What is Global Semiconductor IC Design, Manufacturing, Packaging and Testing Market?

The Global Semiconductor IC Design, Manufacturing, Packaging, and Testing Market is a comprehensive industry that encompasses the entire lifecycle of integrated circuits (ICs). This market involves several critical stages, starting from the initial design of the ICs, followed by their manufacturing, packaging, and finally, testing. IC design is the process where engineers create the blueprint of the semiconductor chip, defining its functionality and performance. Manufacturing involves the actual production of these chips, which is a highly sophisticated process requiring advanced technology and precision. Packaging is the next step, where the manufactured ICs are encased in protective materials to shield them from physical damage and environmental factors. Finally, testing ensures that the ICs meet the required standards and function correctly before they are shipped to customers. This market is crucial for the development of various electronic devices and systems, playing a significant role in the global technology landscape.

IC Design, IC Manufacturing, IC Packaging & Testing in the Global Semiconductor IC Design, Manufacturing, Packaging and Testing Market:

IC design is the foundational step in the semiconductor IC lifecycle, where engineers and designers use specialized software tools to create the architecture of the chip. This involves defining the chip's functions, performance parameters, and layout. The design process is critical as it determines the efficiency and capabilities of the final product. Once the design is finalized, it moves to the manufacturing phase. IC manufacturing is a complex process that involves multiple steps, including photolithography, doping, etching, and layering. These steps are carried out in cleanroom environments to prevent contamination and ensure precision. The manufacturing process requires state-of-the-art equipment and highly skilled personnel to produce high-quality semiconductor chips. After manufacturing, the chips undergo packaging, which involves encasing the ICs in protective materials. Packaging not only protects the chips from physical damage but also facilitates their integration into electronic devices. Different types of packaging are used depending on the application and requirements of the ICs. The final stage is testing, where the packaged ICs are subjected to various tests to ensure they meet the required specifications and performance standards. Testing is crucial as it helps identify any defects or issues before the chips are delivered to customers. The entire process of IC design, manufacturing, packaging, and testing is interconnected, with each stage playing a vital role in the production of reliable and efficient semiconductor chips. This market is essential for the advancement of technology and the development of innovative electronic devices.

Communication, Computer/PC, Consumer, Automotive, Industrial, Others in the Global Semiconductor IC Design, Manufacturing, Packaging and Testing Market:

The Global Semiconductor IC Design, Manufacturing, Packaging, and Testing Market finds extensive usage across various sectors, including communication, computer/PC, consumer electronics, automotive, industrial, and others. In the communication sector, semiconductor ICs are used in devices such as smartphones, tablets, and networking equipment. These ICs enable high-speed data transmission, signal processing, and connectivity, making them essential for modern communication systems. In the computer/PC sector, ICs are used in processors, memory chips, and other components that drive the performance of computers and laptops. They enable faster processing speeds, increased storage capacity, and improved overall performance. In the consumer electronics sector, semiconductor ICs are used in a wide range of devices, including televisions, gaming consoles, and home appliances. These ICs enhance the functionality and performance of consumer electronics, making them more efficient and user-friendly. In the automotive sector, semiconductor ICs are used in various applications, including engine control units, infotainment systems, and advanced driver-assistance systems (ADAS). These ICs improve the safety, efficiency, and connectivity of modern vehicles. In the industrial sector, semiconductor ICs are used in automation systems, robotics, and industrial machinery. They enable precise control, monitoring, and automation of industrial processes, leading to increased productivity and efficiency. Other sectors that utilize semiconductor ICs include healthcare, aerospace, and defense, where they are used in medical devices, avionics, and military equipment. The versatility and wide-ranging applications of semiconductor ICs make them indispensable in today's technology-driven world.

Global Semiconductor IC Design, Manufacturing, Packaging and Testing Market Outlook:

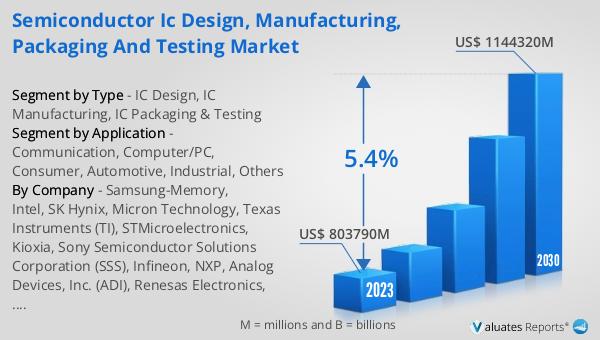

The global Semiconductor IC Design, Manufacturing, Packaging, and Testing market was valued at approximately $803.79 billion in 2023. Projections indicate that this market is expected to grow significantly, reaching around $1.144 trillion by 2030. This growth is anticipated to occur at a compound annual growth rate (CAGR) of 5.4% during the forecast period from 2024 to 2030. This market outlook highlights the increasing demand for semiconductor ICs across various industries, driven by advancements in technology and the growing need for high-performance electronic devices. The continuous innovation in IC design, manufacturing, packaging, and testing processes is expected to further fuel the growth of this market. The rising adoption of semiconductor ICs in emerging technologies such as artificial intelligence, the Internet of Things (IoT), and 5G communication is also contributing to the market's expansion. As the demand for more efficient and powerful electronic devices continues to rise, the global Semiconductor IC Design, Manufacturing, Packaging, and Testing market is poised for substantial growth in the coming years.

| Report Metric | Details |

| Report Name | Semiconductor IC Design, Manufacturing, Packaging and Testing Market |

| Accounted market size in 2023 | US$ 803790 million |

| Forecasted market size in 2030 | US$ 1144320 million |

| CAGR | 5.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Samsung-Memory, Intel, SK Hynix, Micron Technology, Texas Instruments (TI), STMicroelectronics, Kioxia, Sony Semiconductor Solutions Corporation (SSS), Infineon, NXP, Analog Devices, Inc. (ADI), Renesas Electronics, Microchip Technology, Onsemi, NVIDIA, Qualcomm, Broadcom, Advanced Micro Devices, Inc. (AMD), MediaTek, Marvell Technology Group, Novatek Microelectronics Corp., Tsinghua Unigroup, Realtek Semiconductor Corporation, OmniVision Technology, Inc, Monolithic Power Systems, Inc. (MPS), Cirrus Logic, Inc., Socionext Inc., LX Semicon, HiSilicon Technologies, TSMC, Samsung Foundry, GlobalFoundries, United Microelectronics Corporation (UMC), SMIC, Tower Semiconductor, PSMC, VIS (Vanguard International Semiconductor), Hua Hong Semiconductor, HLMC, ASE (SPIL), Amkor, JCET (STATS ChipPAC), Tongfu Microelectronics (TFME), Powertech Technology Inc. (PTI), HT-tech, King Yuan Electronics Corp. (KYEC), ChipMOS TECHNOLOGIES, SFA Semicon, Chipbond Technology Corporation, UTAC, ASML, TEL (Tokyo Electron Ltd.), Lam Research, KLA, Nikon, Carsem, Forehope Electronic (Ningbo) Co.,Ltd., Unisem Group, OSE CORP. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |