What is Global High-Precision Gear Reduction Device Market?

The Global High-Precision Gear Reduction Device Market refers to the worldwide industry focused on the production and distribution of gear reduction devices that offer high precision in their operation. These devices are crucial in applications requiring accurate control of speed and torque, such as robotics, medical equipment, and semiconductor manufacturing. High-precision gear reduction devices are designed to minimize backlash and enhance the efficiency of mechanical systems. They are essential in industries where precision and reliability are paramount, ensuring that machinery operates smoothly and accurately. The market encompasses various types of gear reduction devices, including RV precision reduction devices and harmonic precision reduction devices, each catering to specific needs and applications. As industries continue to advance and demand more precise and efficient machinery, the global market for these high-precision gear reduction devices is expected to grow, driven by technological advancements and increasing applications across various sectors.

RV Precision Reduction Device, Harmonic Precision Reduction Device in the Global High-Precision Gear Reduction Device Market:

RV Precision Reduction Devices and Harmonic Precision Reduction Devices are two key components within the Global High-Precision Gear Reduction Device Market. RV precision reduction devices, also known as RV reducers, are renowned for their high torque capacity, compact size, and exceptional precision. They are widely used in applications that require high accuracy and reliability, such as industrial robots and automated machinery. The RV reducer's design incorporates a cycloidal gear mechanism, which allows for smooth and precise motion control, making it ideal for tasks that demand high precision. On the other hand, Harmonic Precision Reduction Devices, also known as harmonic drives, utilize a unique strain wave gearing mechanism. This design enables them to achieve extremely high reduction ratios in a compact form factor, making them suitable for applications where space is limited but precision is critical. Harmonic drives are commonly used in robotics, aerospace, and medical equipment due to their ability to provide precise and repeatable motion control. Both RV and harmonic precision reduction devices play a crucial role in enhancing the performance and efficiency of various mechanical systems, contributing to the overall growth and development of the high-precision gear reduction device market. As industries continue to evolve and demand more sophisticated and precise machinery, the importance of these devices is expected to increase, driving further innovation and advancements in the field.

Industrial Robot, Medical Equipment, Semiconductor Manufacturing, Others in the Global High-Precision Gear Reduction Device Market:

The usage of Global High-Precision Gear Reduction Devices spans across several critical areas, including industrial robots, medical equipment, semiconductor manufacturing, and other specialized applications. In the realm of industrial robots, these devices are indispensable for ensuring precise and controlled movements. High-precision gear reduction devices enable robots to perform complex tasks with high accuracy, such as assembly, welding, and material handling. The precision and reliability offered by these devices are crucial for maintaining the efficiency and productivity of automated manufacturing processes. In medical equipment, high-precision gear reduction devices are used in various applications, including surgical robots, diagnostic machines, and imaging equipment. These devices ensure that medical instruments operate with the utmost precision, enhancing the accuracy of medical procedures and improving patient outcomes. In semiconductor manufacturing, high-precision gear reduction devices are essential for the production of microchips and other electronic components. The precise control of motion provided by these devices is critical for the intricate processes involved in semiconductor fabrication, such as lithography, etching, and deposition. Additionally, high-precision gear reduction devices find applications in other areas, such as aerospace, defense, and telecommunications, where precision and reliability are paramount. The versatility and effectiveness of these devices make them a vital component in various industries, driving their widespread adoption and contributing to the growth of the global high-precision gear reduction device market.

Global High-Precision Gear Reduction Device Market Outlook:

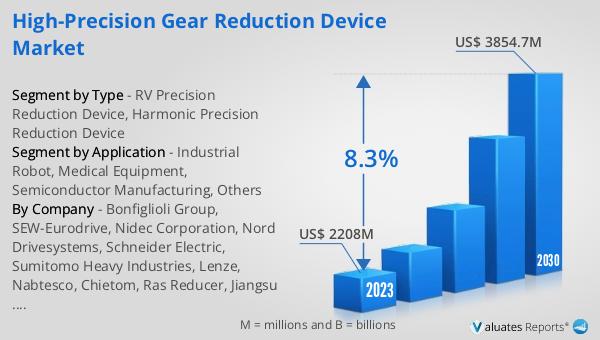

The global High-Precision Gear Reduction Device market was valued at US$ 2208 million in 2023 and is anticipated to reach US$ 3854.7 million by 2030, witnessing a CAGR of 8.3% during the forecast period 2024-2030. This significant growth reflects the increasing demand for high-precision gear reduction devices across various industries. The market's expansion is driven by the need for precise and reliable motion control in applications such as robotics, medical equipment, and semiconductor manufacturing. As industries continue to advance and require more sophisticated machinery, the demand for high-precision gear reduction devices is expected to rise. The market's growth is also supported by technological advancements and innovations in gear reduction technology, which enhance the performance and efficiency of these devices. The increasing adoption of automation and robotics in manufacturing processes further fuels the demand for high-precision gear reduction devices, as they play a crucial role in ensuring the accuracy and reliability of automated systems. Overall, the global high-precision gear reduction device market is poised for substantial growth, driven by the rising demand for precision and efficiency in various industrial applications.

| Report Metric | Details |

| Report Name | High-Precision Gear Reduction Device Market |

| Accounted market size in 2023 | US$ 2208 million |

| Forecasted market size in 2030 | US$ 3854.7 million |

| CAGR | 8.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Bonfiglioli Group, SEW-Eurodrive, Nidec Corporation, Nord Drivesystems, Schneider Electric, Sumitomo Heavy Industries, Lenze, Nabtesco, Chietom, Ras Reducer, Jiangsu Taiyin Transmission Equipment, KEBOT |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |