What is Global Wearable Sensor Patch Market?

The Global Wearable Sensor Patch Market refers to the industry focused on the development, production, and distribution of small, adhesive patches embedded with sensors that can monitor various physiological parameters. These patches are designed to be worn on the skin and can track a range of health metrics such as heart rate, body temperature, blood glucose levels, and more. The market has seen significant growth due to advancements in sensor technology, increasing health awareness, and the rising demand for remote patient monitoring. Wearable sensor patches are used in various sectors including healthcare, fitness, and sports, providing real-time data that can be crucial for medical diagnostics, personal health management, and athletic performance optimization. The convenience, non-invasiveness, and continuous monitoring capabilities of these patches make them highly attractive to consumers and healthcare providers alike. As technology continues to evolve, the Global Wearable Sensor Patch Market is expected to expand further, offering more sophisticated and accurate monitoring solutions.

Temperature Sensor Patch, Blood Glucose Sensor Patch, Blood Pressure/Flow Sensor Patch, Heart Rate Sensor Patch, Other in the Global Wearable Sensor Patch Market:

Temperature Sensor Patches are designed to continuously monitor body temperature, providing real-time data that can be crucial for detecting fevers or monitoring conditions that affect body temperature regulation. These patches are particularly useful in healthcare settings for patients with chronic illnesses or those recovering from surgery. Blood Glucose Sensor Patches are a game-changer for individuals with diabetes. These patches continuously monitor blood glucose levels, providing real-time data that helps in managing the condition more effectively. They eliminate the need for frequent finger-prick tests, making diabetes management less invasive and more convenient. Blood Pressure/Flow Sensor Patches monitor blood pressure and blood flow, providing critical data that can help in the early detection of cardiovascular issues. These patches are particularly beneficial for individuals with hypertension or other cardiovascular conditions, allowing for continuous monitoring without the need for bulky equipment. Heart Rate Sensor Patches are widely used in both healthcare and fitness settings. They provide continuous heart rate monitoring, which is essential for patients with heart conditions and athletes looking to optimize their training. These patches offer a non-invasive way to keep track of heart health, providing valuable data that can be used to adjust treatment plans or training regimens. Other types of sensor patches include those that monitor respiratory rate, oxygen saturation, and even hydration levels. These patches are used in various applications, from monitoring patients with respiratory conditions to helping athletes stay hydrated during intense training sessions. The versatility and convenience of wearable sensor patches make them an invaluable tool in modern healthcare and fitness.

Healthcare, Fitness & Sports in the Global Wearable Sensor Patch Market:

The usage of Global Wearable Sensor Patch Market in healthcare is transformative. These patches provide continuous, real-time monitoring of various health metrics, which is invaluable for managing chronic conditions, post-operative care, and remote patient monitoring. For instance, a temperature sensor patch can alert healthcare providers to a fever in a post-operative patient, allowing for timely intervention. Blood glucose sensor patches are particularly beneficial for diabetic patients, providing continuous glucose monitoring and reducing the need for invasive finger-prick tests. Blood pressure and heart rate sensor patches are crucial for patients with cardiovascular conditions, offering continuous monitoring that can help in early detection of potential issues. In fitness and sports, wearable sensor patches are used to optimize performance and prevent injuries. Heart rate sensor patches, for example, allow athletes to monitor their heart rate in real-time, helping them to train more effectively and avoid overexertion. Temperature sensor patches can help athletes avoid heat-related illnesses by monitoring body temperature during intense training sessions. Blood flow sensor patches can provide data on muscle oxygenation, helping athletes to optimize their training and recovery. The convenience and non-invasiveness of these patches make them an attractive option for both healthcare providers and fitness enthusiasts. They provide valuable data that can be used to improve health outcomes, optimize performance, and enhance overall well-being.

Global Wearable Sensor Patch Market Outlook:

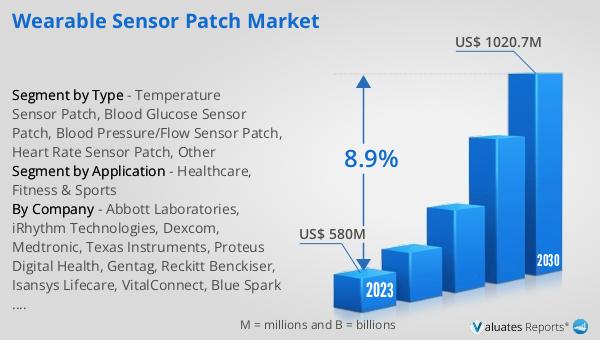

The global Wearable Sensor Patch market was valued at US$ 580 million in 2023 and is anticipated to reach US$ 1020.7 million by 2030, witnessing a CAGR of 8.9% during the forecast period from 2024 to 2030. This significant growth is driven by advancements in sensor technology, increasing health awareness, and the rising demand for remote patient monitoring. Wearable sensor patches offer a convenient, non-invasive way to monitor various health metrics, making them highly attractive to consumers and healthcare providers alike. The market's expansion is also fueled by the growing adoption of these patches in fitness and sports, where they are used to optimize performance and prevent injuries. As technology continues to evolve, the Global Wearable Sensor Patch Market is expected to offer more sophisticated and accurate monitoring solutions, further driving its growth.

| Report Metric | Details |

| Report Name | Wearable Sensor Patch Market |

| Accounted market size in 2023 | US$ 580 million |

| Forecasted market size in 2030 | US$ 1020.7 million |

| CAGR | 8.9% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Abbott Laboratories, iRhythm Technologies, Dexcom, Medtronic, Texas Instruments, Proteus Digital Health, Gentag, Reckitt Benckiser, Isansys Lifecare, VitalConnect, Blue Spark Technologies, Kenzen |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |