What is Global Power Assisted Liposuction System Market?

The Global Power Assisted Liposuction System Market refers to the worldwide industry focused on the development, production, and distribution of advanced liposuction devices that utilize power assistance to enhance the efficiency and precision of fat removal procedures. These systems are designed to assist surgeons by providing mechanical support, reducing manual effort, and improving the overall outcomes of liposuction surgeries. The market encompasses a variety of technologies and devices, including vibrating, rotary, and pneumatic systems, each offering unique benefits and applications. The increasing demand for minimally invasive cosmetic procedures, coupled with advancements in medical technology, has driven the growth of this market. Additionally, the rising prevalence of obesity and the growing awareness of body contouring options have further fueled the adoption of power-assisted liposuction systems globally. As a result, the market has seen significant investments in research and development, leading to the introduction of innovative products that cater to the evolving needs of both patients and healthcare providers.

Vibrating Intubation System, Rotary Intubation System, Pneumatic Intubation System, Other in the Global Power Assisted Liposuction System Market:

The Global Power Assisted Liposuction System Market includes various types of systems such as Vibrating Intubation Systems, Rotary Intubation Systems, Pneumatic Intubation Systems, and others. Vibrating Intubation Systems use high-frequency vibrations to break down fat cells, making it easier to remove them with minimal trauma to surrounding tissues. This technology is particularly beneficial for treating fibrous areas and achieving smoother results. Rotary Intubation Systems, on the other hand, employ a rotating cannula that helps in the emulsification of fat, allowing for more efficient aspiration. This method is known for its precision and ability to target specific areas with greater control. Pneumatic Intubation Systems utilize compressed air to power the cannula, providing consistent and controlled movements that enhance the surgeon's ability to remove fat evenly. These systems are often preferred for their reliability and ease of use. Other types of power-assisted liposuction systems may incorporate a combination of these technologies or introduce new innovations to further improve the safety and effectiveness of the procedure. Each type of system offers distinct advantages, making them suitable for different clinical scenarios and patient needs. The choice of system often depends on the surgeon's preference, the specific requirements of the procedure, and the desired outcomes. As the market continues to evolve, ongoing research and development efforts are expected to bring forth new advancements that will further refine these technologies and expand their applications in the field of cosmetic surgery.

Hospital, Ambulatory Surgery Center, Cosmetic Surgery Center in the Global Power Assisted Liposuction System Market:

The usage of Global Power Assisted Liposuction System Market in hospitals, ambulatory surgery centers, and cosmetic surgery centers is extensive and varied. In hospitals, these systems are primarily used for medical purposes, such as treating patients with lipodystrophy or other conditions that require the removal of excess fat. The advanced technology of power-assisted liposuction systems allows for more precise and efficient fat removal, reducing the risk of complications and improving patient outcomes. Hospitals often have the infrastructure and resources to support complex procedures, making them ideal settings for the use of these advanced systems. Ambulatory Surgery Centers (ASCs) also benefit significantly from power-assisted liposuction systems. ASCs are designed to provide same-day surgical care, including diagnostic and preventive procedures. The minimally invasive nature of power-assisted liposuction makes it well-suited for these centers, as it allows for quicker recovery times and reduced hospital stays. Patients can undergo the procedure and return home the same day, which is a significant advantage in terms of convenience and cost-effectiveness. Cosmetic Surgery Centers are perhaps the most prominent users of power-assisted liposuction systems. These centers specialize in aesthetic procedures aimed at enhancing the appearance of patients. The precision and efficiency offered by power-assisted liposuction systems make them ideal for body contouring and sculpting. Surgeons can achieve more consistent and natural-looking results, which is a critical factor in patient satisfaction. Additionally, the reduced recovery time and lower risk of complications associated with these systems make them highly attractive to patients seeking cosmetic enhancements. Overall, the versatility and effectiveness of power-assisted liposuction systems have made them indispensable tools in various healthcare settings, contributing to better patient outcomes and higher satisfaction rates.

Global Power Assisted Liposuction System Market Outlook:

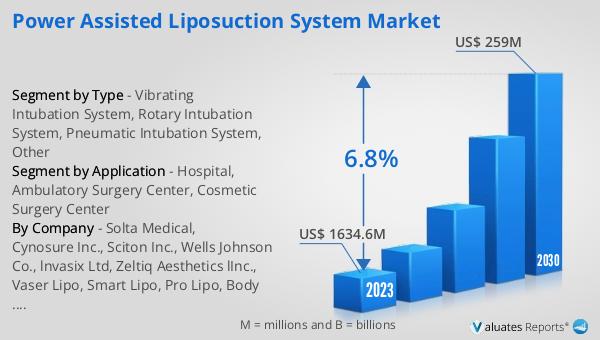

The global Power Assisted Liposuction System market was valued at US$ 1634.6 million in 2023 and is anticipated to reach US$ 259 million by 2030, witnessing a CAGR of 6.8% during the forecast period 2024-2030. This market outlook highlights the significant growth potential of the industry, driven by increasing demand for minimally invasive cosmetic procedures and advancements in medical technology. The projected growth rate underscores the expanding adoption of power-assisted liposuction systems across various healthcare settings, including hospitals, ambulatory surgery centers, and cosmetic surgery centers. The market's robust valuation in 2023 reflects the widespread acceptance and utilization of these advanced systems, which offer numerous benefits such as improved precision, reduced recovery times, and enhanced patient outcomes. As the market continues to evolve, ongoing research and development efforts are expected to introduce new innovations that will further drive growth and expand the applications of power-assisted liposuction systems. The anticipated market value of US$ 259 million by 2030 signifies the increasing recognition of the importance of these systems in modern medical and cosmetic practices. The consistent CAGR of 6.8% during the forecast period indicates a steady and sustained growth trajectory, highlighting the resilience and potential of the global Power Assisted Liposuction System market.

| Report Metric | Details |

| Report Name | Power Assisted Liposuction System Market |

| Accounted market size in 2023 | US$ 1634.6 million |

| Forecasted market size in 2030 | US$ 259 million |

| CAGR | 6.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Solta Medical, Cynosure Inc., Sciton Inc., Wells Johnson Co., lnvasix Ltd, Zeltiq Aesthetics lInc., Vaser Lipo, Smart Lipo, Pro Lipo, Body Tite, Cool Sculpt, Liposonix |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |