What is Global Portable Colour Doppler Ultrasound Machine Market?

The Global Portable Colour Doppler Ultrasound Machine Market refers to the worldwide industry focused on the production, distribution, and utilization of portable ultrasound machines equipped with color Doppler technology. These machines are designed to be compact and mobile, making them ideal for use in various medical settings, including hospitals, clinics, and even remote locations. The color Doppler feature allows for the visualization of blood flow within the body, providing critical information for diagnosing and monitoring various medical conditions. This market is driven by the increasing demand for advanced diagnostic tools that offer high accuracy and ease of use. The portability of these machines makes them particularly valuable in emergency situations and in areas with limited access to healthcare facilities. As technology continues to advance, the capabilities of these portable devices are expected to improve, further expanding their applications and market reach.

2D, 3D in the Global Portable Colour Doppler Ultrasound Machine Market:

In the realm of Global Portable Colour Doppler Ultrasound Machines, 2D and 3D imaging technologies play pivotal roles. 2D imaging, or two-dimensional imaging, is the traditional form of ultrasound imaging that provides flat, cross-sectional views of the body. This type of imaging is widely used due to its simplicity and effectiveness in visualizing internal structures. It is particularly useful for examining organs, tissues, and blood vessels, allowing healthcare professionals to detect abnormalities such as tumors, cysts, and blockages. The portability of 2D color Doppler ultrasound machines enhances their utility in various medical settings, from large hospitals to small clinics and even in fieldwork scenarios. On the other hand, 3D imaging, or three-dimensional imaging, offers a more detailed and realistic view of the body's internal structures. This advanced technology captures multiple 2D images from different angles and reconstructs them into a 3D image. The result is a more comprehensive and accurate representation of the area being examined. In the context of portable color Doppler ultrasound machines, 3D imaging is particularly beneficial for complex diagnostic procedures. For instance, in obstetrics and gynecology, 3D imaging can provide detailed views of the fetus, helping in the early detection of congenital anomalies. In cardiology, it allows for a better assessment of heart structures and functions, aiding in the diagnosis and management of heart diseases. The integration of color Doppler technology with 3D imaging further enhances the diagnostic capabilities of these machines. Color Doppler adds the dimension of blood flow visualization, which is crucial for assessing vascular conditions and blood flow abnormalities. This combination of 3D imaging and color Doppler technology provides a powerful tool for healthcare professionals, enabling them to make more accurate diagnoses and develop more effective treatment plans. The portability of these advanced machines ensures that high-quality diagnostic imaging is accessible even in remote or resource-limited settings. As the demand for advanced diagnostic tools continues to grow, the market for portable color Doppler ultrasound machines with 2D and 3D imaging capabilities is expected to expand. The ongoing advancements in imaging technology, coupled with the increasing need for portable and efficient diagnostic solutions, are likely to drive further innovation and growth in this market.

Radiology/Oncology, Cardiology, Obstetrics & Gynecology, Mammography, Emergency Medicine, Vascular, Others in the Global Portable Colour Doppler Ultrasound Machine Market:

The Global Portable Colour Doppler Ultrasound Machine Market finds extensive usage across various medical fields, including Radiology/Oncology, Cardiology, Obstetrics & Gynecology, Mammography, Emergency Medicine, Vascular, and others. In Radiology and Oncology, these machines are invaluable for diagnosing and monitoring tumors and other abnormalities. The color Doppler feature helps in assessing the blood flow to tumors, which is crucial for determining the nature and stage of cancer. In Cardiology, portable color Doppler ultrasound machines are used to evaluate heart structures and functions. They help in diagnosing conditions such as heart valve disorders, congenital heart defects, and cardiomyopathies by providing detailed images of the heart and its blood flow patterns. In Obstetrics & Gynecology, these machines are essential for monitoring fetal development and maternal health. They provide detailed images of the fetus, helping in the early detection of congenital anomalies and other complications. The color Doppler feature is particularly useful for assessing the blood flow in the placenta and umbilical cord, ensuring the well-being of both the mother and the baby. In Mammography, portable color Doppler ultrasound machines are used as a complementary tool to traditional mammograms. They help in differentiating between benign and malignant breast lesions by providing detailed images of the breast tissue and blood flow patterns. In Emergency Medicine, the portability of these machines makes them ideal for quick and accurate diagnosis in critical situations. They can be used to assess trauma patients, detect internal bleeding, and guide emergency procedures such as needle aspirations and catheter placements. In the field of Vascular medicine, these machines are used to evaluate blood vessels and detect conditions such as deep vein thrombosis, arterial blockages, and aneurysms. The color Doppler feature provides real-time visualization of blood flow, helping in the accurate diagnosis and management of vascular conditions. Other areas where portable color Doppler ultrasound machines are used include urology, musculoskeletal imaging, and pediatric care. In urology, they help in diagnosing conditions such as kidney stones, bladder tumors, and prostate abnormalities. In musculoskeletal imaging, they are used to assess injuries and conditions affecting muscles, tendons, and joints. In pediatric care, these machines are used to monitor the development and health of infants and children. The versatility and portability of these machines make them an indispensable tool in modern healthcare, providing high-quality diagnostic imaging across various medical fields.

Global Portable Colour Doppler Ultrasound Machine Market Outlook:

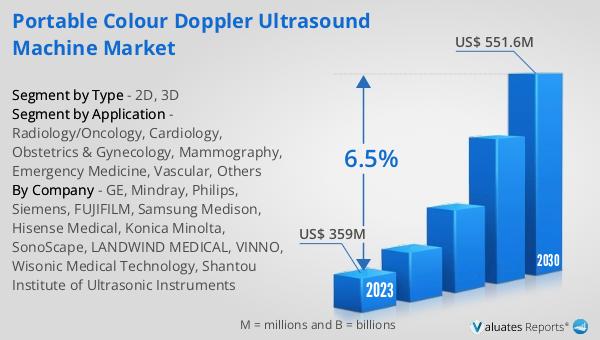

The global market for Portable Colour Doppler Ultrasound Machines was valued at $359 million in 2023 and is projected to grow to $551.6 million by 2030, reflecting a compound annual growth rate (CAGR) of 6.5% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for advanced diagnostic tools that offer high accuracy and ease of use. The portability of these machines makes them particularly valuable in emergency situations and in areas with limited access to healthcare facilities. As technology continues to advance, the capabilities of these portable devices are expected to improve, further expanding their applications and market reach. The rising prevalence of chronic diseases, the growing aging population, and the increasing focus on early diagnosis and preventive healthcare are some of the key factors contributing to the growth of this market. Additionally, the ongoing advancements in imaging technology, coupled with the increasing need for portable and efficient diagnostic solutions, are likely to drive further innovation and growth in this market. The market outlook for Portable Colour Doppler Ultrasound Machines is positive, with significant growth expected in the coming years.

| Report Metric | Details |

| Report Name | Portable Colour Doppler Ultrasound Machine Market |

| Accounted market size in 2023 | US$ 359 million |

| Forecasted market size in 2030 | US$ 551.6 million |

| CAGR | 6.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | GE, Mindray, Philips, Siemens, FUJIFILM, Samsung Medison, Hisense Medical, Konica Minolta, SonoScape, LANDWIND MEDICAL, VINNO, Wisonic Medical Technology, Shantou Institute of Ultrasonic Instruments |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |