What is Global Oral Health Ingredient Market?

The Global Oral Health Ingredient Market encompasses a wide range of components used in products designed to maintain and improve oral hygiene. These ingredients are found in everyday items such as toothpaste, mouthwash, dental floss, and other oral care products. The market includes both natural and synthetic ingredients, each serving specific functions like cleaning, whitening, and protecting teeth and gums. The demand for oral health ingredients is driven by increasing awareness about oral hygiene, rising incidences of dental problems, and the growing popularity of natural and organic products. Additionally, advancements in dental care technology and the development of innovative products are contributing to the market's growth. The market is also influenced by regulatory standards and consumer preferences, which vary across different regions. Overall, the Global Oral Health Ingredient Market plays a crucial role in the broader healthcare industry by providing essential components that help maintain oral health and prevent dental diseases.

Bio-based, Synthetic in the Global Oral Health Ingredient Market:

Bio-based and synthetic ingredients are two primary categories within the Global Oral Health Ingredient Market. Bio-based ingredients are derived from natural sources such as plants, animals, and minerals. These ingredients are often preferred by consumers seeking natural and organic products. Common bio-based ingredients include essential oils like peppermint and tea tree oil, which have antibacterial properties, and natural abrasives like baking soda and silica, which help in cleaning and whitening teeth. Other examples include xylitol, a natural sweetener that helps reduce tooth decay, and aloe vera, known for its soothing and healing properties. On the other hand, synthetic ingredients are chemically manufactured and are designed to mimic or enhance the properties of natural ingredients. These include fluoride, which is widely used for its ability to strengthen tooth enamel and prevent cavities, and triclosan, an antibacterial agent that helps reduce plaque and gingivitis. Synthetic abrasives like hydrated silica and calcium carbonate are also commonly used in toothpaste for their effective cleaning properties. Both bio-based and synthetic ingredients have their advantages and limitations. Bio-based ingredients are generally perceived as safer and more environmentally friendly, but they may not always provide the same level of efficacy as synthetic ingredients. Synthetic ingredients, while highly effective, can sometimes cause side effects or raise concerns about long-term safety. The choice between bio-based and synthetic ingredients often depends on consumer preferences, regulatory requirements, and the specific needs of the oral care product. Manufacturers in the Global Oral Health Ingredient Market are increasingly focusing on developing products that combine the benefits of both bio-based and synthetic ingredients to offer effective and safe oral care solutions. This approach not only caters to the growing demand for natural products but also ensures that the products meet the high standards of efficacy and safety required by consumers and regulatory bodies.

Toothpaste, Mouthwash in the Global Oral Health Ingredient Market:

The Global Oral Health Ingredient Market finds extensive usage in products like toothpaste and mouthwash, which are essential for maintaining oral hygiene. Toothpaste is one of the most commonly used oral care products, and it contains a variety of ingredients that serve different functions. Abrasives like calcium carbonate and hydrated silica help remove plaque and stains from teeth, while fluoride strengthens tooth enamel and prevents cavities. Humectants such as glycerin and sorbitol keep the toothpaste moist and prevent it from drying out. Thickeners like xanthan gum and carrageenan give toothpaste its smooth texture, and flavoring agents like peppermint oil provide a refreshing taste. Additionally, toothpaste may contain antibacterial agents like triclosan to reduce plaque and gingivitis, and whitening agents like hydrogen peroxide to help remove surface stains. Mouthwash, another popular oral care product, also contains a range of ingredients that contribute to oral health. Antiseptic agents like chlorhexidine and cetylpyridinium chloride help kill bacteria and reduce plaque, while fluoride strengthens teeth and prevents cavities. Humectants like glycerin keep the mouthwash from drying out, and flavoring agents provide a pleasant taste. Some mouthwashes also contain natural ingredients like aloe vera and tea tree oil, which have soothing and antibacterial properties. The choice of ingredients in toothpaste and mouthwash depends on the specific needs of the product and the target consumer. For example, toothpaste designed for sensitive teeth may contain potassium nitrate or strontium chloride to help reduce sensitivity, while mouthwash formulated for dry mouth may include ingredients like xylitol and aloe vera to provide moisture and relief. Overall, the Global Oral Health Ingredient Market plays a crucial role in the development of effective and safe oral care products that help maintain oral hygiene and prevent dental problems.

Global Oral Health Ingredient Market Outlook:

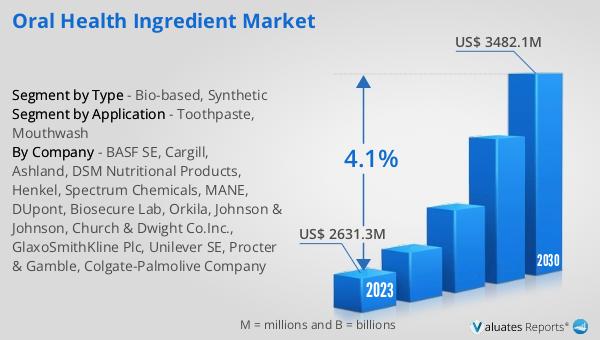

The global Oral Health Ingredient market was valued at US$ 2631.3 million in 2023 and is anticipated to reach US$ 3482.1 million by 2030, witnessing a CAGR of 4.1% during the forecast period 2024-2030. This market growth reflects the increasing awareness and importance of oral hygiene among consumers worldwide. The rising incidences of dental problems, coupled with the growing popularity of natural and organic oral care products, are driving the demand for oral health ingredients. Additionally, advancements in dental care technology and the development of innovative products are contributing to the market's expansion. The market is also influenced by regulatory standards and consumer preferences, which vary across different regions. Manufacturers are focusing on developing products that combine the benefits of both bio-based and synthetic ingredients to offer effective and safe oral care solutions. This approach not only caters to the growing demand for natural products but also ensures that the products meet the high standards of efficacy and safety required by consumers and regulatory bodies. Overall, the Global Oral Health Ingredient Market plays a crucial role in the broader healthcare industry by providing essential components that help maintain oral health and prevent dental diseases.

| Report Metric | Details |

| Report Name | Oral Health Ingredient Market |

| Accounted market size in 2023 | US$ 2631.3 million |

| Forecasted market size in 2030 | US$ 3482.1 million |

| CAGR | 4.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | BASF SE, Cargill, Ashland, DSM Nutritional Products, Henkel, Spectrum Chemicals, MANE, DUpont, Biosecure Lab, Orkila, Johnson & Johnson, Church & Dwight Co.Inc., GlaxoSmithKline Plc, Unilever SE, Procter & Gamble, Colgate-Palmolive Company |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |