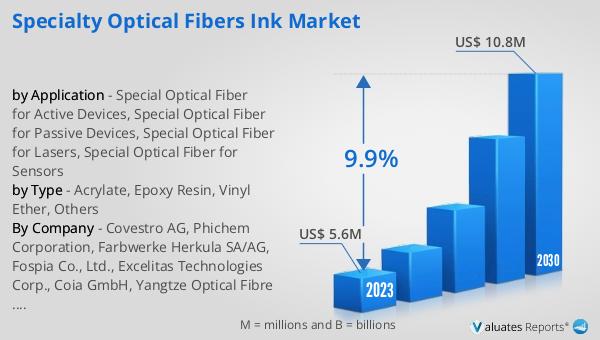

What is Global Optical Fiber Ink Market?

The Global Optical Fiber Ink Market refers to the industry that produces and supplies ink specifically designed for use in optical fibers. Optical fibers are thin strands of glass or plastic that transmit light signals over long distances, making them essential for telecommunications, medical imaging, and various other applications. The ink used in these fibers plays a crucial role in protecting the fibers, enhancing their performance, and ensuring their longevity. This market encompasses a wide range of products, including different types of inks formulated to meet the specific needs of various optical fiber applications. The demand for optical fiber ink is driven by the increasing adoption of optical fibers in various industries, the need for high-speed internet, and advancements in fiber optic technology. As the world becomes more connected and reliant on high-speed data transmission, the Global Optical Fiber Ink Market is expected to grow significantly, offering numerous opportunities for innovation and development in the field.

Acrylate, Epoxy Resin, Vinyl Ether, Others in the Global Optical Fiber Ink Market:

Acrylate, Epoxy Resin, Vinyl Ether, and other materials are essential components in the Global Optical Fiber Ink Market, each offering unique properties and benefits. Acrylate-based inks are widely used due to their excellent adhesion, flexibility, and fast curing times. These inks are particularly suitable for applications that require high durability and resistance to environmental factors such as UV light and moisture. Acrylates are also known for their low viscosity, which allows for easy application and smooth coating on optical fibers. Epoxy resin-based inks, on the other hand, are valued for their exceptional mechanical strength and chemical resistance. These inks provide a robust protective layer that can withstand harsh conditions, making them ideal for use in industrial and outdoor environments. Epoxy resins also offer good adhesion to a variety of substrates, ensuring a secure bond with the optical fibers. Vinyl Ether-based inks are another important category, known for their excellent flexibility and low shrinkage. These inks are often used in applications where maintaining the integrity of the optical fiber's shape and structure is critical. Vinyl Ethers also offer good chemical resistance and can be formulated to provide specific performance characteristics, such as enhanced thermal stability or improved adhesion to certain substrates. Other materials used in optical fiber inks include silicone-based inks, which offer excellent thermal stability and flexibility, and polyurethane-based inks, known for their toughness and abrasion resistance. Each of these materials brings its own set of advantages, allowing manufacturers to tailor their ink formulations to meet the specific requirements of different optical fiber applications. The choice of material depends on various factors, including the intended use of the optical fiber, the environmental conditions it will be exposed to, and the performance characteristics required. By leveraging the unique properties of these materials, the Global Optical Fiber Ink Market continues to innovate and develop new solutions to meet the evolving needs of the industry.

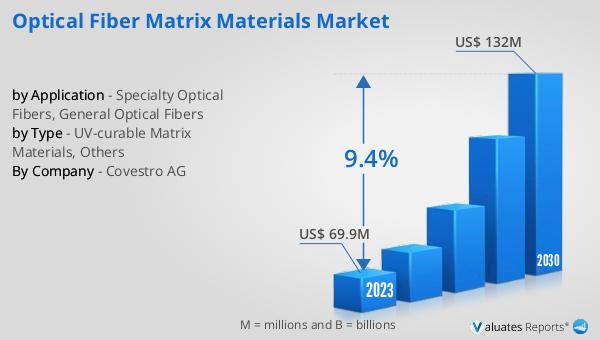

Specialty Optical Fibers, General Optical Fibers in the Global Optical Fiber Ink Market:

The usage of Global Optical Fiber Ink Market products can be broadly categorized into two main areas: Specialty Optical Fibers and General Optical Fibers. Specialty Optical Fibers are designed for specific applications that require unique performance characteristics. These fibers are often used in medical devices, sensors, and military applications, where precision and reliability are paramount. The inks used in specialty optical fibers must meet stringent standards for performance and durability. For example, in medical applications, the ink must be biocompatible and able to withstand sterilization processes. In military applications, the ink must provide robust protection against environmental factors such as extreme temperatures, humidity, and mechanical stress. The ability to customize ink formulations to meet these specific requirements is a key driver of innovation in the Global Optical Fiber Ink Market. General Optical Fibers, on the other hand, are used in a wide range of applications, including telecommunications, data centers, and residential internet connections. The primary function of the ink in these fibers is to protect the fiber from physical damage and environmental degradation. This includes providing resistance to UV light, moisture, and mechanical abrasion. In telecommunications, the ink must also ensure that the optical fiber maintains its performance over long distances and high data transmission rates. The growing demand for high-speed internet and the expansion of fiber optic networks globally are driving the need for high-quality optical fiber inks that can meet these performance standards. Additionally, the ink must be easy to apply and cure quickly to support efficient manufacturing processes. The versatility of optical fiber inks allows them to be used in a variety of other applications as well, such as in automotive and aerospace industries, where they help improve the performance and reliability of fiber optic systems. By addressing the specific needs of both specialty and general optical fibers, the Global Optical Fiber Ink Market plays a crucial role in supporting the advancement of fiber optic technology and its widespread adoption across different industries.

Global Optical Fiber Ink Market Outlook:

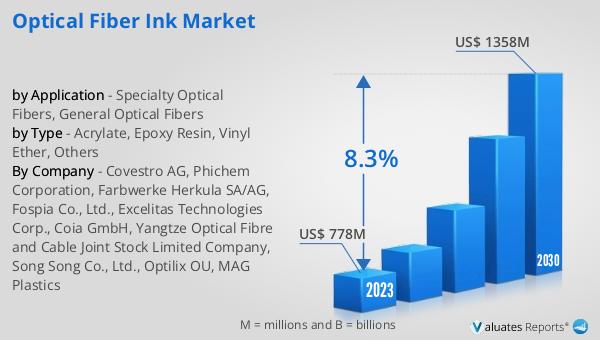

The global Optical Fiber Ink market was valued at US$ 778 million in 2023 and is anticipated to reach US$ 1358 million by 2030, witnessing a CAGR of 8.3% during the forecast period 2024-2030. This significant growth reflects the increasing demand for high-performance optical fiber inks driven by the expansion of fiber optic networks and the rising need for high-speed internet connectivity. The market's robust growth trajectory is also supported by advancements in fiber optic technology and the development of new ink formulations that offer enhanced performance and durability. As industries such as telecommunications, medical, and military continue to adopt optical fibers for their superior data transmission capabilities, the demand for specialized inks that can protect and enhance the performance of these fibers is expected to rise. The market's growth is further fueled by the increasing use of optical fibers in emerging applications such as smart cities, autonomous vehicles, and advanced manufacturing processes. By providing innovative solutions that meet the evolving needs of these industries, the Global Optical Fiber Ink Market is poised to play a critical role in shaping the future of fiber optic technology.

| Report Metric | Details |

| Report Name | Optical Fiber Ink Market |

| Accounted market size in 2023 | US$ 778 million |

| Forecasted market size in 2030 | US$ 1358 million |

| CAGR | 8.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Covestro AG, Phichem Corporation, Farbwerke Herkula SA/AG, Fospia Co., Ltd., Excelitas Technologies Corp., Coia GmbH, Yangtze Optical Fibre and Cable Joint Stock Limited Company, Song Song Co., Ltd., Optilix OU, MAG Plastics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |