devices based on their operational mechanisms: Camera Type and Scanning Type. Camera Type devices utilize high-resolution cameras to capture the laser beam's profile and other characteristics. These devices are known for their ability to provide detailed and accurate measurements, making them ideal for applications requiring high precision. They can capture real-time data and offer a visual representation of the laser beam, which is particularly useful for troubleshooting and optimizing laser systems. Camera Type devices are widely used in research laboratories, medical diagnostics, and industrial quality control processes. On the other hand, Scanning Type devices employ scanning mechanisms to analyze the laser beam. These devices typically use rotating mirrors or other scanning elements to measure the beam's properties over time. Scanning Type devices are known for their robustness and ability to handle high-power lasers, making them suitable for industrial applications where durability and reliability are paramount. They can provide comprehensive data on beam parameters such as power distribution, divergence, and wavelength. While they may not offer the same level of detail as Camera Type devices, Scanning Type devices are valued for their ability to operate in harsh environments and their compatibility with high-power laser systems. Both types of devices play a crucial role in the laser beam diagnostic market, catering to different needs and applications. The choice between Camera Type and Scanning Type devices often depends on the specific requirements of the application, such as the level of detail needed, the power of the laser being analyzed, and the operating environment. As laser technology continues to advance, both Camera Type and Scanning Type devices are evolving to offer more sophisticated and user-friendly features. Manufacturers are focusing on enhancing the accuracy, reliability, and ease of use of these devices to meet the growing demands of their customers. The competition between Camera Type and Scanning Type devices is driving innovation in the market, leading to the development of new and improved diagnostic solutions. Overall, the Global Laser Beam Diagnostic Devices Market is witnessing significant growth, driven by the increasing adoption of laser technology across various sectors and the continuous advancements in diagnostic tools.

Industrial, Laboratory in the Global Laser Beam Diagnostic Devices Market:

The usage of Global Laser Beam Diagnostic Devices in industrial and laboratory settings is extensive and varied. In industrial applications, these devices are crucial for ensuring the quality and efficiency of laser-based manufacturing processes. Industries such as automotive, aerospace, electronics, and materials processing rely heavily on laser technology for cutting, welding, engraving, and additive manufacturing. Laser Beam Diagnostic Devices help in monitoring and optimizing these processes by providing precise measurements of beam parameters. For instance, in laser cutting and welding, the quality of the cut or weld is directly influenced by the laser beam's profile, power, and focus. Diagnostic devices enable operators to fine-tune these parameters, ensuring high-quality results and reducing material waste. Additionally, these devices play a vital role in maintaining the safety of laser operations by detecting any deviations or anomalies in the beam that could pose a risk to equipment or personnel. In laboratory settings, Laser Beam Diagnostic Devices are indispensable tools for scientific research and experimentation. Researchers use these devices to study the properties of lasers and their interactions with various materials. This includes fundamental research in physics, chemistry, and materials science, as well as applied research in fields such as photonics, telecommunications, and medical diagnostics. In a laboratory environment, the ability to accurately measure and analyze laser beams is essential for conducting experiments and validating theoretical models. For example, in photonics research, understanding the behavior of laser beams at different wavelengths and power levels is crucial for developing new optical devices and technologies. Similarly, in medical diagnostics, Laser Beam Diagnostic Devices are used to calibrate and optimize laser-based imaging and treatment systems, ensuring their accuracy and effectiveness. The versatility and precision of these devices make them invaluable tools for advancing scientific knowledge and technological innovation. Overall, the usage of Global Laser Beam Diagnostic Devices in industrial and laboratory settings highlights their importance in ensuring the quality, safety, and efficiency of laser applications. As laser technology continues to evolve and find new applications, the demand for advanced diagnostic tools is expected to grow, driving further innovation and development in this market.

Global Laser Beam Diagnostic Devices Market Outlook:

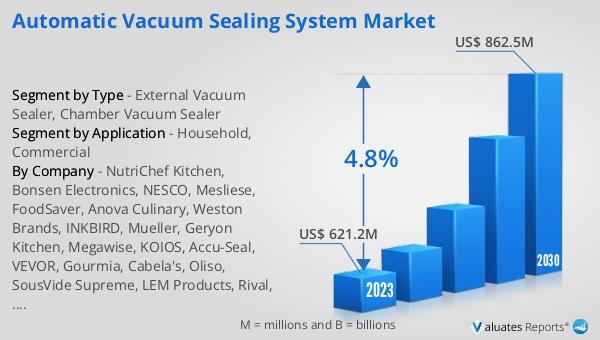

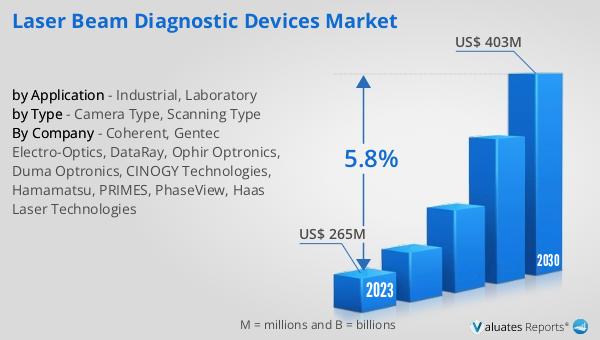

The global Laser Beam Diagnostic Devices market was valued at US$ 265 million in 2023 and is anticipated to reach US$ 403 million by 2030, witnessing a CAGR of 5.8% during the forecast period 2024-2030. This market outlook indicates a robust growth trajectory driven by the increasing adoption of laser technology across various sectors. The rising demand for precision and accuracy in laser applications is fueling the need for advanced diagnostic tools. Companies in this market are focusing on innovation and the development of user-friendly devices to cater to the evolving needs of their customers. The market is characterized by a mix of established players and emerging startups, all striving to offer more sophisticated and reliable diagnostic solutions. The continuous advancements in laser technology and the growing emphasis on quality control and safety are expected to further propel the market's growth. Overall, the Global Laser Beam Diagnostic Devices Market is poised for significant expansion, driven by the increasing use of lasers in industrial, medical, and research applications.

| Report Metric | Details |

| Report Name | Laser Beam Diagnostic Devices Market |

| Accounted market size in 2023 | US$ 265 million |

| Forecasted market size in 2030 | US$ 403 million |

| CAGR | 5.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Coherent, Gentec Electro-Optics, DataRay, Ophir Optronics, Duma Optronics, CINOGY Technologies, Hamamatsu, PRIMES, PhaseView, Haas Laser Technologies |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |