What is Global Light Electric Commercial Vehicles Market?

The Global Light Electric Commercial Vehicles Market refers to the worldwide industry focused on the production, distribution, and utilization of light electric vehicles (LEVs) designed for commercial purposes. These vehicles are typically powered by electric batteries and are used for various commercial activities such as transportation of goods, passenger services, and other business operations. The market encompasses a wide range of vehicles including electric vans, trucks, buses, and other light commercial vehicles. The shift towards electric vehicles in the commercial sector is driven by the need to reduce carbon emissions, lower operational costs, and comply with stringent environmental regulations. Additionally, advancements in battery technology, increasing fuel prices, and government incentives are further propelling the growth of this market. The adoption of light electric commercial vehicles is seen as a sustainable solution to address the challenges of urban congestion, pollution, and the rising demand for efficient and eco-friendly transportation options. As businesses and governments worldwide continue to prioritize sustainability, the Global Light Electric Commercial Vehicles Market is expected to witness significant growth in the coming years.

≤200kWh, >200kWh in the Global Light Electric Commercial Vehicles Market:

In the Global Light Electric Commercial Vehicles Market, the classification based on battery capacity is crucial for understanding the performance and application of these vehicles. Vehicles with a battery capacity of ≤200kWh are generally designed for shorter routes and lighter loads. These vehicles are ideal for urban deliveries, last-mile logistics, and other short-distance commercial activities. They offer the advantage of lower initial costs and are easier to charge, making them suitable for businesses with limited infrastructure. On the other hand, vehicles with a battery capacity of >200kWh are built for longer distances and heavier loads. These vehicles are equipped with more powerful batteries that provide extended range and higher payload capacity, making them suitable for intercity transportation, long-haul logistics, and other demanding commercial operations. The higher battery capacity also translates to longer charging times and higher costs, but the benefits in terms of range and performance often outweigh these drawbacks. The choice between ≤200kWh and >200kWh vehicles depends on the specific needs of the business, including the nature of the goods being transported, the distance to be covered, and the availability of charging infrastructure. As battery technology continues to evolve, the efficiency and performance of both categories are expected to improve, further enhancing their appeal to commercial users. The Global Light Electric Commercial Vehicles Market is thus characterized by a diverse range of vehicles catering to different commercial needs, with battery capacity being a key differentiator in terms of performance and application.

Coach, Truck, Others in the Global Light Electric Commercial Vehicles Market:

The usage of Global Light Electric Commercial Vehicles Market spans across various sectors, including coaches, trucks, and other commercial vehicles. In the coach segment, electric coaches are increasingly being adopted for public transportation, tourism, and corporate travel. These vehicles offer a quieter and more comfortable ride compared to traditional diesel-powered coaches, making them an attractive option for passengers. Additionally, electric coaches contribute to reducing air pollution and greenhouse gas emissions, aligning with the sustainability goals of many cities and organizations. In the truck segment, electric trucks are being used for a wide range of applications, from urban deliveries to long-haul transportation. They are particularly beneficial for last-mile delivery services, where the shorter distances and frequent stops make electric trucks a cost-effective and environmentally friendly option. The reduced noise levels of electric trucks also make them suitable for nighttime deliveries in residential areas. Other commercial vehicles in the Global Light Electric Commercial Vehicles Market include electric vans, minibuses, and specialized vehicles such as electric garbage trucks and street sweepers. These vehicles are used in various industries, including logistics, construction, and public services. The versatility and environmental benefits of electric commercial vehicles make them an attractive choice for businesses looking to reduce their carbon footprint and operational costs. As technology advances and charging infrastructure improves, the adoption of electric commercial vehicles is expected to increase across all these segments, further driving the growth of the Global Light Electric Commercial Vehicles Market.

Global Light Electric Commercial Vehicles Market Outlook:

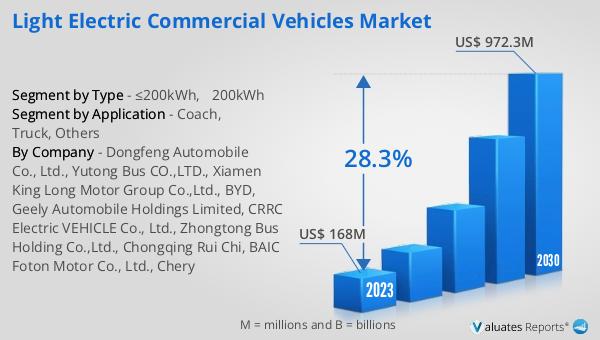

The global Light Electric Commercial Vehicles market was valued at US$ 168 million in 2023 and is anticipated to reach US$ 972.3 million by 2030, witnessing a CAGR of 28.3% during the forecast period 2024-2030. This significant growth reflects the increasing demand for sustainable and efficient transportation solutions in the commercial sector. The market's expansion is driven by several factors, including advancements in battery technology, government incentives, and the rising awareness of environmental issues. Businesses are increasingly recognizing the benefits of electric commercial vehicles, such as lower operational costs, reduced emissions, and compliance with stringent environmental regulations. The shift towards electric vehicles is also supported by the growing availability of charging infrastructure and the development of new models with improved performance and range. As a result, the Global Light Electric Commercial Vehicles Market is poised for substantial growth in the coming years, offering numerous opportunities for manufacturers, suppliers, and other stakeholders in the industry. The transition to electric commercial vehicles is not only a response to regulatory pressures but also a strategic move to enhance operational efficiency and sustainability. With the continued focus on reducing carbon footprints and promoting green transportation, the Global Light Electric Commercial Vehicles Market is set to play a crucial role in shaping the future of commercial transportation.

| Report Metric | Details |

| Report Name | Light Electric Commercial Vehicles Market |

| Accounted market size in 2023 | US$ 168 million |

| Forecasted market size in 2030 | US$ 972.3 million |

| CAGR | 28.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Dongfeng Automobile Co., Ltd., Yutong Bus CO.,LTD., Xiamen King Long Motor Group Co.,Ltd., BYD, Geely Automobile Holdings Limited, CRRC Electric VEHICLE Co., Ltd., Zhongtong Bus Holding Co.,Ltd., Chongqing Rui Chi, BAIC Foton Motor Co., Ltd., Chery |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |