What is Global Bio-Based Hydraulic Fluids Market?

The Global Bio-Based Hydraulic Fluids Market is a rapidly evolving sector within the broader hydraulic fluids industry. These fluids are derived from renewable biological sources such as vegetable oils and synthetic esters, making them an environmentally friendly alternative to traditional petroleum-based hydraulic fluids. The primary advantage of bio-based hydraulic fluids is their biodegradability, which significantly reduces the environmental impact in case of leaks or spills. Additionally, these fluids offer excellent lubrication properties, thermal stability, and a high viscosity index, making them suitable for a wide range of industrial applications. The market is driven by increasing environmental regulations and a growing awareness of sustainable practices among industries. As companies strive to reduce their carbon footprint and adhere to stricter environmental standards, the demand for bio-based hydraulic fluids is expected to rise. This market is not only beneficial for the environment but also offers economic advantages by potentially reducing the costs associated with environmental cleanup and disposal of hazardous materials. Overall, the Global Bio-Based Hydraulic Fluids Market represents a significant step towards more sustainable industrial practices.

Vegetable Oils, Synthetic Esters in the Global Bio-Based Hydraulic Fluids Market:

Vegetable oils and synthetic esters are two primary types of bio-based hydraulic fluids that are gaining traction in the Global Bio-Based Hydraulic Fluids Market. Vegetable oils, such as soybean, rapeseed, and sunflower oils, are popular due to their natural availability and biodegradability. These oils are chemically modified to enhance their performance characteristics, such as oxidative stability and low-temperature fluidity, making them suitable for hydraulic systems. Vegetable oils offer excellent lubricity, which reduces wear and tear on hydraulic components, thereby extending the lifespan of machinery. On the other hand, synthetic esters are engineered fluids that offer superior performance compared to vegetable oils. They are synthesized through the chemical reaction of fatty acids and alcohols, resulting in fluids with excellent thermal stability, low volatility, and high viscosity index. Synthetic esters are particularly suitable for high-temperature and high-pressure applications, where traditional hydraulic fluids may fail. They also offer excellent biodegradability and low toxicity, making them an environmentally friendly option. Both vegetable oils and synthetic esters are gaining popularity due to their ability to meet stringent environmental regulations while providing high performance. The choice between vegetable oils and synthetic esters depends on the specific requirements of the application, such as operating temperature, pressure, and environmental conditions. In summary, vegetable oils and synthetic esters are two key components of the Global Bio-Based Hydraulic Fluids Market, each offering unique advantages that cater to different industrial needs.

Mining, Construction, Transportation, Oil & Gas, Metal Production, Food & Beverage, Others in the Global Bio-Based Hydraulic Fluids Market:

The usage of Global Bio-Based Hydraulic Fluids Market spans across various industries, including mining, construction, transportation, oil & gas, metal production, food & beverage, and others. In the mining industry, bio-based hydraulic fluids are used in heavy machinery and equipment to ensure smooth operation and reduce the risk of environmental contamination in case of leaks. The biodegradability of these fluids is particularly important in mining operations, where spills can have severe environmental consequences. In the construction industry, bio-based hydraulic fluids are used in a wide range of equipment, including excavators, loaders, and cranes. These fluids help in reducing the carbon footprint of construction activities and comply with environmental regulations. In the transportation sector, bio-based hydraulic fluids are used in various vehicles, including trucks, buses, and trains. They help in improving fuel efficiency and reducing emissions, contributing to a cleaner environment. In the oil & gas industry, bio-based hydraulic fluids are used in drilling rigs, pumps, and other equipment. Their high performance and biodegradability make them suitable for use in environmentally sensitive areas. In the metal production industry, bio-based hydraulic fluids are used in hydraulic presses, rolling mills, and other machinery. They help in reducing wear and tear on equipment and improve the overall efficiency of operations. In the food & beverage industry, bio-based hydraulic fluids are used in food processing equipment, where the risk of contamination must be minimized. These fluids are non-toxic and safe for use in food-related applications. Overall, the Global Bio-Based Hydraulic Fluids Market plays a crucial role in various industries by providing environmentally friendly and high-performance hydraulic fluids.

Global Bio-Based Hydraulic Fluids Market Outlook:

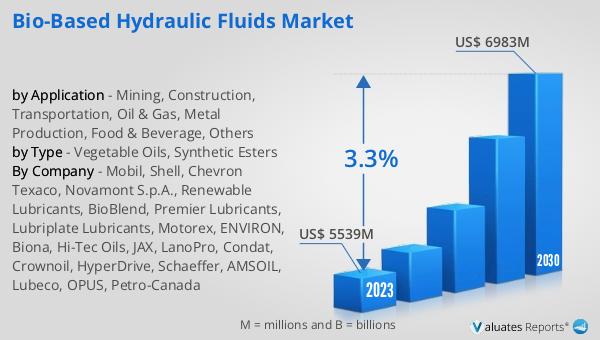

The global Bio-Based Hydraulic Fluids market was valued at US$ 5539 million in 2023 and is anticipated to reach US$ 6983 million by 2030, witnessing a CAGR of 3.3% during the forecast period 2024-2030. This market growth reflects the increasing demand for sustainable and environmentally friendly hydraulic fluids across various industries. The shift towards bio-based hydraulic fluids is driven by stringent environmental regulations and a growing awareness of the need to reduce carbon footprints. Companies are increasingly adopting these fluids to comply with regulations and to enhance their sustainability profiles. The market's steady growth rate indicates a positive outlook for the future, with more industries expected to transition to bio-based hydraulic fluids. This transition not only benefits the environment but also offers economic advantages by potentially reducing costs associated with environmental cleanup and disposal of hazardous materials. The Global Bio-Based Hydraulic Fluids Market is poised for significant growth, driven by the dual benefits of environmental sustainability and high performance.

| Report Metric | Details |

| Report Name | Bio-Based Hydraulic Fluids Market |

| Accounted market size in 2023 | US$ 5539 million |

| Forecasted market size in 2030 | US$ 6983 million |

| CAGR | 3.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Mobil, Shell, Chevron Texaco, Novamont S.p.A., Renewable Lubricants, BioBlend, Premier Lubricants, Lubriplate Lubricants, Motorex, ENVIRON, Biona, Hi-Tec Oils, JAX, LanoPro, Condat, Crownoil, HyperDrive, Schaeffer, AMSOIL, Lubeco, OPUS, Petro-Canada |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |