What is Global Non-Sealed Motorcycle Chain Market?

The Global Non-Sealed Motorcycle Chain Market refers to the worldwide industry focused on the production, distribution, and sale of non-sealed chains used in motorcycles. Unlike sealed chains, non-sealed chains do not have O-rings or X-rings to keep the lubricant inside the chain links, making them more affordable and easier to maintain. These chains are typically used in motorcycles that operate in less demanding environments, where the need for constant lubrication and cleaning is manageable. The market encompasses various types of non-sealed chains, including standard roller chains and heavy-duty roller chains, which cater to different performance requirements and motorcycle types. The demand for non-sealed motorcycle chains is driven by factors such as the increasing popularity of motorcycles for commuting and leisure, especially in developing countries, and the cost-effectiveness of non-sealed chains compared to their sealed counterparts. Additionally, the market is influenced by the growth of the motorcycle aftermarket, where riders seek replacement parts and upgrades for their bikes. Overall, the Global Non-Sealed Motorcycle Chain Market plays a crucial role in the motorcycle industry, providing essential components that ensure the smooth operation and longevity of motorcycles.

Standard Roller Chain, Heavy-Duty Roller Chain, Others in the Global Non-Sealed Motorcycle Chain Market:

Standard roller chains are a fundamental component of the Global Non-Sealed Motorcycle Chain Market. These chains consist of a series of cylindrical rollers held together by side links, which engage with the sprockets on the motorcycle to transmit power from the engine to the wheels. Standard roller chains are known for their simplicity, durability, and cost-effectiveness, making them a popular choice for a wide range of motorcycles, from small commuter bikes to larger touring models. They are particularly favored in regions where motorcycles are a primary mode of transportation due to their affordability and ease of maintenance. Heavy-duty roller chains, on the other hand, are designed to withstand more demanding conditions and higher loads. These chains are constructed with thicker plates and stronger pins, providing enhanced strength and durability. Heavy-duty roller chains are commonly used in high-performance motorcycles, off-road bikes, and motorcycles that are subjected to harsh riding conditions. They offer superior resistance to wear and elongation, ensuring reliable performance even in challenging environments. In addition to standard and heavy-duty roller chains, the Global Non-Sealed Motorcycle Chain Market also includes other types of chains, such as specialty chains designed for specific applications. These may include chains with unique materials or coatings to enhance their performance characteristics, such as corrosion resistance or reduced friction. Specialty chains are often used in niche markets or for custom motorcycle builds, where specific performance attributes are required. Overall, the diversity of chain types within the Global Non-Sealed Motorcycle Chain Market allows manufacturers and riders to select the most appropriate chain for their specific needs, ensuring optimal performance and longevity of their motorcycles.

OEM, Aftermarket in the Global Non-Sealed Motorcycle Chain Market:

The Global Non-Sealed Motorcycle Chain Market serves two primary segments: Original Equipment Manufacturer (OEM) and Aftermarket. In the OEM segment, non-sealed motorcycle chains are supplied directly to motorcycle manufacturers for installation on new bikes. OEM chains are typically designed to meet the specific requirements of the motorcycle models they are intended for, ensuring compatibility and optimal performance. Manufacturers often choose non-sealed chains for their cost-effectiveness and ease of maintenance, particularly for entry-level and mid-range motorcycles. The use of non-sealed chains in OEM applications helps keep the overall cost of the motorcycle down, making them more accessible to a broader range of consumers. In the Aftermarket segment, non-sealed motorcycle chains are sold as replacement parts or upgrades for existing motorcycles. The aftermarket is a significant driver of demand for non-sealed chains, as riders seek to maintain or enhance the performance of their bikes. Non-sealed chains are popular in the aftermarket due to their affordability and the ease with which they can be installed and maintained. Riders who frequently use their motorcycles for commuting or leisure often prefer non-sealed chains for their simplicity and cost-effectiveness. Additionally, the aftermarket provides opportunities for customization, allowing riders to choose chains that match their specific riding style and preferences. The availability of a wide range of non-sealed chains in the aftermarket ensures that riders can find the right chain for their motorcycle, whether they are looking for a standard roller chain for everyday use or a heavy-duty chain for more demanding conditions. Overall, the Global Non-Sealed Motorcycle Chain Market plays a vital role in both the OEM and Aftermarket segments, providing essential components that contribute to the performance and longevity of motorcycles.

Global Non-Sealed Motorcycle Chain Market Outlook:

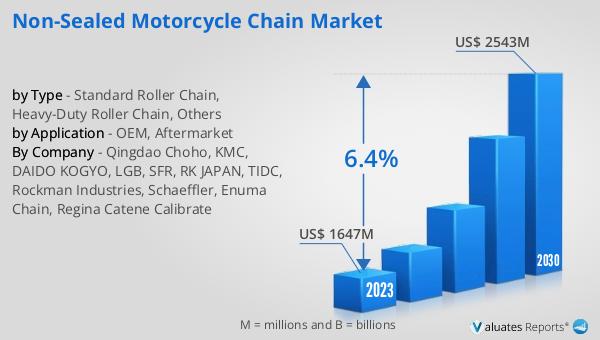

The global Non-Sealed Motorcycle Chain market was valued at US$ 1647 million in 2023 and is anticipated to reach US$ 2543 million by 2030, witnessing a CAGR of 6.4% during the forecast period 2024-2030. This market outlook indicates a robust growth trajectory for the non-sealed motorcycle chain industry, driven by factors such as increasing motorcycle sales, particularly in emerging markets, and the cost advantages of non-sealed chains. The projected growth underscores the importance of non-sealed chains in the motorcycle industry, as they offer a cost-effective and reliable solution for power transmission. The market's expansion is also likely to be supported by advancements in chain manufacturing technologies and materials, which enhance the performance and durability of non-sealed chains. As the market continues to grow, it will provide opportunities for manufacturers, distributors, and retailers to capitalize on the increasing demand for non-sealed motorcycle chains. The anticipated growth in market value reflects the ongoing importance of non-sealed chains in meeting the needs of motorcycle riders worldwide, ensuring that they remain a key component in the global motorcycle industry.

| Report Metric | Details |

| Report Name | Non-Sealed Motorcycle Chain Market |

| Accounted market size in 2023 | US$ 1647 million |

| Forecasted market size in 2030 | US$ 2543 million |

| CAGR | 6.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Qingdao Choho, KMC, DAIDO KOGYO, LGB, SFR, RK JAPAN, TIDC, Rockman Industries, Schaeffler, Enuma Chain, Regina Catene Calibrate |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |