What is Global Biodegradable Floral Foam Market?

The Global Biodegradable Floral Foam Market refers to the industry focused on producing and distributing floral foam that is environmentally friendly and decomposes naturally over time. Traditional floral foam, often used by florists to arrange and support flowers, is made from synthetic materials that do not break down easily and can contribute to environmental pollution. In contrast, biodegradable floral foam is designed to offer the same functionality while being more sustainable. This market is driven by increasing environmental awareness and the demand for eco-friendly products. Consumers and businesses alike are becoming more conscious of their environmental footprint, leading to a growing preference for biodegradable options. The market encompasses various types of biodegradable floral foam, catering to different needs and preferences, and is supported by advancements in material science and manufacturing processes that make these products more effective and affordable.

in the Global Biodegradable Floral Foam Market:

Biodegradable floral foam comes in various types, each designed to meet the specific needs of different customers. One common type is the water-absorbing biodegradable foam, which is ideal for fresh flower arrangements. This type of foam can hold water for extended periods, keeping flowers hydrated and fresh. It is often used by florists for creating bouquets, centerpieces, and other floral displays. Another type is the dry biodegradable foam, which is used for artificial flowers and dried flower arrangements. This foam does not absorb water but provides a sturdy base for securing stems and other decorative elements. It is popular among hobbyists and DIY enthusiasts who create long-lasting floral decorations. There is also a type of biodegradable foam that is infused with nutrients, designed to support the growth of live plants. This type is used in horticulture and gardening, providing a sustainable alternative to traditional planting mediums. Additionally, some biodegradable foams are designed to be more rigid and durable, suitable for large-scale commercial displays and installations. These foams can support heavier floral arrangements and are often used in event planning and interior decoration. The versatility of biodegradable floral foam makes it suitable for a wide range of applications, from small personal projects to large professional installations. As the market continues to grow, manufacturers are developing new formulations and types of biodegradable foam to meet the evolving needs of their customers. This includes foams with enhanced water retention properties, improved structural integrity, and added features such as pest resistance. The development of these new products is driven by ongoing research and innovation in material science, as well as feedback from customers and industry professionals. By offering a variety of biodegradable floral foam options, the market is able to cater to the diverse needs of its customers, promoting sustainability and reducing environmental impact.

Commercial, Residential in the Global Biodegradable Floral Foam Market:

The usage of biodegradable floral foam in commercial and residential settings highlights its versatility and environmental benefits. In commercial settings, biodegradable floral foam is widely used by florists, event planners, and interior decorators. Florists use it to create stunning floral arrangements for weddings, corporate events, and other special occasions. The foam provides a stable base for flowers, allowing for intricate designs and ensuring that the arrangements stay fresh throughout the event. Event planners and decorators also use biodegradable floral foam for large-scale installations, such as floral arches, centerpieces, and stage decorations. The foam's ability to hold water and support heavy arrangements makes it an ideal choice for these applications. Additionally, businesses that prioritize sustainability often choose biodegradable floral foam to align with their environmental goals and reduce their carbon footprint. In residential settings, biodegradable floral foam is popular among hobbyists and DIY enthusiasts who enjoy creating their own floral arrangements. It is used for making bouquets, wreaths, and other decorative pieces that can brighten up a home. The foam's ease of use and ability to keep flowers fresh make it a favorite among home decorators. Gardeners and horticulturists also use biodegradable floral foam for planting and growing live plants. The foam provides a nutrient-rich medium that supports plant growth and can be easily integrated into garden beds or pots. This makes it a sustainable alternative to traditional soil and planting mediums. Overall, the use of biodegradable floral foam in both commercial and residential settings demonstrates its practicality and environmental benefits. By choosing biodegradable options, consumers and businesses can enjoy beautiful floral arrangements while minimizing their impact on the environment.

Global Biodegradable Floral Foam Market Outlook:

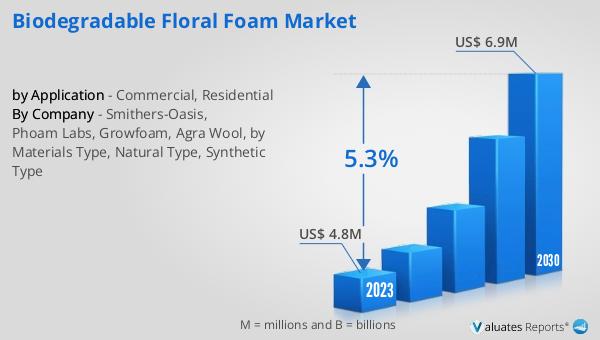

The global market for biodegradable floral foam was valued at $4.8 million in 2023 and is expected to grow to $6.9 million by 2030, with a compound annual growth rate (CAGR) of 5.3% during the forecast period from 2024 to 2030. This growth reflects the increasing demand for sustainable and eco-friendly products in the floral industry. As more consumers and businesses become aware of the environmental impact of traditional floral foam, the shift towards biodegradable alternatives is gaining momentum. The market's steady growth is supported by advancements in material science and manufacturing processes, which have made biodegradable floral foam more effective and affordable. This positive market outlook indicates a promising future for biodegradable floral foam, driven by the growing emphasis on sustainability and environmental responsibility.

| Report Metric | Details |

| Report Name | Biodegradable Floral Foam Market |

| Accounted market size in 2023 | US$ 4.8 million |

| Forecasted market size in 2030 | US$ 6.9 million |

| CAGR | 5.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Smithers-Oasis, Phoam Labs, Growfoam, Agra Wool, by Materials Type, Natural Type, Synthetic Type |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |