What is Global Geophysical Ground Penetrating Radar Market?

The Global Geophysical Ground Penetrating Radar (GPR) Market refers to the worldwide industry focused on the development, production, and application of ground-penetrating radar technology. GPR is a non-invasive method that uses radar pulses to image the subsurface. This technology is widely used in various fields such as engineering, archaeology, geology, and environmental science to detect and map subsurface structures and features. The market encompasses a range of GPR systems, including handheld and cart-based models, each designed for specific applications and environments. The growth of this market is driven by the increasing demand for non-destructive testing methods, advancements in radar technology, and the expanding application areas of GPR. As industries continue to seek efficient and accurate methods for subsurface exploration, the Global Geophysical GPR Market is expected to see significant growth.

Handheld Ground Penetrating Radar, Cart Based Ground Penetrating Radar in the Global Geophysical Ground Penetrating Radar Market:

Handheld Ground Penetrating Radar (GPR) and Cart-Based Ground Penetrating Radar are two primary types of GPR systems used in the Global Geophysical GPR Market. Handheld GPR systems are portable and easy to use, making them ideal for quick surveys and hard-to-reach areas. These devices are commonly used in applications such as utility detection, concrete inspection, and small-scale archaeological investigations. Handheld GPR systems are favored for their mobility and ease of deployment, allowing operators to conduct surveys in confined spaces or rugged terrains where larger systems may not be practical. On the other hand, Cart-Based GPR systems are mounted on wheeled platforms, providing greater stability and the ability to cover larger areas more efficiently. These systems are typically used in applications that require extensive data collection, such as road and bridge inspections, large-scale archaeological surveys, and geological mapping. Cart-Based GPR systems offer higher data resolution and depth penetration compared to handheld models, making them suitable for more detailed and comprehensive surveys. Both types of GPR systems play a crucial role in the Global Geophysical GPR Market, catering to different needs and applications across various industries. The choice between handheld and cart-based GPR systems depends on factors such as the survey area, required data resolution, and specific application requirements. As technology continues to advance, both handheld and cart-based GPR systems are expected to become more sophisticated, offering improved performance and expanded capabilities.

Engineering Survey, Archaeological Investigation, Geological Hazard Investigation, Environmental Monitoring, Others in the Global Geophysical Ground Penetrating Radar Market:

The Global Geophysical Ground Penetrating Radar Market finds extensive usage in various areas, including Engineering Survey, Archaeological Investigation, Geological Hazard Investigation, Environmental Monitoring, and others. In Engineering Survey, GPR is used to detect and map subsurface utilities, voids, and other features that may affect construction projects. This helps engineers and construction professionals to plan and execute projects more efficiently, reducing the risk of damage to existing infrastructure. In Archaeological Investigation, GPR is used to locate and map buried artifacts, structures, and features without the need for excavation. This non-invasive method allows archaeologists to preserve the integrity of archaeological sites while gaining valuable insights into past human activities. Geological Hazard Investigation involves the use of GPR to identify and assess potential hazards such as sinkholes, landslides, and fault lines. By providing detailed subsurface images, GPR helps geologists to understand the underlying causes of geological hazards and develop mitigation strategies. Environmental Monitoring is another important application of GPR, where it is used to detect and monitor subsurface contamination, groundwater levels, and other environmental factors. This information is crucial for environmental scientists and policymakers to make informed decisions about environmental protection and remediation efforts. Other applications of GPR include forensic investigations, mining exploration, and military applications. The versatility and non-invasive nature of GPR make it a valuable tool in a wide range of fields, contributing to the growth and development of the Global Geophysical GPR Market.

Global Geophysical Ground Penetrating Radar Market Outlook:

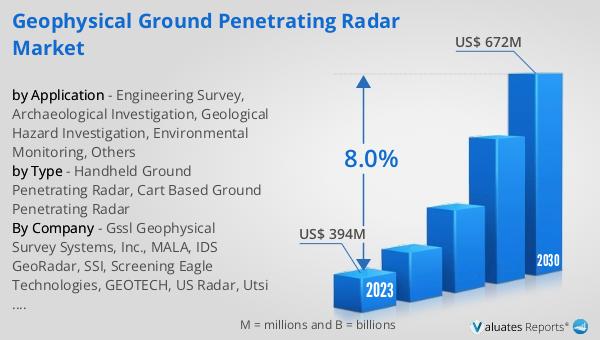

The global Geophysical Ground Penetrating Radar market was valued at US$ 394 million in 2023 and is anticipated to reach US$ 672 million by 2030, witnessing a CAGR of 8.0% during the forecast period 2024-2030. This significant growth reflects the increasing demand for advanced subsurface exploration technologies across various industries. The market's expansion is driven by factors such as the rising need for non-destructive testing methods, technological advancements in radar systems, and the growing application areas of GPR. As industries continue to seek efficient and accurate methods for subsurface exploration, the Global Geophysical GPR Market is expected to see substantial growth. The projected increase in market value underscores the importance of GPR technology in addressing the challenges of subsurface exploration and mapping. With continuous innovation and development, the Global Geophysical GPR Market is poised to play a crucial role in various fields, including engineering, archaeology, geology, and environmental science.

| Report Metric | Details |

| Report Name | Geophysical Ground Penetrating Radar Market |

| Accounted market size in 2023 | US$ 394 million |

| Forecasted market size in 2030 | US$ 672 million |

| CAGR | 8.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Gssl Geophysical Survey Systems, Inc., MALA, IDS GeoRadar, SSI, Screening Eagle Technologies, GEOTECH, US Radar, Utsi Electronics, Chemring Group, Radiodetection, Japan Radio Co, ChinaGPR, Kedian Reed |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |