What is Global Security Radiation Portal Monitors Market?

The Global Security Radiation Portal Monitors Market is a specialized sector focused on the development and deployment of devices designed to detect and monitor radiation levels. These monitors are crucial for ensuring safety and security in various environments by identifying the presence of radioactive materials. They are typically installed at strategic locations such as border crossings, ports, and critical infrastructure to prevent the illicit trafficking of nuclear and radiological materials. The market encompasses a range of products, including fixed and mobile units, each tailored to specific applications and environments. The demand for these monitors is driven by increasing concerns over nuclear terrorism, the need for regulatory compliance, and the growing awareness of radiation hazards. As a result, the market is characterized by continuous innovation and technological advancements aimed at enhancing detection capabilities and operational efficiency.

Personal Type, Vehicle Type in the Global Security Radiation Portal Monitors Market:

In the Global Security Radiation Portal Monitors Market, there are different types of monitors designed to cater to specific needs, including personal and vehicle types. Personal radiation monitors are portable devices that individuals can carry to detect radiation exposure in real-time. These are particularly useful for first responders, security personnel, and workers in environments where radiation exposure is a risk. They provide immediate alerts and data, enabling quick decision-making and response to potential threats. On the other hand, vehicle radiation monitors are installed at checkpoints, border crossings, and entry points of critical infrastructure to scan vehicles for radioactive materials. These monitors are designed to detect radiation from a distance, ensuring that vehicles carrying hazardous materials are identified before they can enter sensitive areas. Vehicle monitors are often integrated with automated systems to facilitate efficient and non-intrusive screening processes. Both personal and vehicle radiation monitors play a crucial role in enhancing security and safety by providing reliable and accurate radiation detection capabilities.

Homeland Security, Steel Recycling and Smelting, Nuclear Industry, Airports & Seaports, Others in the Global Security Radiation Portal Monitors Market:

The usage of Global Security Radiation Portal Monitors Market spans across various critical areas, including Homeland Security, Steel Recycling and Smelting, the Nuclear Industry, Airports & Seaports, and others. In Homeland Security, these monitors are essential for preventing the illicit trafficking of radioactive materials, thereby safeguarding national security. They are deployed at border crossings, government buildings, and other high-risk locations to detect and deter potential threats. In the Steel Recycling and Smelting industry, radiation portal monitors are used to ensure that scrap metal is free from radioactive contamination before it is processed. This is crucial for maintaining the safety of workers and the quality of the final product. In the Nuclear Industry, these monitors are used to detect and monitor radiation levels in and around nuclear facilities, ensuring compliance with safety regulations and protecting both workers and the environment. At Airports & Seaports, radiation portal monitors are installed to screen cargo and passengers for radioactive materials, enhancing security and preventing the smuggling of hazardous substances. Other areas where these monitors are used include hospitals, research facilities, and waste management sites, where they help to detect and manage radiation exposure. Overall, the widespread usage of radiation portal monitors underscores their importance in maintaining safety and security across various sectors.

Global Security Radiation Portal Monitors Market Outlook:

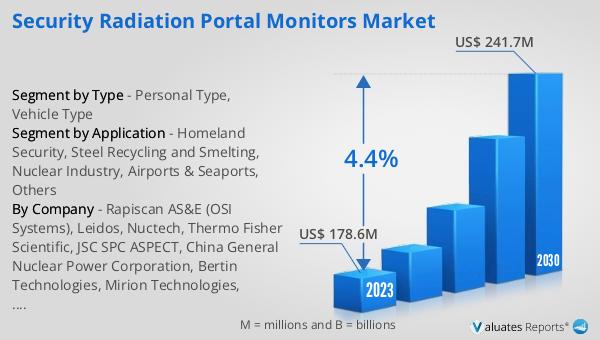

The global Security Radiation Portal Monitors market was valued at US$ 178.6 million in 2023 and is anticipated to reach US$ 241.7 million by 2030, witnessing a CAGR of 4.4% during the forecast period 2024-2030. This growth is driven by increasing concerns over nuclear terrorism, the need for regulatory compliance, and the growing awareness of radiation hazards. The market is characterized by continuous innovation and technological advancements aimed at enhancing detection capabilities and operational efficiency. As a result, the demand for these monitors is expected to rise steadily over the forecast period.

| Report Metric | Details |

| Report Name | Security Radiation Portal Monitors Market |

| Accounted market size in 2023 | US$ 178.6 million |

| Forecasted market size in 2030 | US$ 241.7 million |

| CAGR | 4.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Rapiscan AS&E (OSI Systems), Leidos, Nuctech, Thermo Fisher Scientific, JSC SPC ASPECT, China General Nuclear Power Corporation, Bertin Technologies, Mirion Technologies, Radiation Solutions Inc., Polimaster, ShangHai Ergonomics Detecting Instrument, Symetrica, RadComm Systems, Arktis Radiation Detectors, NuviaTech Instruments, Ludlum Measurements, ATOMTEX, NuCare Inc. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |