What is Global Oatcakes Market?

The global oatcakes market is a fascinating segment within the broader food industry, characterized by its unique blend of tradition and modernity. Oatcakes, which are essentially biscuits made from oats, have been a staple in various cultures for centuries. They are known for their nutritional benefits, including high fiber content, which aids in digestion and provides a sustained energy release. The market for oatcakes has seen significant growth due to increasing consumer awareness about healthy eating habits and the rising demand for convenient, nutritious snacks. This market encompasses a wide range of products, from traditional recipes to innovative flavors and formulations that cater to diverse consumer preferences. The global reach of oatcakes is evident as they are popular in regions like North America, Europe, and Asia, each with its own unique twist on the classic oatcake. The market is also influenced by factors such as changing lifestyles, increasing disposable incomes, and the growing trend of on-the-go snacking. As more people seek healthier alternatives to conventional snacks, the demand for oatcakes is expected to continue its upward trajectory, making it a dynamic and evolving market to watch.

Original Flavor, Cheese Flavor, Other in the Global Oatcakes Market:

When it comes to flavors in the global oatcakes market, the variety is both vast and intriguing. Original flavor oatcakes are the most traditional and widely recognized. They are typically made with simple ingredients like oats, water, and a pinch of salt, offering a wholesome and natural taste that appeals to purists and health-conscious consumers alike. These oatcakes are versatile and can be enjoyed on their own or paired with a variety of toppings, from cheese to jam, making them a staple in many households. On the other hand, cheese-flavored oatcakes bring a savory twist to the classic recipe. These oatcakes are often infused with different types of cheese, such as cheddar or parmesan, providing a rich and indulgent flavor profile. Cheese-flavored oatcakes are particularly popular as a snack option or as an accompaniment to soups and salads. They cater to those who enjoy a more robust and savory taste, adding a layer of complexity to the traditional oatcake. Beyond the original and cheese flavors, the market also offers a plethora of other varieties. These can include sweet options like honey and cinnamon, which add a touch of sweetness and spice, making them perfect for breakfast or dessert. There are also oatcakes with added seeds and nuts, providing extra crunch and nutritional benefits. These variations cater to the growing demand for functional foods that offer additional health benefits beyond basic nutrition. Moreover, the market has seen the introduction of gluten-free oatcakes, catering to consumers with specific dietary needs. These oatcakes are made with gluten-free oats and other alternative ingredients, ensuring that everyone can enjoy the benefits of oatcakes without compromising on taste or texture. The diversity in flavors and formulations within the global oatcakes market reflects the evolving consumer preferences and the industry's ability to innovate and adapt. Whether it's the simplicity of the original flavor, the savory richness of cheese, or the unique combinations found in other varieties, there is an oatcake to suit every palate. This wide range of options not only enhances the appeal of oatcakes but also drives their popularity across different demographics and regions. As the market continues to grow, we can expect even more exciting and innovative flavors to emerge, further solidifying oatcakes' position as a beloved and versatile snack.

Supermarket, Specialty Store, Online Sales, Other in the Global Oatcakes Market:

The global oatcakes market finds its usage across various retail channels, each playing a crucial role in making these nutritious snacks accessible to consumers. Supermarkets are one of the primary distribution channels for oatcakes. They offer a wide range of brands and flavors, making it convenient for consumers to find their preferred oatcakes during their regular grocery shopping. Supermarkets often have dedicated sections for health foods, where oatcakes are prominently displayed, attracting health-conscious shoppers. The availability of oatcakes in supermarkets also ensures that they reach a broad audience, from busy professionals looking for a quick snack to families seeking healthy options for their children. Specialty stores, on the other hand, cater to a more niche market. These stores often focus on organic, gluten-free, or gourmet products, and oatcakes fit perfectly into these categories. Specialty stores provide a curated shopping experience, where consumers can find high-quality oatcakes that may not be available in mainstream supermarkets. This channel is particularly important for consumers with specific dietary needs or those who are looking for unique and artisanal oatcake varieties. Online sales have become increasingly significant in the global oatcakes market, especially with the rise of e-commerce and changing consumer shopping habits. Online platforms offer the convenience of shopping from home, with the added benefit of a wider selection of products. Consumers can easily compare different brands, read reviews, and make informed purchasing decisions. Online sales also allow for direct-to-consumer models, where oatcake manufacturers can sell their products directly to customers, bypassing traditional retail channels. This not only increases the reach of oatcakes but also allows for better customer engagement and feedback. Other distribution channels, such as convenience stores and health food stores, also play a role in the oatcakes market. Convenience stores provide a quick and easy option for consumers looking for a healthy snack on the go. Health food stores, similar to specialty stores, focus on products that cater to specific health and wellness needs. These stores often carry a variety of oatcakes, including those that are organic, gluten-free, or enriched with additional nutrients. The diverse range of retail channels ensures that oatcakes are accessible to a wide audience, catering to different preferences and shopping habits. Each channel has its unique advantages, contributing to the overall growth and popularity of oatcakes in the global market. As consumer demand for healthy and convenient snacks continues to rise, the presence of oatcakes across these various channels is likely to expand, further solidifying their position as a staple in the snack food industry.

Global Oatcakes Market Outlook:

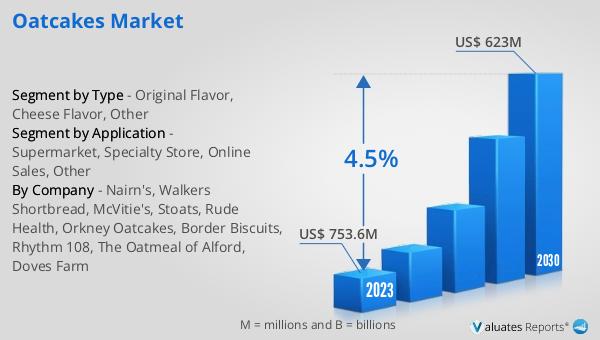

The global oatcakes market was valued at approximately $753.6 million in 2023. Looking ahead, it is expected to reach around $623 million by 2030, reflecting a compound annual growth rate (CAGR) of 4.5% during the forecast period from 2024 to 2030. This market outlook indicates a steady growth trajectory, driven by increasing consumer awareness about the health benefits of oats and the rising demand for convenient, nutritious snacks. The projected growth rate suggests that the market will continue to expand, albeit at a moderate pace, as more consumers incorporate oatcakes into their daily diets. The anticipated market value by 2030 underscores the potential for oatcakes to become a more prominent player in the global snack food industry. This growth is likely to be supported by ongoing product innovation, expanding distribution channels, and the increasing popularity of healthy eating trends. As the market evolves, oatcake manufacturers will need to stay attuned to consumer preferences and continue to offer products that meet the demand for both taste and nutrition. The steady CAGR of 4.5% reflects a positive outlook for the global oatcakes market, highlighting its resilience and potential for sustained growth in the coming years.

| Report Metric | Details |

| Report Name | Oatcakes Market |

| Accounted market size in 2023 | US$ 753.6 million |

| Forecasted market size in 2030 | US$ 623 million |

| CAGR | 4.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Nairn's, Walkers Shortbread, McVitie's, Stoats, Rude Health, Orkney Oatcakes, Border Biscuits, Rhythm 108, The Oatmeal of Alford, Doves Farm |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |