What is Global Electric Arc Furnace (EAF) Dust Recycling Market?

The Global Electric Arc Furnace (EAF) Dust Recycling Market refers to the industry focused on the collection, processing, and recycling of dust produced during the operation of electric arc furnaces in steelmaking. Electric arc furnaces are used to melt scrap steel, and during this process, a significant amount of dust is generated. This dust contains valuable metals such as zinc, lead, and iron, which can be recovered and reused. The recycling of EAF dust not only helps in reducing environmental pollution but also conserves natural resources by recovering these metals. The market encompasses various technologies and processes used to treat and recycle EAF dust, including both pyrometallurgical and hydrometallurgical methods. The demand for EAF dust recycling is driven by the increasing emphasis on sustainable practices in the steel industry and stringent environmental regulations. Companies operating in this market are continuously innovating to improve the efficiency and effectiveness of their recycling processes.

Pyrometallurgy, Hydrometallurgy in the Global Electric Arc Furnace (EAF) Dust Recycling Market:

Pyrometallurgy and hydrometallurgy are two primary methods used in the Global Electric Arc Furnace (EAF) Dust Recycling Market. Pyrometallurgy involves high-temperature processes to extract metals from EAF dust. This method typically includes steps such as roasting, smelting, and refining. During roasting, the EAF dust is heated in the presence of oxygen, which helps to convert metal compounds into oxides. These oxides are then smelted in a furnace to separate the metal from impurities. The final step, refining, involves further purification of the extracted metals. Pyrometallurgical processes are energy-intensive but are effective in recovering metals like zinc and lead from EAF dust. On the other hand, hydrometallurgy involves the use of aqueous solutions to extract metals from EAF dust. This method includes leaching, where the dust is treated with a solvent to dissolve the metal compounds. The resulting solution is then subjected to various chemical reactions to precipitate and recover the metals. Hydrometallurgical processes are generally considered to be more environmentally friendly compared to pyrometallurgical methods, as they operate at lower temperatures and produce fewer emissions. However, they can be more complex and require careful management of the chemical reagents used. Both pyrometallurgy and hydrometallurgy have their advantages and limitations, and the choice of method depends on factors such as the composition of the EAF dust, the specific metals to be recovered, and economic considerations. Companies in the EAF dust recycling market often use a combination of both methods to optimize metal recovery and minimize environmental impact.

Cement Industry, Steel Industry, Others in the Global Electric Arc Furnace (EAF) Dust Recycling Market:

The Global Electric Arc Furnace (EAF) Dust Recycling Market finds significant applications in various industries, including the cement industry, steel industry, and others. In the cement industry, EAF dust is used as an alternative raw material in the production of clinker, the primary component of cement. The high content of calcium and iron in EAF dust makes it suitable for use in cement manufacturing, helping to reduce the consumption of natural raw materials and lower production costs. Additionally, the recycling of EAF dust in the cement industry contributes to the reduction of waste and supports sustainable practices. In the steel industry, EAF dust recycling is crucial for recovering valuable metals such as zinc, lead, and iron. The recovered metals can be reused in the steelmaking process, reducing the need for virgin raw materials and lowering production costs. The recycling of EAF dust also helps steel manufacturers comply with environmental regulations by minimizing the disposal of hazardous waste. Furthermore, the steel industry benefits from the reduced environmental impact associated with the recycling of EAF dust, as it helps to decrease greenhouse gas emissions and conserve natural resources. Apart from the cement and steel industries, EAF dust recycling has applications in other sectors as well. For instance, the recovered zinc from EAF dust can be used in the production of zinc-based products such as galvanizing materials, batteries, and chemicals. The lead recovered from EAF dust can be used in the manufacturing of batteries, radiation shielding materials, and other lead-based products. The iron recovered from EAF dust can be used in various applications, including the production of iron-based alloys and as a raw material in the foundry industry. Overall, the recycling of EAF dust provides numerous benefits across different industries, including cost savings, resource conservation, and environmental protection.

Global Electric Arc Furnace (EAF) Dust Recycling Market Outlook:

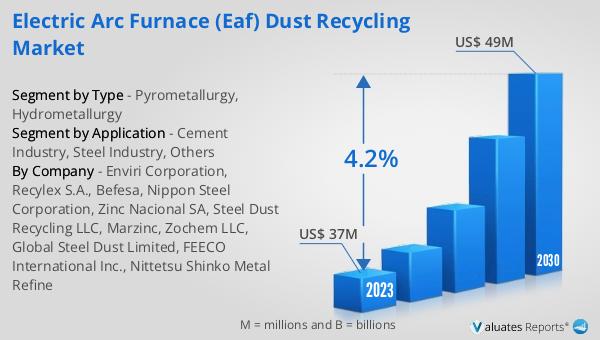

The global Electric Arc Furnace (EAF) Dust Recycling market was valued at US$ 37 million in 2023 and is anticipated to reach US$ 49 million by 2030, witnessing a CAGR of 4.2% during the forecast period 2024-2030. This growth can be attributed to the increasing emphasis on sustainable practices in the steel industry and stringent environmental regulations that mandate the proper disposal and recycling of EAF dust. The market is driven by the need to recover valuable metals such as zinc, lead, and iron from EAF dust, which not only helps in reducing environmental pollution but also conserves natural resources. Companies operating in this market are continuously innovating to improve the efficiency and effectiveness of their recycling processes, making it a dynamic and evolving industry. The adoption of advanced technologies and processes, such as pyrometallurgy and hydrometallurgy, plays a crucial role in enhancing metal recovery rates and minimizing environmental impact. As the demand for recycled metals continues to grow, the EAF dust recycling market is expected to witness significant growth in the coming years.

| Report Metric | Details |

| Report Name | Electric Arc Furnace (EAF) Dust Recycling Market |

| Accounted market size in 2023 | US$ 37 million |

| Forecasted market size in 2030 | US$ 49 million |

| CAGR | 4.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Enviri Corporation, Recylex S.A., Befesa, Nippon Steel Corporation, Zinc Nacional SA, Steel Dust Recycling LLC, Marzinc, Zochem LLC, Global Steel Dust Limited, FEECO International Inc., Nittetsu Shinko Metal Refine |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |