What is Global AI In Clinical Trials Market?

The Global AI in Clinical Trials Market refers to the integration of artificial intelligence technologies in the process of conducting clinical trials. Clinical trials are essential for testing the safety and efficacy of new drugs and treatments before they are approved for public use. AI can significantly enhance this process by analyzing vast amounts of data more quickly and accurately than traditional methods. This includes identifying suitable candidates for trials, predicting outcomes, and monitoring patient responses in real-time. The use of AI in clinical trials can lead to faster drug development, reduced costs, and improved patient outcomes. By leveraging machine learning algorithms, natural language processing, and other AI technologies, researchers can gain deeper insights into complex data sets, streamline trial processes, and make more informed decisions. This not only accelerates the pace of medical advancements but also ensures that new treatments are safe and effective for patients. The global market for AI in clinical trials is growing as more pharmaceutical companies, research organizations, and healthcare providers recognize the potential benefits of incorporating AI into their trial processes.

Software, Service in the Global AI In Clinical Trials Market:

In the Global AI in Clinical Trials Market, software and services play crucial roles in enhancing the efficiency and effectiveness of clinical trials. AI-powered software solutions are designed to handle various aspects of clinical trials, from patient recruitment to data analysis. These software tools use machine learning algorithms to sift through large datasets, identify patterns, and make predictions that can inform trial design and execution. For instance, AI software can analyze electronic health records to identify potential trial participants who meet specific criteria, thereby speeding up the recruitment process. Additionally, these tools can monitor patient data in real-time, providing researchers with immediate insights into patient responses and potential side effects. This real-time monitoring can help in making timely adjustments to the trial protocol, ensuring patient safety and improving the overall trial outcomes. On the other hand, AI services in clinical trials encompass a range of support activities provided by specialized firms. These services include data management, statistical analysis, and regulatory compliance support. Service providers often employ AI technologies to automate routine tasks, such as data entry and cleaning, which can significantly reduce the time and effort required for these activities. Moreover, AI-driven analytics services can offer deeper insights into trial data, helping researchers to identify trends and correlations that might not be apparent through traditional analysis methods. This can lead to more accurate and reliable results, ultimately enhancing the credibility of the trial findings. Furthermore, AI services can assist in ensuring that clinical trials comply with regulatory requirements. Regulatory bodies have stringent guidelines for conducting clinical trials, and non-compliance can result in significant delays or even the termination of a trial. AI technologies can help in maintaining accurate records, generating necessary documentation, and ensuring that all trial activities are conducted in accordance with regulatory standards. This not only helps in avoiding potential legal issues but also builds trust with stakeholders, including patients, healthcare providers, and regulatory authorities. In summary, the integration of AI software and services in clinical trials offers numerous benefits, including faster patient recruitment, real-time data monitoring, enhanced data analysis, and improved regulatory compliance. These advancements can lead to more efficient and effective clinical trials, ultimately accelerating the development of new treatments and improving patient outcomes. As the Global AI in Clinical Trials Market continues to grow, the adoption of these technologies is expected to become increasingly widespread, transforming the way clinical trials are conducted and paving the way for more innovative and effective healthcare solutions.

Pharmaceutical and Biotechnology Companies, Contract Research Organization, Other in the Global AI In Clinical Trials Market:

The usage of AI in clinical trials is particularly significant for pharmaceutical and biotechnology companies, contract research organizations (CROs), and other stakeholders involved in the drug development process. Pharmaceutical and biotechnology companies are at the forefront of adopting AI technologies to streamline their clinical trial processes. These companies invest heavily in research and development to bring new drugs to market, and the integration of AI can significantly reduce the time and cost associated with clinical trials. AI can help these companies in various ways, such as identifying potential drug candidates, predicting patient responses, and optimizing trial designs. By leveraging AI, pharmaceutical and biotechnology companies can accelerate the drug development process, bringing new treatments to market more quickly and efficiently. Contract Research Organizations (CROs) also play a crucial role in the Global AI in Clinical Trials Market. CROs are specialized firms that provide support to pharmaceutical and biotechnology companies in conducting clinical trials. These organizations often handle multiple trials simultaneously, making efficiency and accuracy critical to their operations. AI technologies can help CROs manage large volumes of data, automate routine tasks, and provide real-time insights into trial progress. This can lead to more efficient trial management, reduced costs, and improved trial outcomes. Additionally, AI can assist CROs in ensuring regulatory compliance, which is essential for the successful completion of clinical trials. Other stakeholders, such as academic institutions, government agencies, and non-profit organizations, also benefit from the integration of AI in clinical trials. Academic institutions often conduct clinical trials as part of their research activities, and AI can help them analyze complex data sets, identify trends, and generate new insights. Government agencies and non-profit organizations, on the other hand, may be involved in funding or overseeing clinical trials. AI can assist these organizations in monitoring trial progress, ensuring compliance with regulatory standards, and evaluating the effectiveness of new treatments. By leveraging AI, these stakeholders can contribute to the advancement of medical research and the development of new therapies. In conclusion, the usage of AI in clinical trials offers significant benefits to pharmaceutical and biotechnology companies, contract research organizations, and other stakeholders involved in the drug development process. By enhancing efficiency, reducing costs, and improving trial outcomes, AI technologies are transforming the way clinical trials are conducted. As the Global AI in Clinical Trials Market continues to grow, the adoption of these technologies is expected to become increasingly widespread, leading to more innovative and effective healthcare solutions.

Global AI In Clinical Trials Market Outlook:

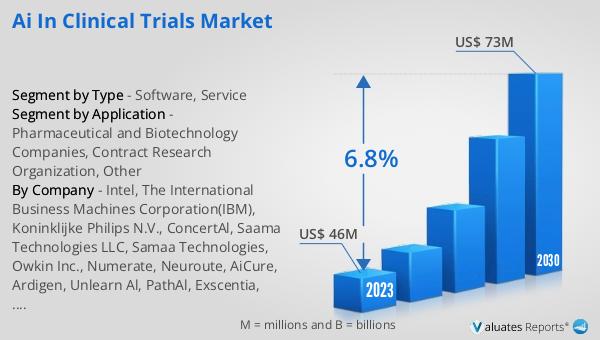

The global market for AI in clinical trials was valued at $46 million in 2023 and is projected to grow to $73 million by 2030, reflecting a compound annual growth rate (CAGR) of 6.8% during the forecast period from 2024 to 2030. This growth is indicative of the increasing recognition of the benefits that AI technologies bring to the clinical trial process. The ability of AI to analyze large datasets quickly and accurately, identify suitable trial participants, predict outcomes, and monitor patient responses in real-time is driving its adoption across the pharmaceutical and biotechnology sectors. As more companies and research organizations integrate AI into their clinical trial processes, the market is expected to expand further. This growth also underscores the potential of AI to revolutionize the drug development process, making it more efficient, cost-effective, and capable of delivering better patient outcomes. The projected increase in market value highlights the significant impact that AI is expected to have on the future of clinical trials and the broader healthcare industry.

| Report Metric | Details |

| Report Name | AI In Clinical Trials Market |

| Accounted market size in 2023 | US$ 46 million |

| Forecasted market size in 2030 | US$ 73 million |

| CAGR | 6.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Intel, The International Business Machines Corporation(IBM), Koninklijke Philips N.V., ConcertAl, Saama Technologies LLC, Samaa Technologies, Owkin Inc., Numerate, Neuroute, AiCure, Ardigen, Unlearn Al, PathAl, Exscentia, Aitia Infotech Pvt Ltd., Euretos, VeriSIM Life, Envisagenics, NURITAs, BioSymetrics, BioAge Labs lInc |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |